How Boise Cascade's Sharp Earnings Drop Will Impact BCC Investors

Boise Cascade Co. BCC | 0.00 |

- Boise Cascade reported third quarter 2025 earnings, with sales reaching US$1.67 billion and net income at US$21.77 million, both decreasing from the previous year.

- This earnings release highlighted a sharp year-over-year drop in profitability, with basic earnings per share falling to US$0.58 from US$2.34 a year earlier.

- We will examine how this pronounced decline in sales and earnings shapes Boise Cascade's investment narrative going forward.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Boise Cascade Investment Narrative Recap

To be a shareholder in Boise Cascade, you generally need to believe in the company’s long-term exposure to US housing and remodeling demand, and its ongoing investments in manufacturing and distribution. The recent third quarter earnings report, which showed clear declines in both sales and profit, reinforces concerns around persistent pricing pressures and soft end-market demand, currently the most important short-term challenges. This earnings miss amplifies the biggest risk to the business, which remains prolonged margin and revenue weakness if housing markets and wood product prices do not recover.

One noteworthy recent announcement is Boise Cascade’s ongoing share repurchase program, capped at US$300 million. While this action typically signals management confidence and can support earnings per share, the benefit to investors may be muted unless underlying demand and profitability trends stabilize, given the backdrop of sustained earnings pressure highlighted in the latest results.

However, it’s also important for investors to be aware that, in contrast to management’s positive capital allocation moves, the company is still contending with...

Boise Cascade is projected to reach $7.0 billion in revenue and $285.8 million in earnings by 2028. This outlook assumes a 2.4% annual revenue growth rate and a $23.5 million increase in earnings from the current $262.3 million.

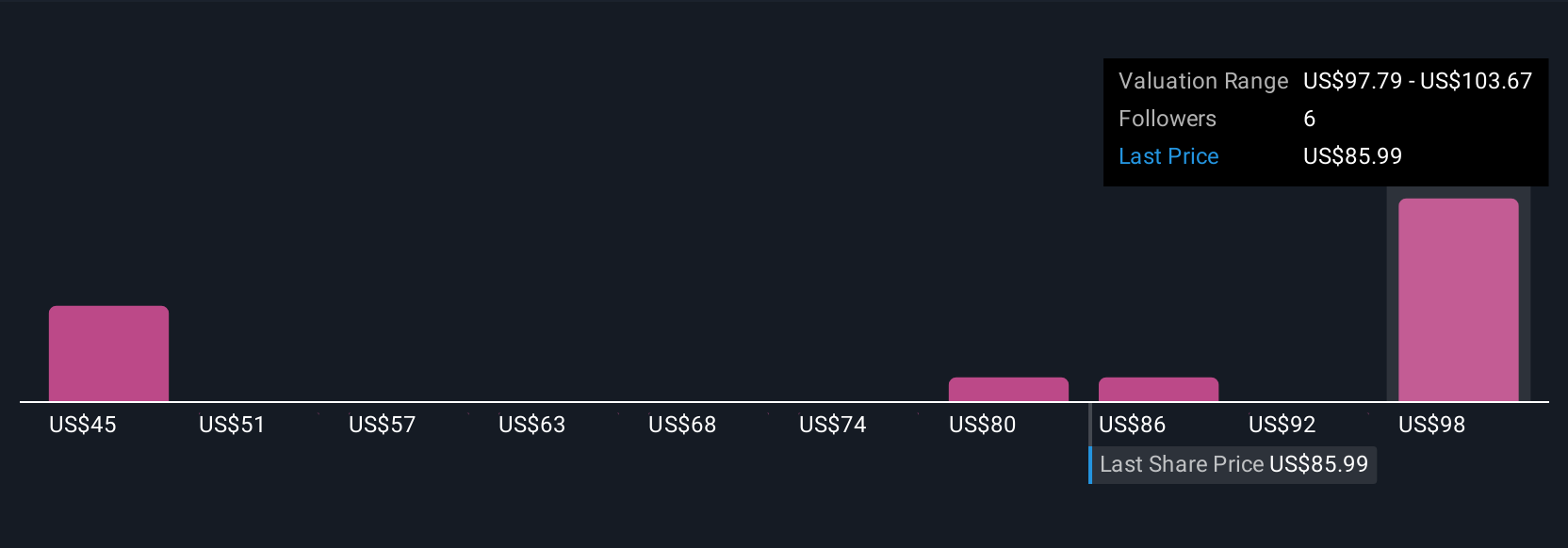

Uncover how Boise Cascade's forecasts yield a $91.17 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community estimate Boise Cascade’s fair value anywhere between US$70 and US$228, suggesting widely different revenue and margin expectations. These differences come as pricing pressure and lackluster demand continue to weigh on sentiment, challenging investors to consider a broad range of potential outcomes.

Explore 5 other fair value estimates on Boise Cascade - why the stock might be worth just $70.00!

Build Your Own Boise Cascade Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Boise Cascade research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Boise Cascade research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boise Cascade's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.