How Dividend, Buybacks and Index Exit Could Reshape Carnival’s (CCL) Capital Allocation Story

Carnival Corporation Ltd. CCL | 0.00 |

- Carnival Corporation has declared a quarterly dividend of US$0.15 per share, payable on August 28, 2026, to shareholders on record as of August 7, 2026, and recently completed a share repurchase of 15,100,000 shares for US$390,340,000.

- At the same time, Carnival finished a pier extension at its Celebration Key destination that doubles ship berthing capacity, even as the company was removed from several Russell growth indices, potentially affecting how index-tracking funds hold the stock.

- Now we’ll examine how Carnival’s new dividend, alongside its index removals, may influence the existing investment narrative for the company.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Carnival Investment Narrative Recap

To own Carnival today, you need to believe cruising remains a resilient way to spend leisure dollars and that the company can convert strong demand into sustainable cash generation despite high debt and volatile costs. The new US$0.15 quarterly dividend and recent index removals do not materially change the near term picture: investors still appear focused on fuel costs as the key short term swing factor and balance sheet risk as the main overhang.

The most relevant update here is Carnival’s completed share repurchase of 15,100,000 shares for US$390,340,000, alongside its dividend declaration. Together, these moves point to a company allocating more cash to shareholders just as it brings Celebration Key’s expanded capacity online, which could be important for investors who see capital returns as part of the thesis while watching how geopolitical tensions and fuel prices affect earnings resilience.

Yet behind the dividend headline, investors should also be aware of the pressure that rising fuel and financing costs could still place on Carnival’s...

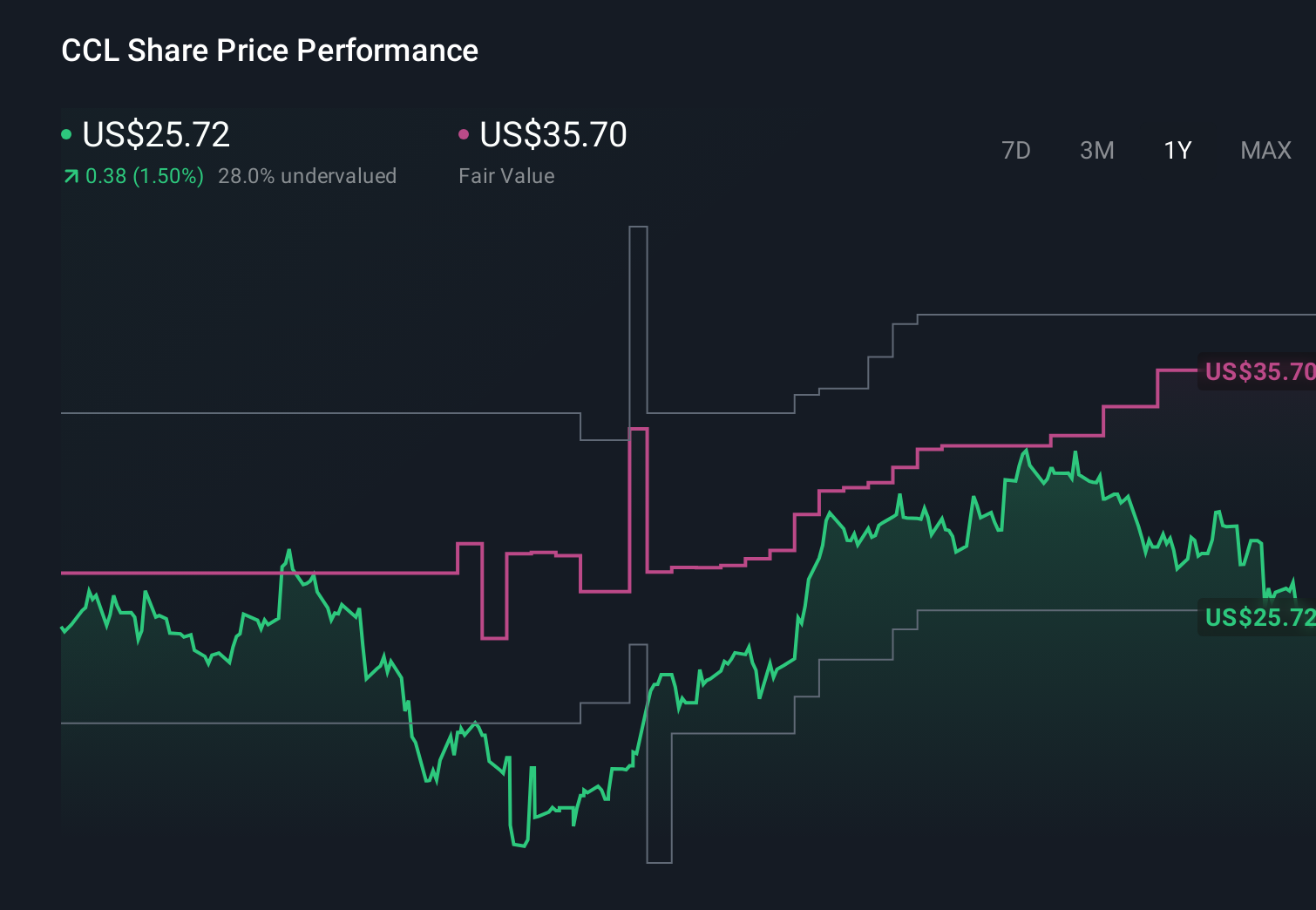

Carnival's narrative projects $30.5 billion revenue and $4.0 billion earnings by 2029. This requires 3.8% yearly revenue growth and about a $0.9 billion earnings increase from $3.1 billion today.

Uncover how Carnival's forecasts yield a $35.60 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in around US$31.0 billion of revenue and US$4.4 billion of earnings by 2029, but compared with the baseline focus on debt and fuel costs, they lean far harder on the idea that margin expansion and loyalty-driven spending will outweigh those risks, which shows how differently you and other investors might interpret the same dividend and index changes.

Explore 10 other fair value estimates on Carnival - why the stock might be worth just $28.70!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carnival research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Carnival research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.