How Does Recent Analyst Downgrade Affect the On Running Valuation in 2025?

On Holding AG Class A ONON | 33.03 | -5.00% |

Thinking about what to do with On Holding stock? You are not alone. Whether you are a long-term believer in the brand's running revolution or just curious about the recent price action, now could be a moment to revisit your strategy. In the last seven days, On Holding shares inched up by 1.1%, which is not dramatic but notable given recent headwinds. Over 30 days, they are down 1.7%, and if you zoom out further, the picture gets choppier. Year-to-date, the stock has shed 23.8%, and over the past year, it is down 14.6%. Yet, despite these dips, step back even further and the long-run performance is striking, with shares up a remarkable 148.3% over three years.

Much of this ride has reflected broader market volatility and shifts in how investors perceive risk within growth stocks like On Holding. The company has captured significant attention, especially as active lifestyle brands continue to ride cultural tailwinds, but the near-term action is not just noise. Investors seem to be re-evaluating both growth prospects and valuation.

On that front, here is a quick snapshot: On Holding’s valuation score sits at just 1 out of 6, suggesting the stock looks undervalued by only one of the standard checks in our framework. But numbers alone do not tell the whole story. Let us dive into how those valuation approaches stack up, and stick around, because toward the end of this article we will cover a smarter way to look at what this score really means for your investing decisions.

On Holding scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: On Holding Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them back to their present value. This approach helps investors gauge what the company is theoretically worth today based on anticipated future performance, rather than just current financials or sentiment.

For On Holding, the latest reported Free Cash Flow is CHF 330.8 million. Analysts supply forecasts up to five years out, while projections beyond this period rely on Simply Wall St's extrapolations. By 2029, Free Cash Flow is projected to reach CHF 591 million, and estimates continue upward for the next decade. All figures are reported in Swiss Francs (CHF), which is On Holding's reporting currency.

