How China’s 200-Jet Order and Tariff Talks Could Reshape Boeing’s (BA) China Market Access

Boeing Company BA | 0.00 |

- Earlier this week, China confirmed an order for 200 Boeing aircraft following talks between Presidents Trump and Xi, reviving Boeing’s access to a key aviation market and pairing the deal with a framework for reciprocal tariff reductions on about US$30.00 billion of goods on each side.

- Although the order fell short of earlier expectations for a larger deal, it still marks Boeing’s first major Chinese commitment in nearly a decade and may help ease trade frictions that had constrained its commercial prospects in the country.

- Against this backdrop, we’ll examine how renewed Chinese orders and tariff-reduction talks interact with Boeing’s existing backlog-driven investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Boeing Investment Narrative Recap

To own Boeing today, you have to believe its large commercial backlog and improving operations can eventually outweigh current losses, high debt and lingering safety concerns. The confirmed 200-jet China order and tariff framework support the backlog story, but the key near term catalyst is still consistent production and certification progress, while the biggest risk remains execution missteps that delay deliveries and keep cash flow under pressure. This week’s news helps sentiment but does not remove that core risk.

The Gilat Sidewinder inflight connectivity milestone fits this backdrop by highlighting how Boeing is trying to add value on each airframe through higher margin services and technology. While less eye catching than a headline aircraft order, factory line fit broadband capability can reinforce Boeing Global Services as a supporting catalyst alongside the China deal, especially if airlines increasingly prioritize connected cabins when deciding how to allocate future fleet spending.

Yet investors should also be aware that if quality control issues resurface at the same time as Boeing leans harder on China related growth, then...

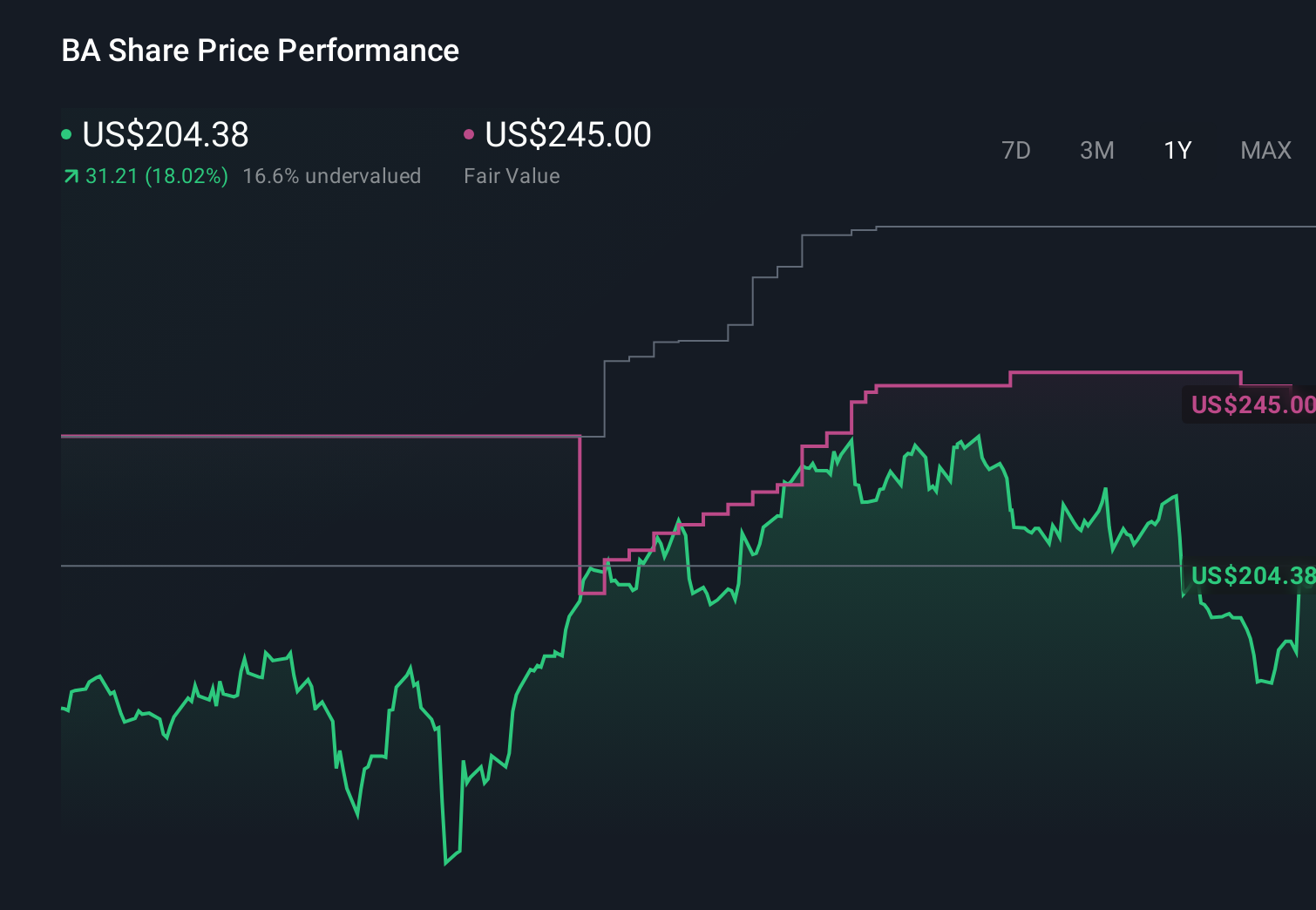

Boeing's narrative projects $125.3 billion revenue and $7.9 billion earnings by 2029. This requires 10.8% yearly revenue growth and about a $6.0 billion earnings increase from $1.9 billion today.

Uncover how Boeing's forecasts yield a $269.52 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already wary, assuming revenue growth of about 8.6 percent a year and earnings of roughly US$4.1 billion by 2029, and they focus more on structural quality control and certification risks than on trade wins like the China order, reminding you that this new deal could meaningfully reshape both the cautious and the optimistic stories from here.

Explore 6 other fair value estimates on Boeing - why the stock might be worth just $260.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.