How Booz Allen Hamilton's Expanded US$1.50 Billion Credit Facility At BAH Has Changed Its Investment Story

Booz Allen Hamilton Holding Corporation Class A BAH | 0.00 |

- On February 27, 2026, Booz Allen Hamilton Holding Corporation amended its long-standing credit agreement, lifting its revolving credit facility from US$1.0 billion to US$1.50 billion, extending maturities to 2031, and refinancing part of its term loans.

- The amendment also broadens the company’s capacity to take on new debt and return cash via dividends and share repurchases, potentially reshaping its financial flexibility and capital allocation options.

- Next, we will examine how this expanded US$1.50 billion revolving credit capacity may influence Booz Allen Hamilton’s investment narrative and risk profile.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Booz Allen Hamilton Holding Investment Narrative Recap

To own Booz Allen Hamilton, you need to believe its government focused tech consulting model can keep converting contract demand into steady earnings despite funding delays and intense competition. The recent US$500 million increase in revolving credit and extended debt maturities mainly enhances financial flexibility; it does not materially change the near term revenue timing risk from slow federal procurement, though it could modestly influence how management balances growth investments with shareholder returns.

The January 23, 2026 earnings release is especially relevant here, with nine month sales at US$8,434 million and net income at US$646 million, highlighting how revenue softness can coexist with solid profitability. The richer credit agreement, alongside a higher quarterly dividend of US$0.59 per share, gives Booz Allen more room to support payouts and potential buybacks while managing a high debt load, which interacts directly with the catalysts and risks around earnings volatility.

Yet investors should also weigh how this higher debt capacity might amplify Booz Allen’s exposure to government funding delays and contract concentration risk...

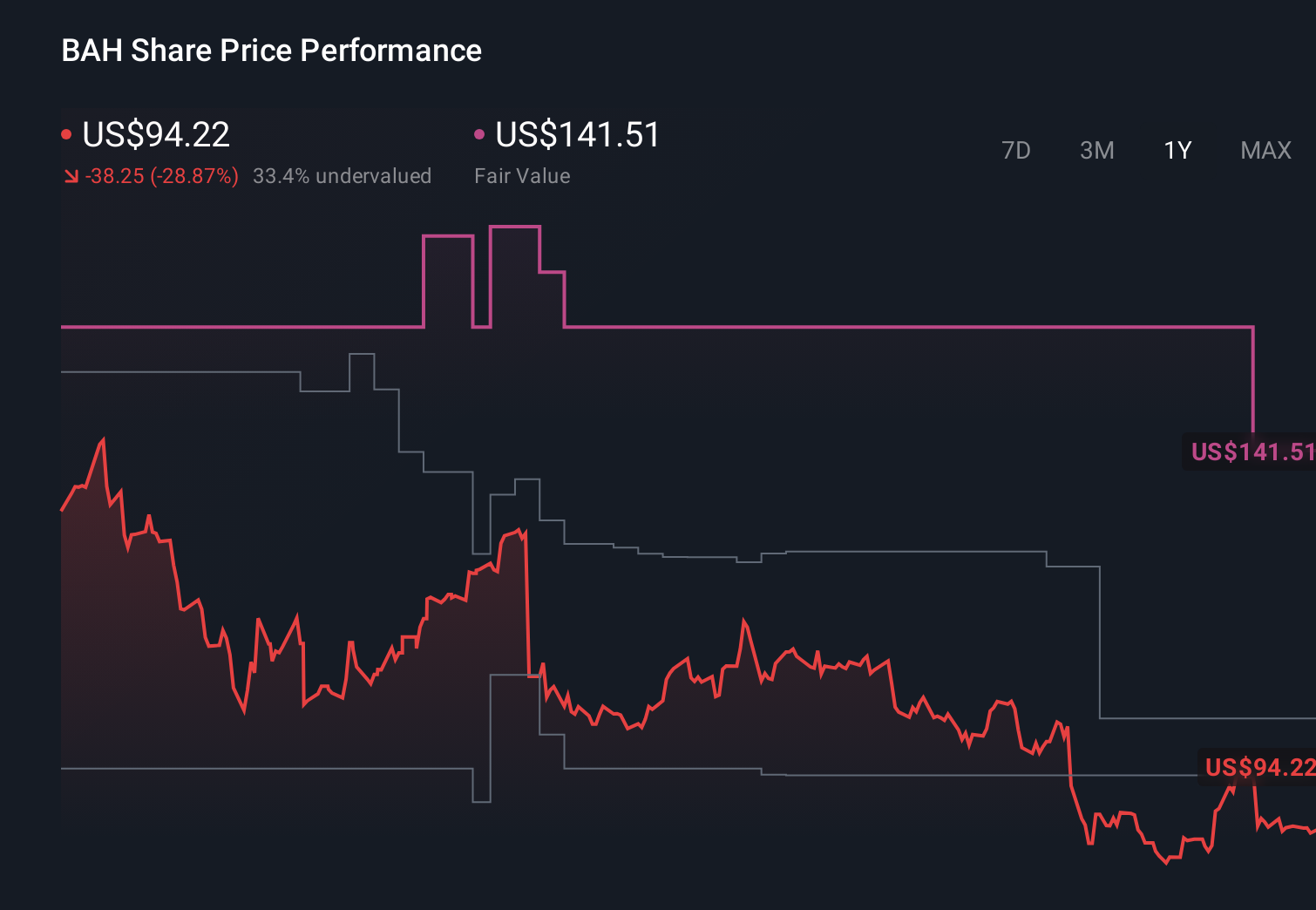

Booz Allen Hamilton Holding's narrative projects $13.5 billion revenue and $775.2 million earnings by 2028. This requires 4.1% yearly revenue growth and an earnings decrease of about $224.8 million from $1.0 billion today.

Uncover how Booz Allen Hamilton Holding's forecasts yield a $106.82 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenue around US$14.6 billion and earnings near US$859 million by 2028, which is far more upbeat than consensus. The expanded US$1.50 billion revolver could either support that growth centric view or sharpen concerns about debt and government exposure, so it is worth comparing how different investors weigh these contrasting paths.

Explore 8 other fair value estimates on Booz Allen Hamilton Holding - why the stock might be worth just $80.00!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Booz Allen Hamilton Holding research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Booz Allen Hamilton Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Booz Allen Hamilton Holding's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.