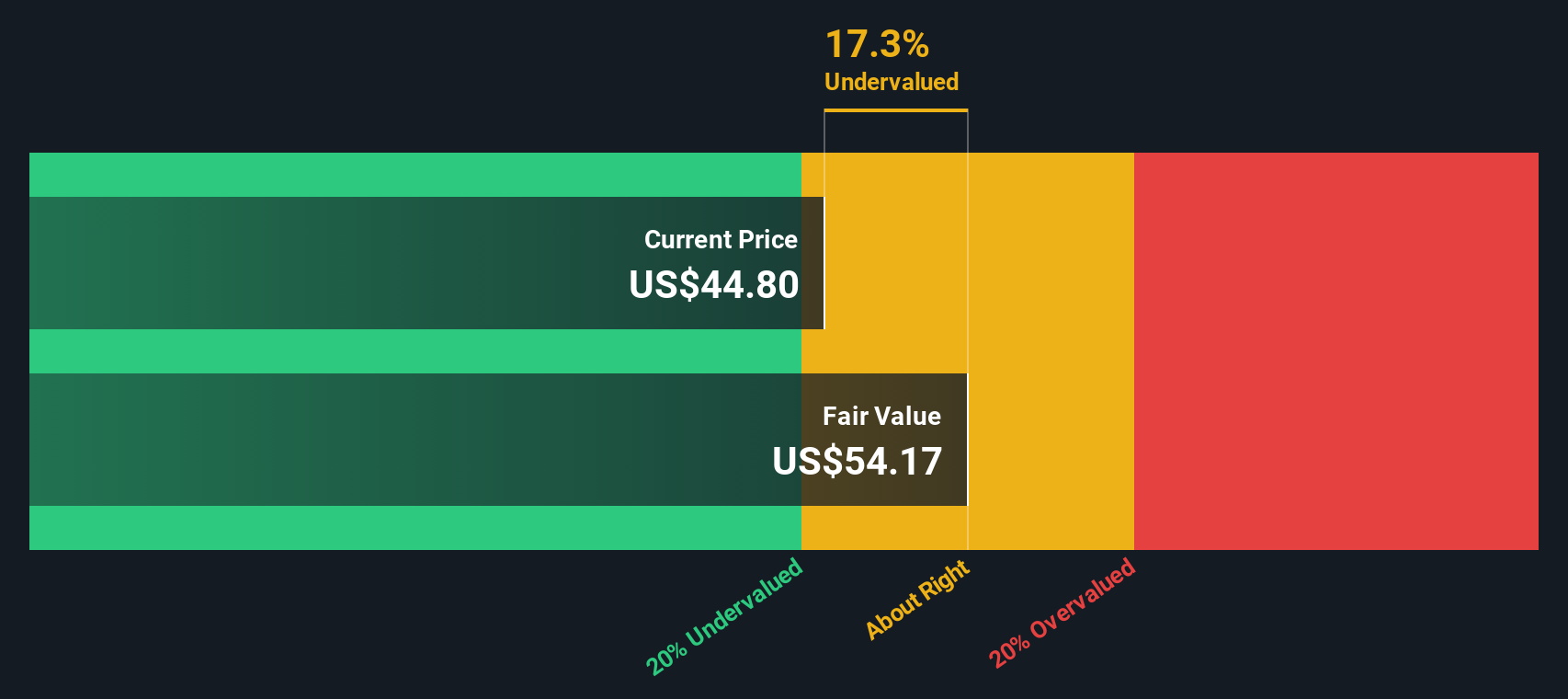

Based on these projections and the 2 Stage Free Cash Flow to Equity model, On Holding’s DCF fair value comes in at $36.04 per share. Compared to the current share price, the DCF model implies the stock is about 17.0% overvalued. This suggests the market is pricing in stronger or faster growth than what is currently justified by cash flows alone.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests On Holding may be overvalued by 17.0%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: On Holding Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies because it captures how much investors are willing to pay for each dollar of current earnings. For growth-oriented brands like On Holding that have shown profits, PE makes it easier to compare valuation across similar firms.

An appropriate or “normal” PE ratio depends on expectations for the company’s future growth, its risk profile, and general market sentiment. Higher growth rates or lower risk typically justify higher PE multiples, while sluggish growth and elevated risk mean a lower multiple is warranted.

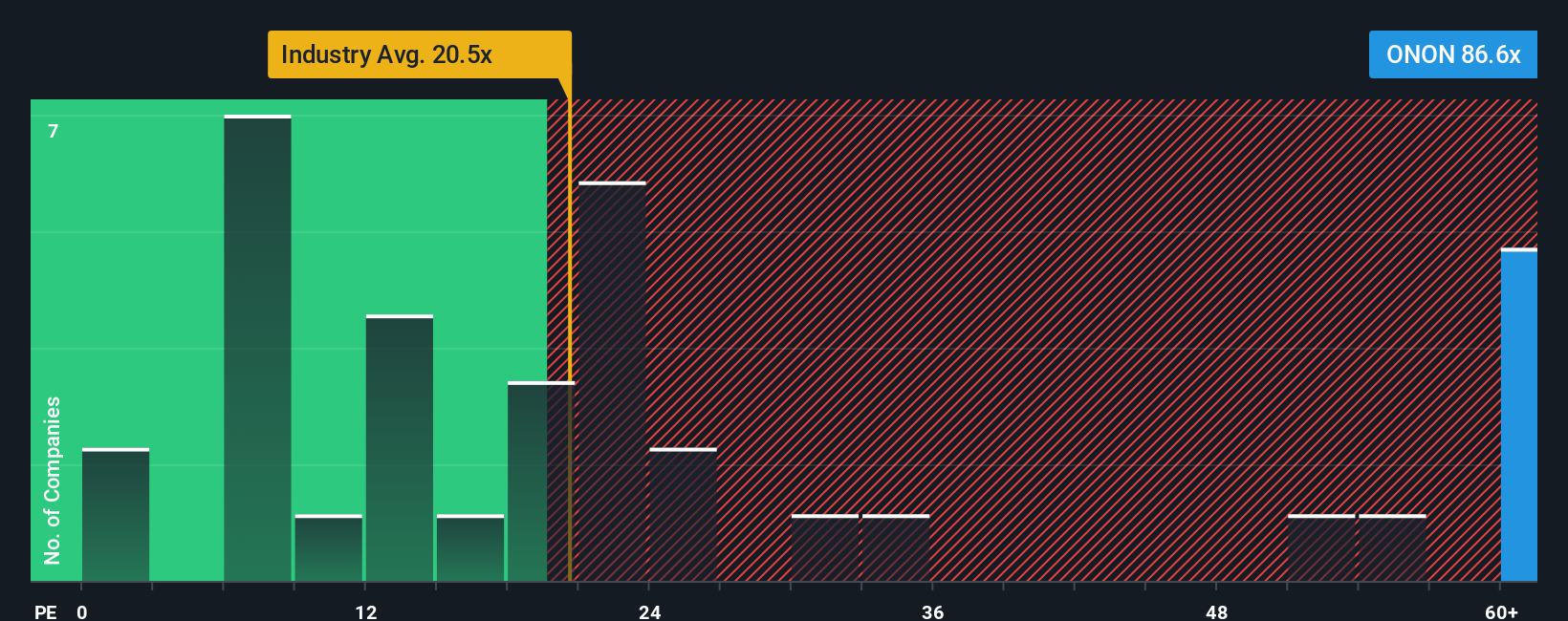

Currently, On Holding trades at a PE ratio of 81.2x, which is significantly higher than both the peer group average of 21.0x and the luxury industry average of 19.5x. This suggests that the market is pricing in exceptional future growth for the company. However, rather than only measuring against peers or industry, Simply Wall St calculates a “Fair Ratio” in this case, 33.0x which considers On Holding’s unique mix of expected earnings growth, profit margins, size, industry characteristics, and risk factors.

