How Does Mastercard Stack Up After Its New Global Bank Partnerships?

Mastercard Incorporated Class A MA | 491.65 | -1.60% |

Thinking about what to do with your Mastercard shares, or whether now might be the moment to jump in? You're not alone. Mastercard’s stock has captured plenty of attention lately, especially given its string of long-term gains. While the past month saw a slight dip of 2.2%, the stock still boasts a solid 9.4% rise year-to-date. Step back even further, and Mastercard’s performance is hard to ignore: up 11.9% over the last year, an impressive 82.0% over three years, and a doubling of value over five years with a 101.7% return.

Mastercard’s steady climb can be traced partly to ongoing momentum in global payments, as well as recent headlines about new partnerships with major banks aiming to simplify cross-border transactions. As consumers and businesses shift further into digital payments, investors have started viewing companies like Mastercard as both growth stories and pillars of fintech stability. This has shaped risk perceptions and fueled debate about where fair value really lies.

But with the share price recently closing at $571.36, the big question is whether Mastercard can justify its pricey-looking valuation. Interestingly, according to our valuation checks, Mastercard is undervalued in just 1 out of 6 categories, earning a value score of 1. That may sound underwhelming, but the nuances of valuation can be surprisingly revealing. Next, let’s dig into exactly how Mastercard stacks up across traditional value metrics before exploring whether there might be a smarter, more holistic way to gauge what this stock is truly worth.

Mastercard scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Mastercard Excess Returns Analysis

The Excess Returns valuation model focuses on how much value a company generates by producing returns on its invested capital above its cost of equity. For Mastercard, this approach highlights its ability to turn every invested dollar into significantly more in actual profits than it costs the company to raise and use capital. This reflects Mastercard's status as a world-class financial franchise.

In concrete terms, Mastercard’s Book Value stands at $8.67 per share, while its Stable EPS is estimated at $28.88 per share, according to a blend of future Return on Equity predictions from 12 analysts. The Cost of Equity is relatively low at $1.10 per share, meaning Mastercard’s core operations produce an Excess Return of $27.78 per share. Its average Return on Equity is a striking 195.03%, and analysts expect its Stable Book Value to rise towards $14.81 per share, based on projections from 8 analysts.

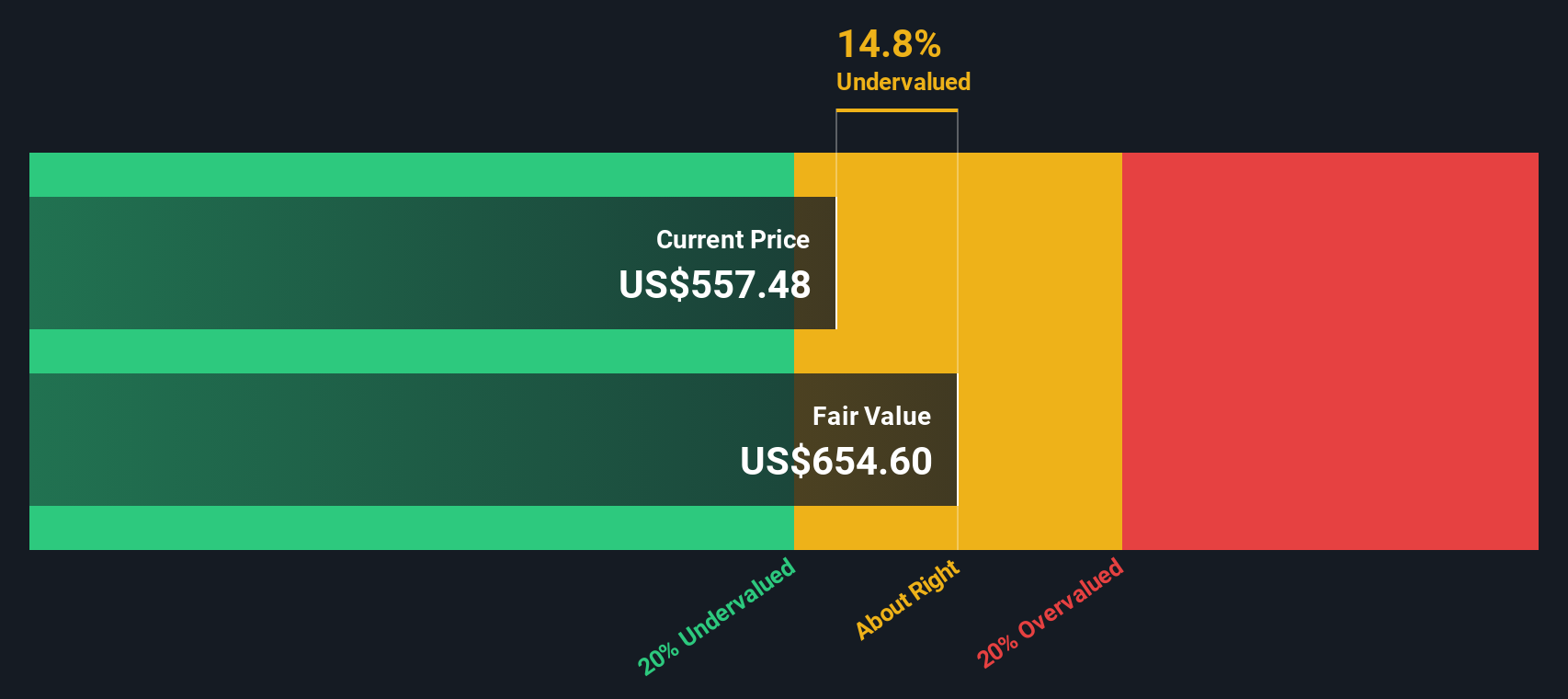

Considering these figures, the Excess Returns model estimates Mastercard's intrinsic value at $651.10 per share. With its recent closing price at $571.36, this suggests the stock is about 12.2% undervalued at current levels.

