How Does Exact Sciences Stack Up After 78% YTD Rally and New Clinical Study News?

Exact Sciences Corporation EXAS | 0.00 |

- Ever wondered if Exact Sciences is truly worth its current price, or if the market is overlooking a hidden gem? You are not alone, and we are about to dig into what is really driving the numbers behind this biotech stock.

- Shares have surged 59.8% in the last month and 17.7% just in the past week, with a standout 78.2% gain year-to-date. This indicates renewed optimism and some big shifts in how investors are viewing the company’s prospects.

- Fueling this positive sentiment, there has been a string of headlines around Exact Sciences’ continued progress in expanding its cancer diagnostics portfolio and the rollout of new clinical studies, drawing attention from both analysts and the healthcare sector at large.

- Despite these moves, Exact Sciences currently scores a 3 out of 6 on valuation checks. This suggests there is more to the story, so let us break down the valuation math and, at the end, explore an even better way to judge if this company is really as valuable as the market thinks.

Approach 1: Exact Sciences Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting those projections back to today's dollars. This approach offers a grounded view of what the company could realistically be worth based on its ability to generate free cash flow rather than just market hype or short-term moves.

For Exact Sciences, the most recent reported Free Cash Flow was $222 million. Analysts expect this figure to reach $346 million in 2026, increasing further to over $1.3 billion by 2035, although estimates beyond five years are extrapolated and carry some uncertainty. All cash flow projections are made in USD. This long-term perspective allows investors to see how growth in clinical diagnostics and expanding market adoption could translate into significant cash generation over time.

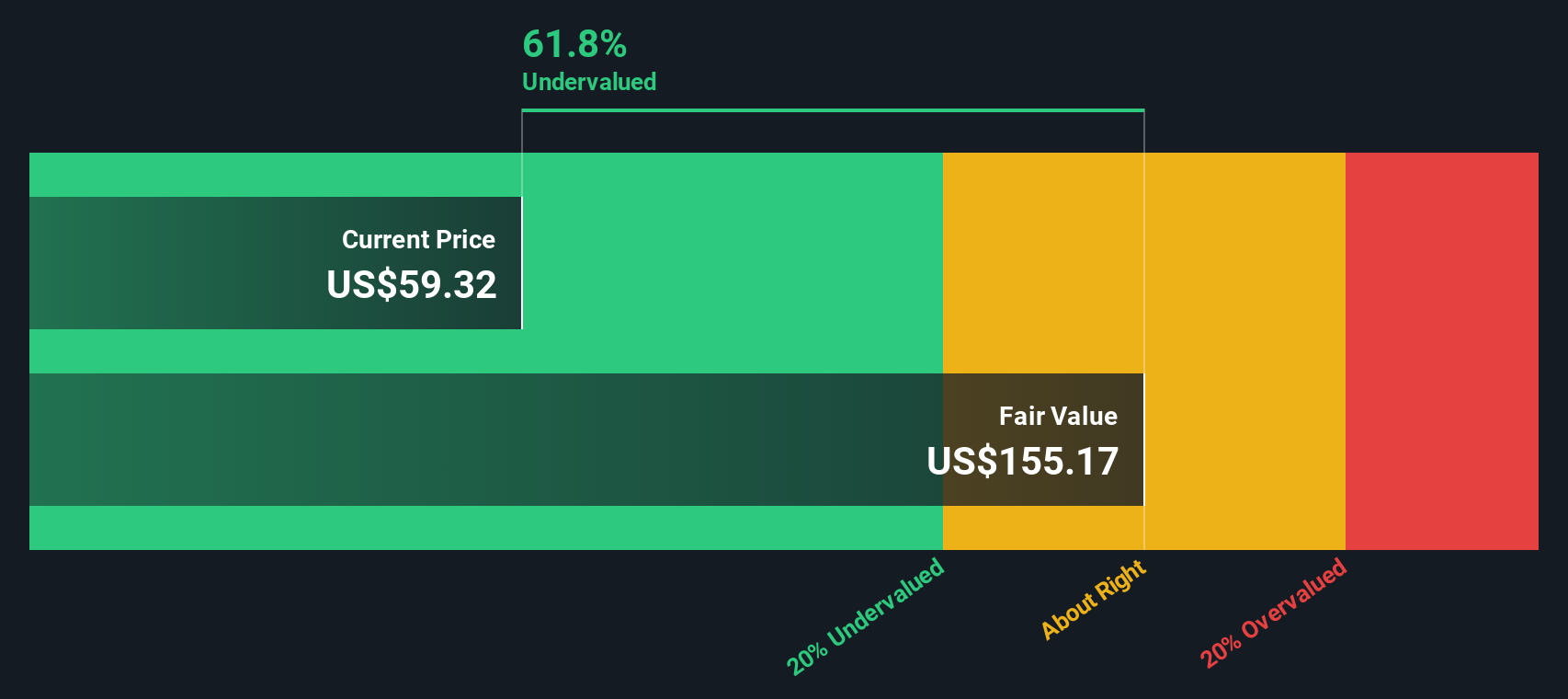

Based on these cash flows, the DCF model calculates an intrinsic value of $118.68 per share, which is about 14.5% higher than the current market price. This suggests that the stock may be undervalued relative to its future growth potential according to this method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Exact Sciences is undervalued by 14.5%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

