How GM’s Defense Pivot and Battery Bet Could Reshape General Motors’ (GM) Risk Profile

General Motors Company GM | 0.00 |

- In recent days, General Motors has been reported to be in talks with Lockheed Martin about manufacturing components for weapons systems through its GM Defense unit, while also managing issues ranging from a limited airbag recall and a new dealer lawsuit to a ratified supplier labor contract and an investment in sodium‑ion battery startup Peak Energy.

- Taken together, these developments highlight GM’s push to diversify into defense and advanced energy storage while continuing to modernize its vehicle development and address operational and legal challenges.

- Next, we’ll examine how GM’s potential defense manufacturing collaboration with Lockheed Martin could influence the company’s investment narrative and risk profile.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

General Motors Investment Narrative Recap

To own GM today, you have to believe it can use its scale in trucks and EVs, plus software and services, to grow earnings while managing quality, regulatory and capital intensity pressures. The Lockheed Martin talks, airbag recall, dealer lawsuit and Peak Energy investment do not materially change the near term focus on improving margins and executing on electrification, but they add fresh angles to GM’s diversification and operational risk picture.

The potential Lockheed Martin collaboration through GM Defense is the clearest tie to this news, because it introduces a possible new revenue stream that does not rely on consumer auto demand. For investors watching catalysts around EV profitability and software growth, even a modest defense manufacturing footprint could slightly rebalance GM’s mix of earnings drivers, while also adding exposure to government procurement cycles and defense related policy risk.

Yet behind GM’s push into defense and new batteries, investors should also be aware of the risk that...

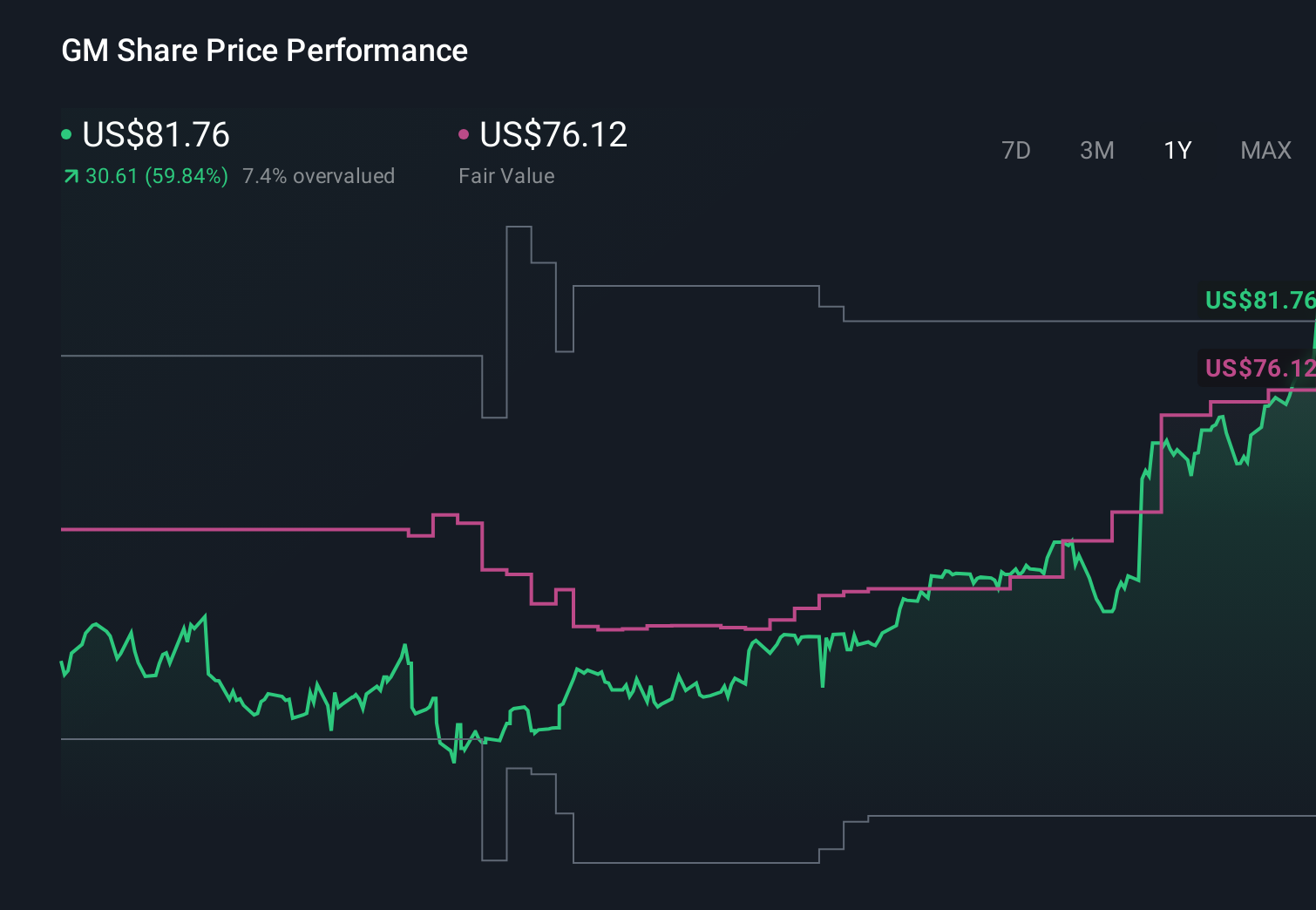

General Motors' narrative projects $195.5 billion revenue and $10.8 billion earnings by 2029. This requires 1.9% yearly revenue growth and about a $8.4 billion earnings increase from $2.4 billion today.

Uncover how General Motors' forecasts yield a $94.81 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much harsher picture, assuming revenue only reaches about US$188.5 billion and earnings about US$10.2 billion by 2029, and they worry that if GM cannot reduce EV costs quickly enough in the face of aggressive competitors, even moves like the Lockheed Martin talks might not offset margin pressure.

Explore 8 other fair value estimates on General Motors - why the stock might be worth 19% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your General Motors research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free General Motors research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate General Motors' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 32 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.