Result: UNDERVALUED

Our Excess Returns analysis suggests Mastercard is undervalued by 12.2%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Mastercard Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely accepted valuation tool for profitable companies like Mastercard, as it connects a company’s share price to its actual bottom-line earnings. Since Mastercard is both established and highly profitable, using the PE ratio helps investors gauge whether they are paying a reasonable price for its future growth and stability.

Growth expectations and risk play major roles in what PE ratio is considered “fair.” Companies with faster expected earnings growth or lower risk tend to justify higher PE multiples, while less robust or riskier profiles warrant lower ones. Mastercard currently trades at a PE of 38.0x, which is notably higher than the industry average of 16.2x and the peer average of 20.7x. At first glance, this premium might raise eyebrows, but it often signals the market’s confidence in Mastercard’s future prospects or its competitive advantages.

To get a more precise read, Simply Wall St’s Fair Ratio weighs not just growth, but also profit margins, risk factors, market cap and industry dynamics to arrive at a custom benchmark. This makes it a more insightful metric than simple peer or industry comparisons. Mastercard’s Fair Ratio stands at 23.0x. Comparing this to the current PE of 38.0x, the stock appears to be priced significantly above what would be expected, even after accounting for its robust profile. This suggests Mastercard may be trading at a valuation above what its underlying fundamentals warrant.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Mastercard Narrative

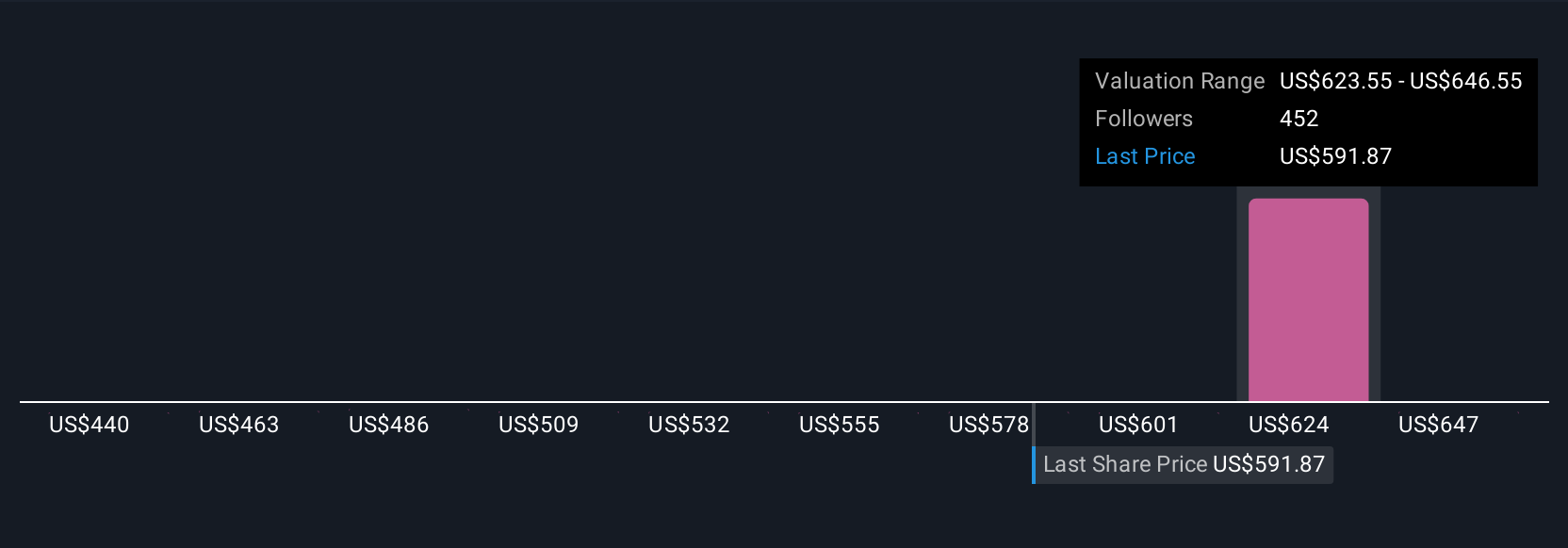

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your personal story about a company, connecting your view of Mastercard’s future—things like revenue growth, profit margins, and risks—to a financial forecast and ultimately to a fair value. Narratives make investing more approachable by letting you clearly express why you think Mastercard is worth a certain price, instead of just relying on static metrics. On Simply Wall St’s Community page, millions of investors use Narratives to instantly compare their estimated fair value to the current price, helping them decide when to buy or sell. These Narratives update dynamically as new news, earnings, or trends emerge, keeping your decision-making fresh and relevant. For example, one investor may think Mastercard’s digital expansion justifies a high price target of $690, while another, more cautious view could set fair value at $520. These are different perspectives, grounded in distinct stories and forecasts. Narratives empower you to invest with both your insights and the numbers in mind, all in one approachable tool.

Do you think there's more to the story for Mastercard? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.