Approach 2: Exact Sciences Price vs Sales

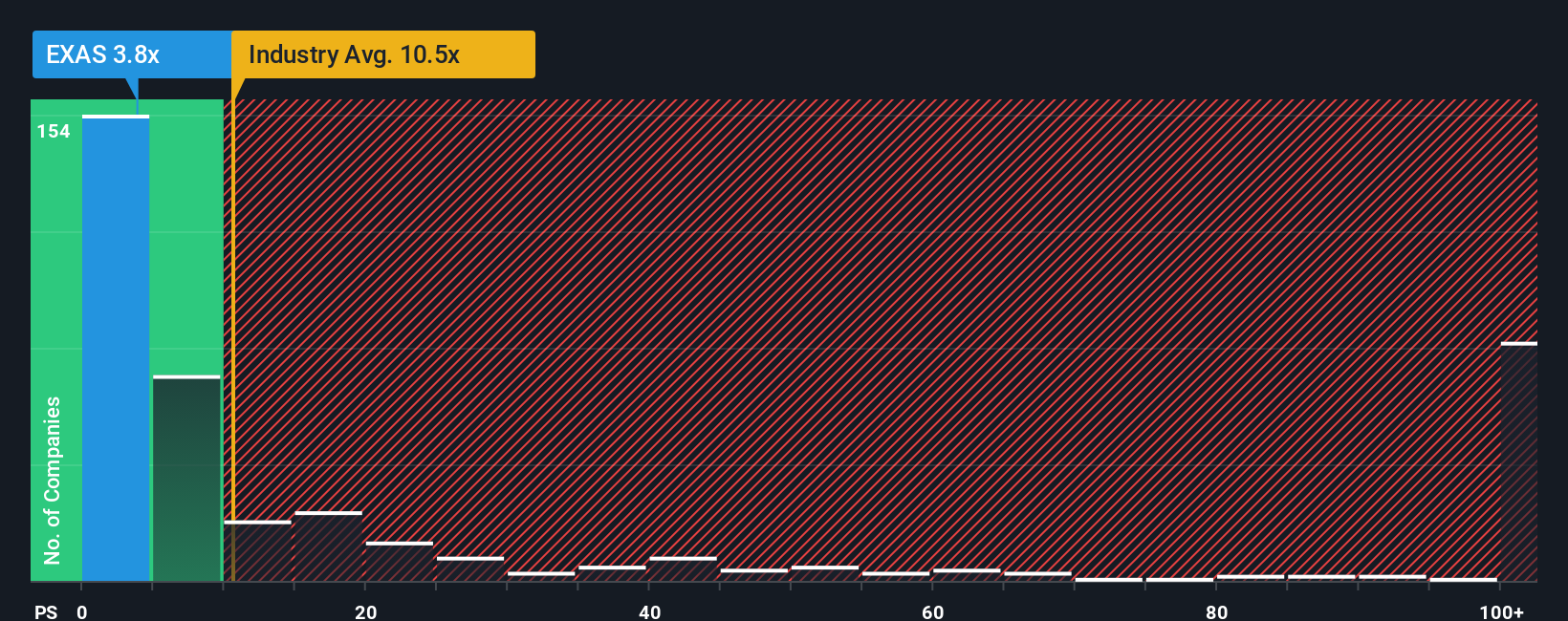

The Price-to-Sales (P/S) ratio is a favored metric for valuing companies like Exact Sciences, especially when profits are still developing but revenue growth is robust. This approach provides insight into how much investors are willing to pay for each dollar of the company’s sales. This is particularly important in the biotech sector, where rapid growth and reinvestment often mask underlying profitability.

When future growth prospects are high or risk is lower, investors typically accept a higher P/S multiple. Conversely, heightened risk or slower anticipated growth leads the market to pay less for a given amount of sales.

Currently, Exact Sciences trades at a 6.24x P/S multiple. For context, the average P/S for Biotechs is 13.12x, while its closest listed peers sit at an average of 5.47x. However, looking at these numbers alone can be misleading if they do not account for the company’s unique growth profile or risk factors.

This is where Simply Wall St’s proprietary Fair Ratio comes in. The Fair Ratio for Exact Sciences, calculated at 7.16x, incorporates not only industry and peer benchmarks but also factors such as growth expectations, profit margins, risk, and the company’s size. This offers investors a more nuanced view of what the appropriate multiple could be.

With Exact Sciences’ current P/S ratio slightly below the Fair Ratio, this method suggests the market may be undervaluing its growth outlook and strengths.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1432 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Exact Sciences Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your personal story or perspective on a company. It connects your beliefs about a business's future with financial forecasts and, ultimately, your view of fair value. Instead of relying solely on analyst estimates or one-size-fits-all models, Narratives empower you to bring your own logic and expectations about Exact Sciences (such as assumptions around revenue growth, profit margins, or competitive risks) directly into the valuation process.

Narratives make investing more approachable by linking company stories to actual numbers and projected outcomes, helping you see how your assumptions translate to a current fair value versus today’s market price. Available within Simply Wall St’s Community page, which is used by millions of investors, Narratives update dynamically as news or earnings emerge. This keeps your analysis relevant in real time and makes it simpler to know if now is the right time to buy or sell.

For example, some investors believe Exact Sciences could be worth as much as $82 if momentum in cancer screening and new product launches continues. Others see a more cautious value near $50 if competitive and execution risks play out. Narratives let you test both stories side by side, so you can make smarter, more confident decisions based on your view of the company’s future.

Do you think there's more to the story for Exact Sciences? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.