This proprietary Fair Ratio gives a more tailored benchmark for valuation than blunt peer or industry averages, making it especially useful for outliers or rapidly changing businesses. Comparing the Fair Ratio of 33.0x to the actual PE of 81.2x shows the stock’s current price embeds a much rosier outlook than justified by its fundamentals and risk, signaling a material valuation premium.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your On Holding Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Narratives are not just numbers; they are the story you tell about a company’s future, linking your perspective and assumptions, such as growth, margins, and fair value, to a financial forecast. This approach makes investing more personal and actionable, bringing context and clarity to what you believe might happen next.

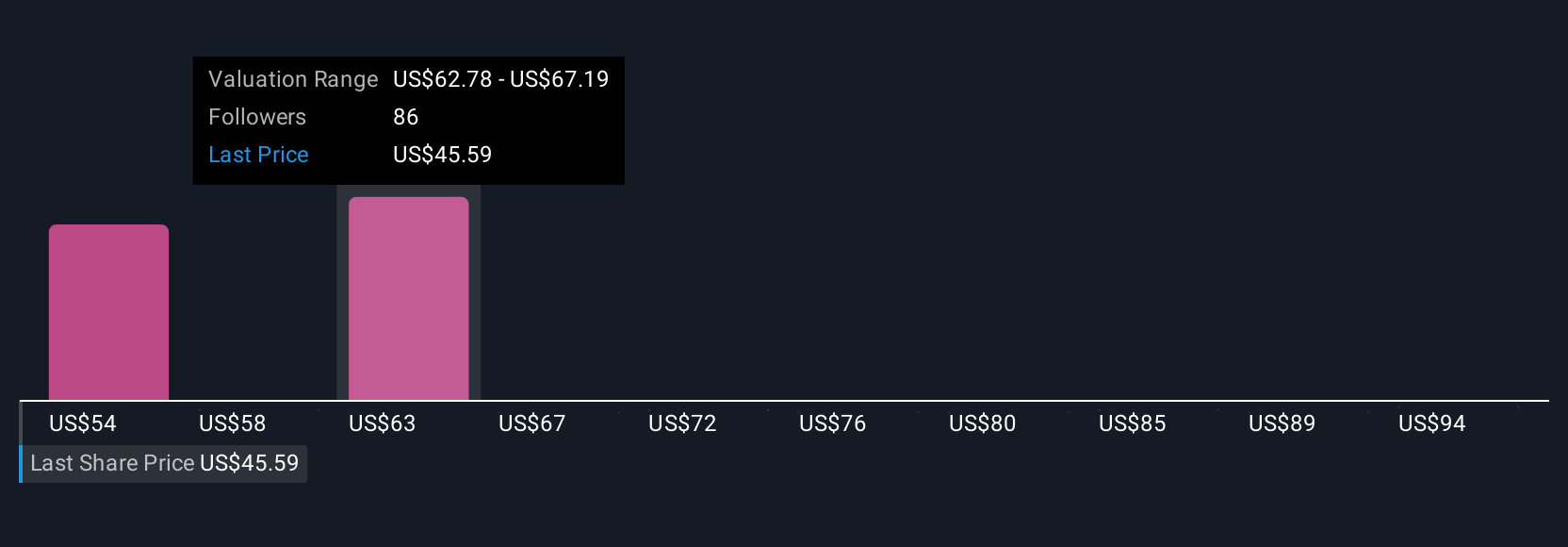

With Narratives, available to every investor on Simply Wall St’s Community page, anyone can connect their view of On Holding’s business momentum with concrete revenue and earnings forecasts, and see how their fair value stacks up against today’s price. Narratives update automatically as new information, news, or earnings are released, making sure your story stays relevant as circumstances evolve. For example, the most bullish investors recently forecast a price target of CHF79.18, expecting sustained global expansion and higher margins. The most cautious see fair value at just CHF39.82 due to concerns around premium pricing and competition, illustrating how a Narrative expresses your unique view in numbers. Comparing your Narrative-based fair value to On Holding’s market price helps you decide when the stock is worth a buy, a hold, or a pass, with greater confidence and transparency.

Do you think there's more to the story for On Holding? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.