How Carvana’s Q1 Results, Stock Split and Chicago Expansion At Carvana (CVNA) Have Changed Its Investment Story

Carvana CVNA | 0.00 |

- In early May 2026, Carvana reported first‑quarter results showing revenue of US$6.43 billion and net income of US$250 million, while also executing a five‑for‑one stock split and confirming that shareholders rejected a proposal for an independent board chair at its annual meeting.

- A key operational update was Carvana’s plan to add inspection and reconditioning capabilities to its ADESA Chicago site, expanding local inventory and fulfillment capacity and supporting faster delivery and broader vehicle selection for customers in the Chicago area and wholesale buyers.

- We’ll now examine how Carvana’s stock split and Chicago reconditioning expansion may influence the company’s longer‑term investment narrative.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

Carvana Investment Narrative Recap

To own Carvana, you need to believe its online model can keep scaling while reconditioning and logistics investments eventually support sustainable profitability. The latest stock split and strong Q1 results highlight execution upside, but the most important near term catalyst remains efficient ramp up of new capacity. The biggest risk is that expanded ADESA integrations like Chicago run below optimal utilization for too long, keeping unit costs elevated. So far, this news does not materially change that balance.

The ADESA Chicago reconditioning expansion is the most relevant update here, because it goes straight to that utilization question. Adding IRC capabilities and a local inventory pool fits the broader push to use technology and infrastructure to lower per unit costs and improve delivery speed. If Chicago and similar sites scale smoothly, they could support the growth narrative. If they lag, they could instead reinforce concerns about operational bottlenecks and margin pressure.

Yet even with solid recent results, higher reconditioning and logistics costs remain a risk investors should be aware of if utilization falls short of...

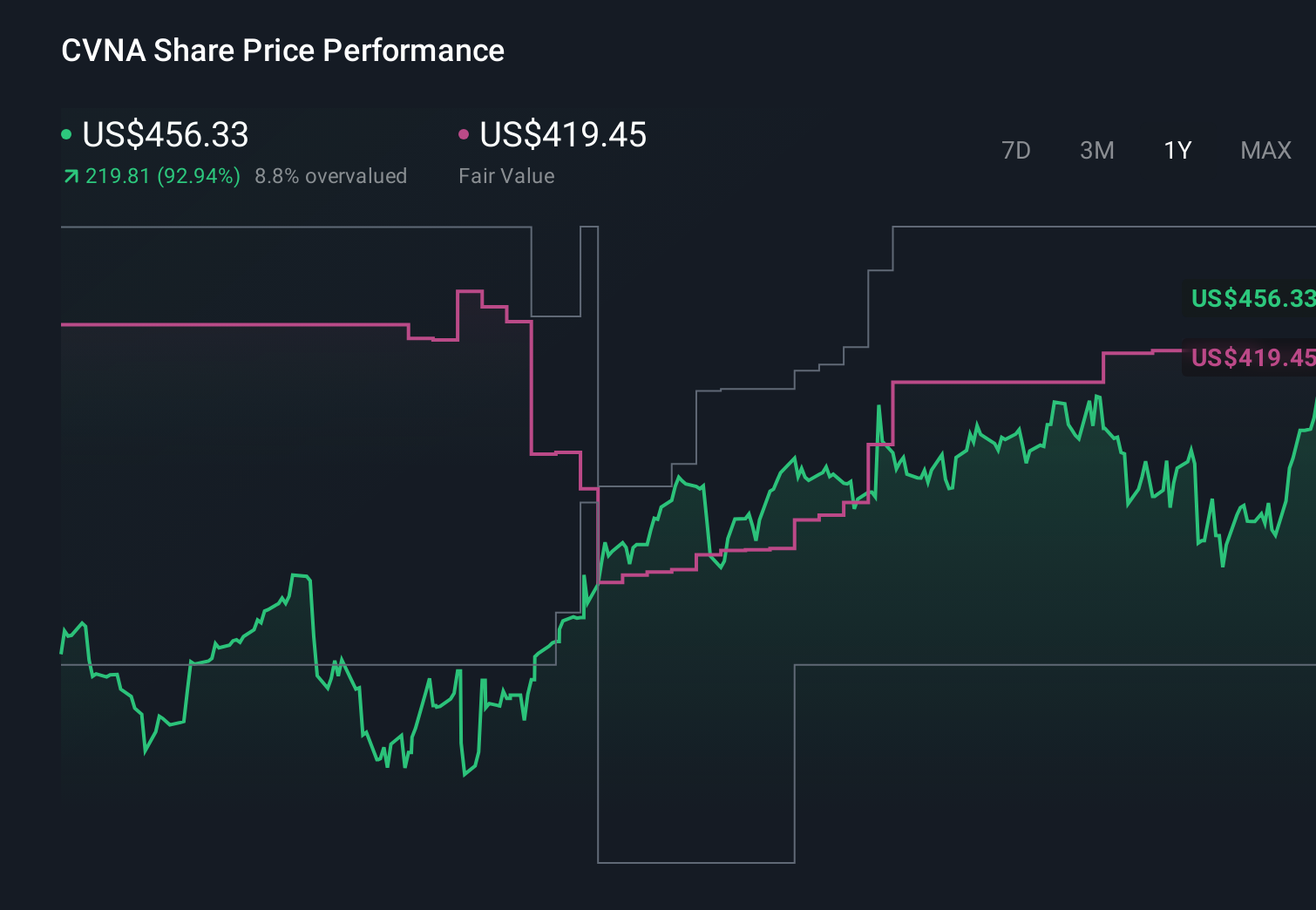

Carvana's narrative projects $40.2 billion revenue and $3.0 billion earnings by 2029. This requires 25.6% yearly revenue growth and a $1.6 billion earnings increase from $1.4 billion today.

Uncover how Carvana's forecasts yield a $428.50 fair value, a 481% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts came in far more cautious, assuming earnings of about US$1.7 billion by 2029 and margin compression, while others point to ADESA expansions as a path to better unit economics, so you should recognize how far apart these views are and consider how fresh news like the Chicago IRC could shift either side of that debate.

Explore 14 other fair value estimates on Carvana - why the stock might be worth over 7x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.