How Insider Option Exercise Amid Margin Pressure At Paychex (PAYX) Has Changed Its Investment Story

Paychex, Inc. PAYX | 0.00 |

- Earlier this week, Paychex director Joseph M. Velli exercised options on 10,220 shares at US$60.59 each, increasing his direct holding to 89,564 shares as the options neared their 10‑year expiration, while separate coverage highlighted slower revenue growth and rising costs pressuring operating margins.

- While this insider exercise was not accompanied by open‑market sales, the combination of margin compression and moderating demand raises fresh questions about Paychex’s operational efficiency and competitive position versus software peers.

- We’ll now examine how concerns about slowing revenue growth and margin pressure may influence Paychex’s existing investment narrative and outlook.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Paychex Investment Narrative Recap

To own Paychex, you need to believe small and midsize businesses will keep relying on its payroll and HR platforms, even as competition from software peers intensifies. The latest option exercise by director Joseph M. Velli is largely administrative and does not materially affect the near term catalyst, which is management’s ability to stabilize margins as costs outpace revenue growth. The biggest current risk remains that moderating demand and higher expenses further erode profitability.

The most relevant recent announcement here is Paychex’s Q3 2026 report, which showed revenue growth alongside compressed net margins versus the prior year. That pattern lines up with concerns around slower demand and rising costs, and it puts more weight on whether new AI tools and platform enhancements can eventually offset margin pressure. How Paychex balances investment in technology with expense control could prove critical for the next phase of the story.

Yet beneath these headline numbers, there is a risk around client price sensitivity that investors should be aware of, particularly if smaller deal sizes and lower bundle selection...

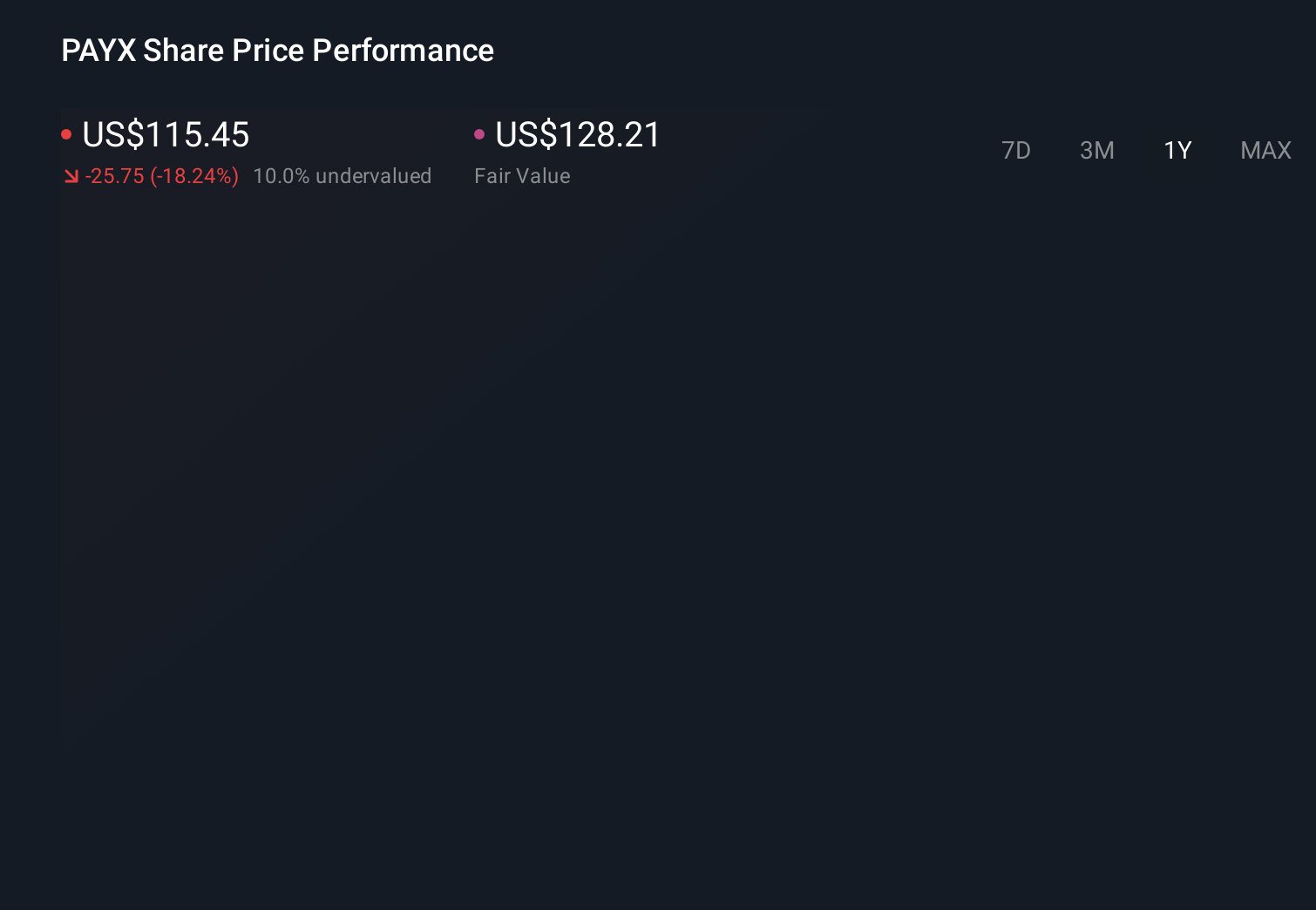

Paychex's narrative projects $7.5 billion revenue and $2.3 billion earnings by 2029. This requires 5.9% yearly revenue growth and a roughly $0.7 billion earnings increase from $1.6 billion today.

Uncover how Paychex's forecasts yield a $100.93 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$7.8 billion and earnings US$2.5 billion, which looks very different if smaller, more price sensitive client deals and this latest margin pressure prompt a rethink of how far Paychex’s profitability can really stretch.

Explore 6 other fair value estimates on Paychex - why the stock might be worth just $90.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Paychex research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.