How Brazil’s BEYONTTRA Approval and New Data Releases Will Impact BridgeBio Pharma (BBIO) Investors

BridgeBio Pharma BBIO | 0.00 |

- BridgeBio Pharma recently received Brazilian regulator ANVISA’s approval for BEYONTTRA (acoramidis) to treat adult transthyretin amyloidosis cardiomyopathy (ATTR-CM), based on positive Phase 3 ATTRibute-CM results, and plans to begin commercialization in partnership with Biopas in the second half of 2026.

- Alongside this new Latin American market entry, BridgeBio is spotlighting its rare disease portfolio with fresh Phase 3 data on acoramidis and encaleret at major global cardiology and endocrinology conferences, reinforcing clinical depth behind its pipeline story.

- We’ll now examine how Brazil’s BEYONTTRA approval, supported by ATTRibute-CM data, could influence BridgeBio’s previously outlined investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

BridgeBio Pharma Investment Narrative Recap

To own BridgeBio, you need to believe its rare disease focus and ATTR-CM franchise can eventually support profitability despite high cash burn and concentration in Attruby. Brazil’s BEYONTTRA approval broadens geographic reach but does not meaningfully change that the most important near term catalyst is continued execution of global acoramidis launches, while the biggest risk remains sustained losses and potential future dilution if expenses keep outpacing revenue.

The Brazilian ANVISA approval for BEYONTTRA, with commercialization targeted for the second half of 2026, is the clearest near term tie to BridgeBio’s existing acoramidis story. It complements upcoming Phase 3 ATTRibute-CM data presentations at ESC Heart Failure 2026, which keep clinical momentum in focus and could shape physician adoption trends, a key factor for how quickly revenue might scale relative to the company’s elevated operating expense base.

Yet despite this clinical and regulatory progress, investors should still watch for the risk that high operating costs and potential future equity raises could...

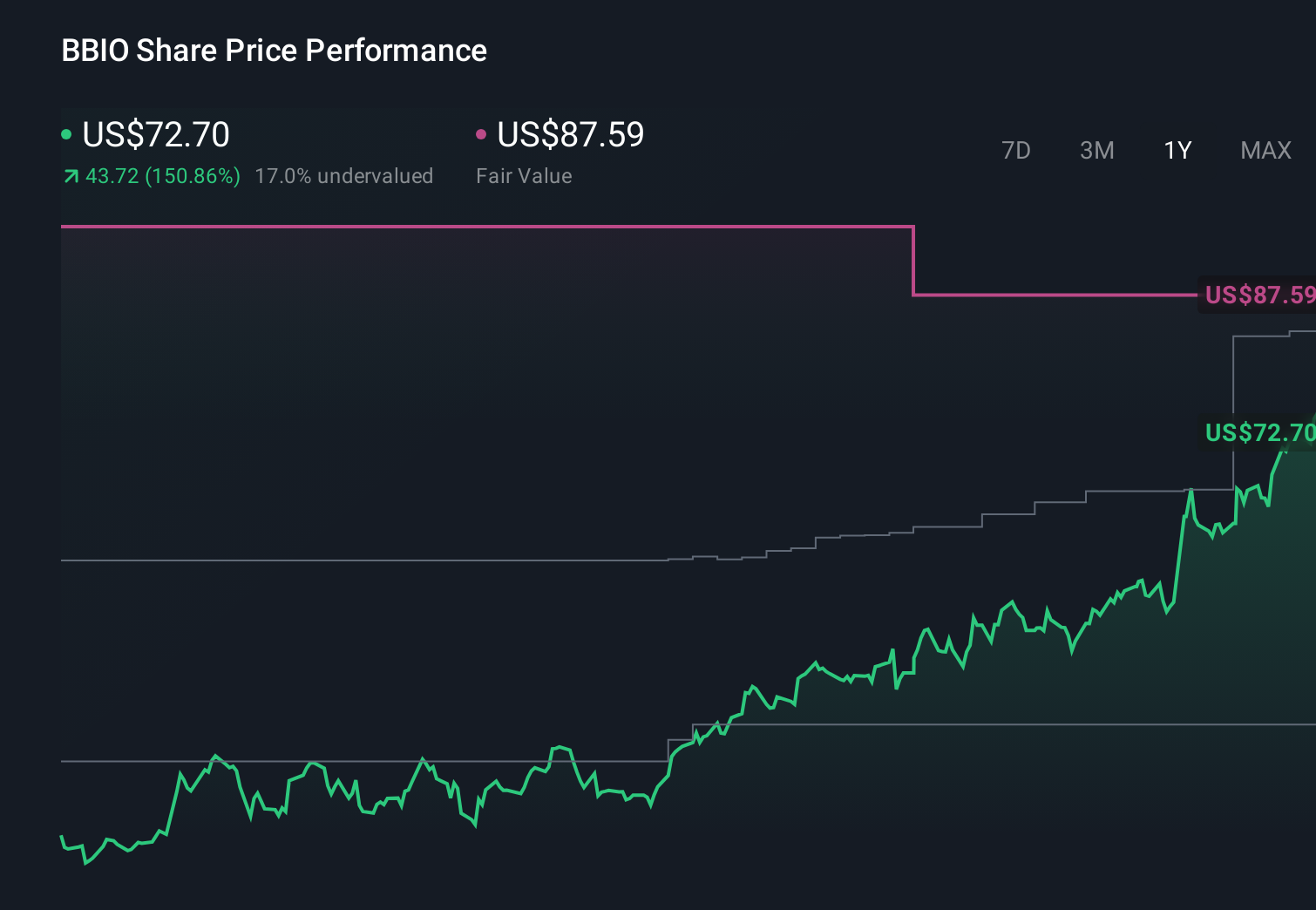

BridgeBio Pharma's narrative projects $2.4 billion revenue and $758.3 million earnings by 2029.

Uncover how BridgeBio Pharma's forecasts yield a $100.89 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$3.4 billion and earnings US$1.3 billion by 2029, so you should expect that views on Brazil’s approval and broader ATTR-CM momentum may push those bullish scenarios even further from the more cautious consensus and make it worthwhile to compare these sharply different outlooks before deciding how you feel about BridgeBio’s long term potential.

Explore 9 other fair value estimates on BridgeBio Pharma - why the stock might be worth over 4x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your BridgeBio Pharma research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free BridgeBio Pharma research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BridgeBio Pharma's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.