How Enterprise’s Conference Spotlight On Midstream Scale And Income Profile At EPD Has Changed Its Investment Story

Enterprise Products Partners L.P. EPD | 37.57 | +0.37% |

- In late February and early March 2026, Enterprise Products Partners L.P. participated in multiple investor conferences, including THRIVE Energy in Houston and Jefferies’ Power, Utilities & Clean Energy event in New York, highlighting its extensive midstream energy infrastructure and recent project additions.

- These appearances gave management a platform to underscore Enterprise’s long record of distribution growth, A- credit rating, and expanding NGL and export capabilities, reinforcing its profile as a defensively positioned income-focused partnership.

- Now we will examine how Enterprise’s recent project expansions and conference messaging affect the existing investment narrative around distributions and growth.

Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners today, you have to be comfortable with a midstream partnership built around fee-based cash flows, a long history of distribution growth, and a sizable debt load that supports large-scale projects. The recent conference appearances do not appear to change the near term picture much, with the main upside catalyst still tied to new assets ramping volumes, while key risks remain around Permian producer activity and export demand sensitivity.

Among the recent updates, Enterprise’s plan to invest US$3.1 billion to US$3.5 billion in organic capital projects in 2026 looks most relevant. These investments, particularly in Permian infrastructure and export capabilities, sit right at the center of the volume driven growth story that underpins distribution stability, but they also intersect with the existing risk that weaker producer activity or shifting tariffs could leave new capacity underused.

Yet against this backdrop, investors should still be aware that concentrated exposure to Permian producer behavior and export markets could...

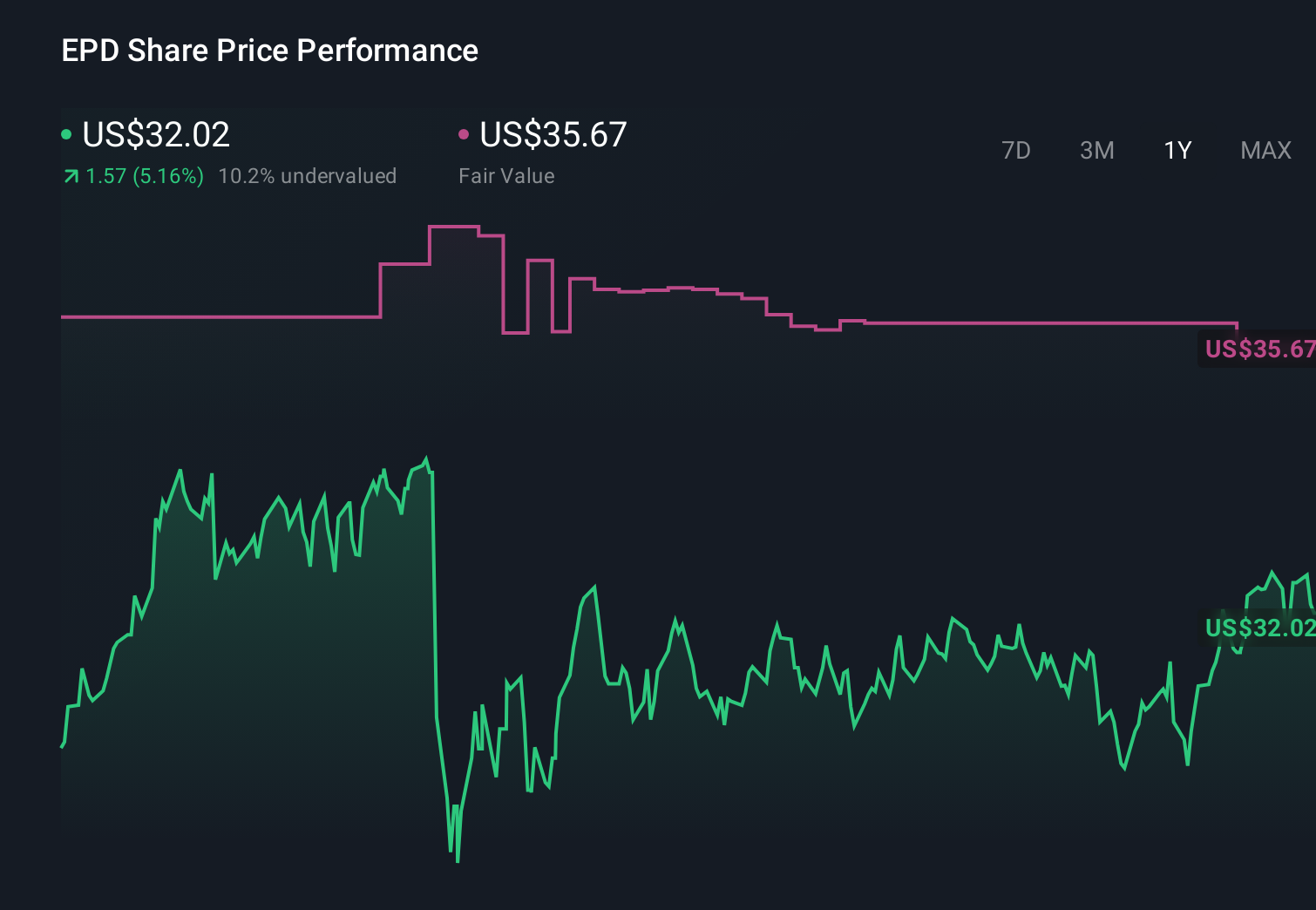

Enterprise Products Partners' narrative projects $53.5 billion revenue and $6.6 billion earnings by 2028. This assumes revenue will decline by 0.8% per year and an earnings increase of about $0.8 billion from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $36.65 fair value, in line with its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community see fair value for Enterprise Products Partners between US$34 and about US$86.65, underscoring how widely opinions can differ. When you set those views against the company’s heavy 2026 capital program in the Permian, it raises real questions about how volume trends and tariffs might shape future cash flows and distributions.

Explore 8 other fair value estimates on Enterprise Products Partners - why the stock might be worth 9% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

No Opportunity In Enterprise Products Partners?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.