How Delta’s Event-Driven Trans-Atlantic Flights and Service Tweaks at Delta Air Lines (DAL) Shape Its Premium Narrative

Delta Air Lines, Inc. DAL | 0.00 |

- Delta Air Lines recently disclosed insider share sale activity, outlined participation in an upcoming investor conference, adjusted short-haul in-flight services, and added temporary trans-Atlantic flights to serve football fans traveling to major matches in Madrid and Munich later this year.

- Together, these moves highlight how Delta is balancing event-driven international demand with cost-focused service changes as fuel expenses remain elevated across the airline industry.

- We’ll now examine how Delta’s special event-driven trans-Atlantic flights may influence its investment narrative around premium, international demand.

Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Delta Air Lines Investment Narrative Recap

To own Delta, you need to believe its premium, international and loyalty businesses can offset pressure in domestic main cabin demand and high fuel costs. The latest news around special event flights, short-haul service cuts and insider selling does not materially change that near term. The most important catalyst remains management’s ability to protect margins while capacity stays roughly flat, while the biggest risk is a sharper pullback in core U.S. leisure and corporate demand.

Among recent updates, Delta’s decision to end food and beverage service in economy on flights under 350 miles stands out. This move fits with the near term catalyst of margin protection as fuel expenses stay elevated, even as the airline invests in premium long haul offerings like the temporary football-related trans Atlantic flights. For shareholders, it is another small but telling example of how Delta is prioritizing cost discipline over convenience at the lower end of the cabin.

Yet even as premium demand holds up, investors should be aware that a deeper downturn in main cabin traffic could...

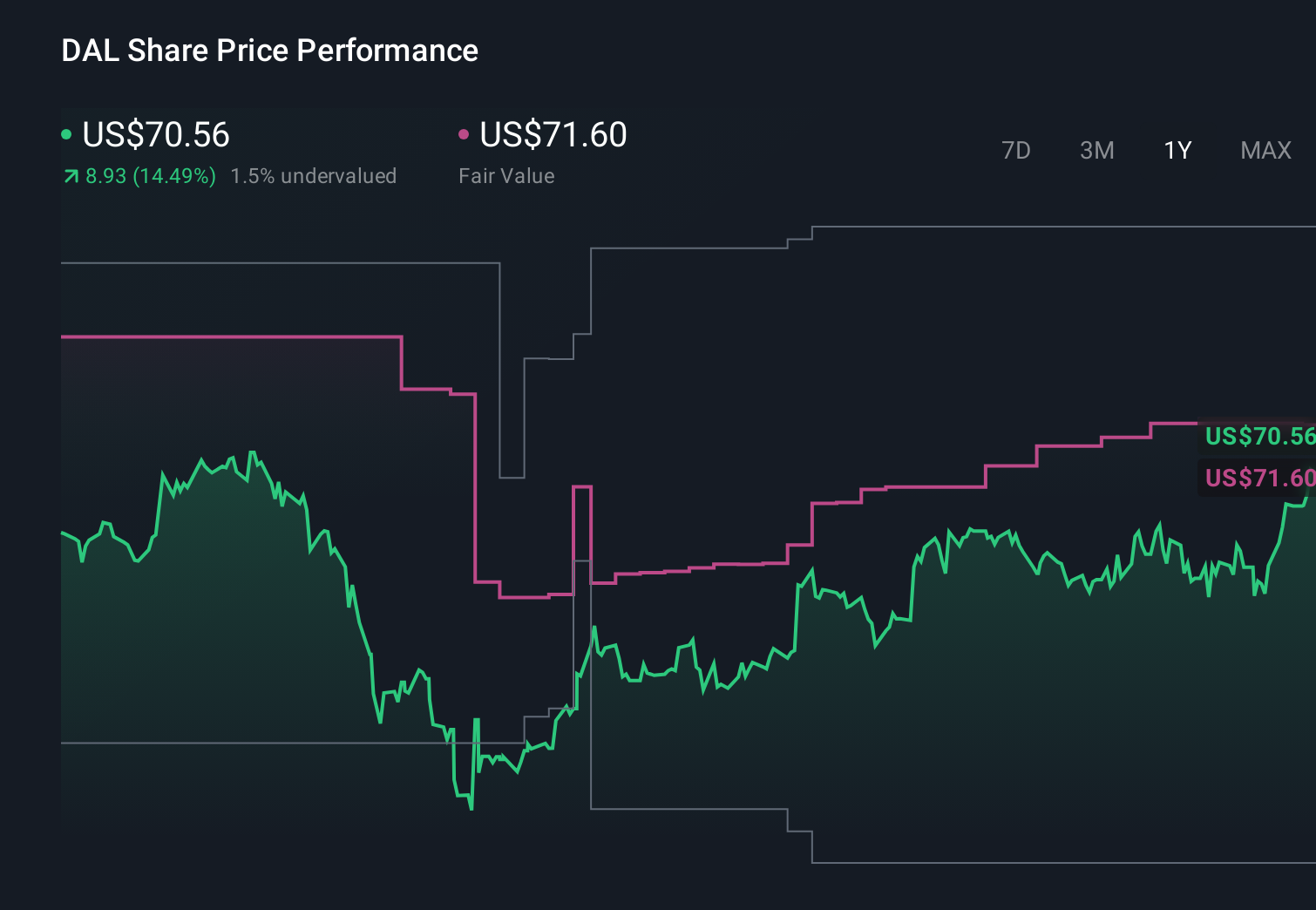

Delta Air Lines' narrative projects $72.9 billion revenue and $5.5 billion earnings by 2029.

Uncover how Delta Air Lines' forecasts yield a $79.89 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Delta could reach about US$82.1 billion in revenue and US$6.0 billion in earnings, but this premium focused growth story could look very different if event driven international strength cannot fully offset ongoing softness in domestic main cabin demand.

Explore 10 other fair value estimates on Delta Air Lines - why the stock might be worth 25% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Delta Air Lines research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Delta Air Lines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Delta Air Lines' overall financial health at a glance.

Looking For Alternative Opportunities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.