How Investors Are Reacting To Bank of America (BAC) Q1 Beat, New Funding Moves and Tech Push

Bank of America Corp BAC | 0.00 |

- Earlier in May 2026, Bank of America reported Q1 results that exceeded analyst expectations for both revenue and GAAP EPS, while also continuing to expand its fixed-income funding with multiple new senior unsecured note offerings across a range of maturities and coupons.

- These developments, combined with increased attention on the bank’s digital platform and its role in broader themes such as AI-driven power demand and major philanthropic partnerships like the Boston Marathon, highlight how Bank of America is positioning itself across funding, technology, and brand visibility.

- With Bank of America’s stronger-than-expected Q1 earnings now on the table, we’ll examine how this performance reshapes its investment narrative.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Bank of America Investment Narrative Recap

To own Bank of America, you need to believe in a large, diversified bank that can steadily convert its scale, digital capabilities, and balance sheet into consistent earnings, even as growth expectations remain moderate and return on equity stays below 20%. The recent Q1 beat and new fixed-income issuance do not materially change the key near term catalyst of digital and AI driven efficiency gains, nor the biggest risk around funding costs and credit quality if economic conditions weaken.

The recent series of senior unsecured note offerings, with fixed coupons ranging from 4.4% to 6.0% across maturities out to 2046, is most relevant here because it shows Bank of America actively refreshing its funding stack while continuing large buybacks and dividends. For investors focused on catalysts like digital investment and disciplined balance sheet management, this new issuance sits alongside the COMPUTEX tech event and recent AI and nuclear energy research as part of how the bank is framing its future earnings engine.

Yet investors should also consider how rising competition for deposits could pressure funding costs and net interest income just as...

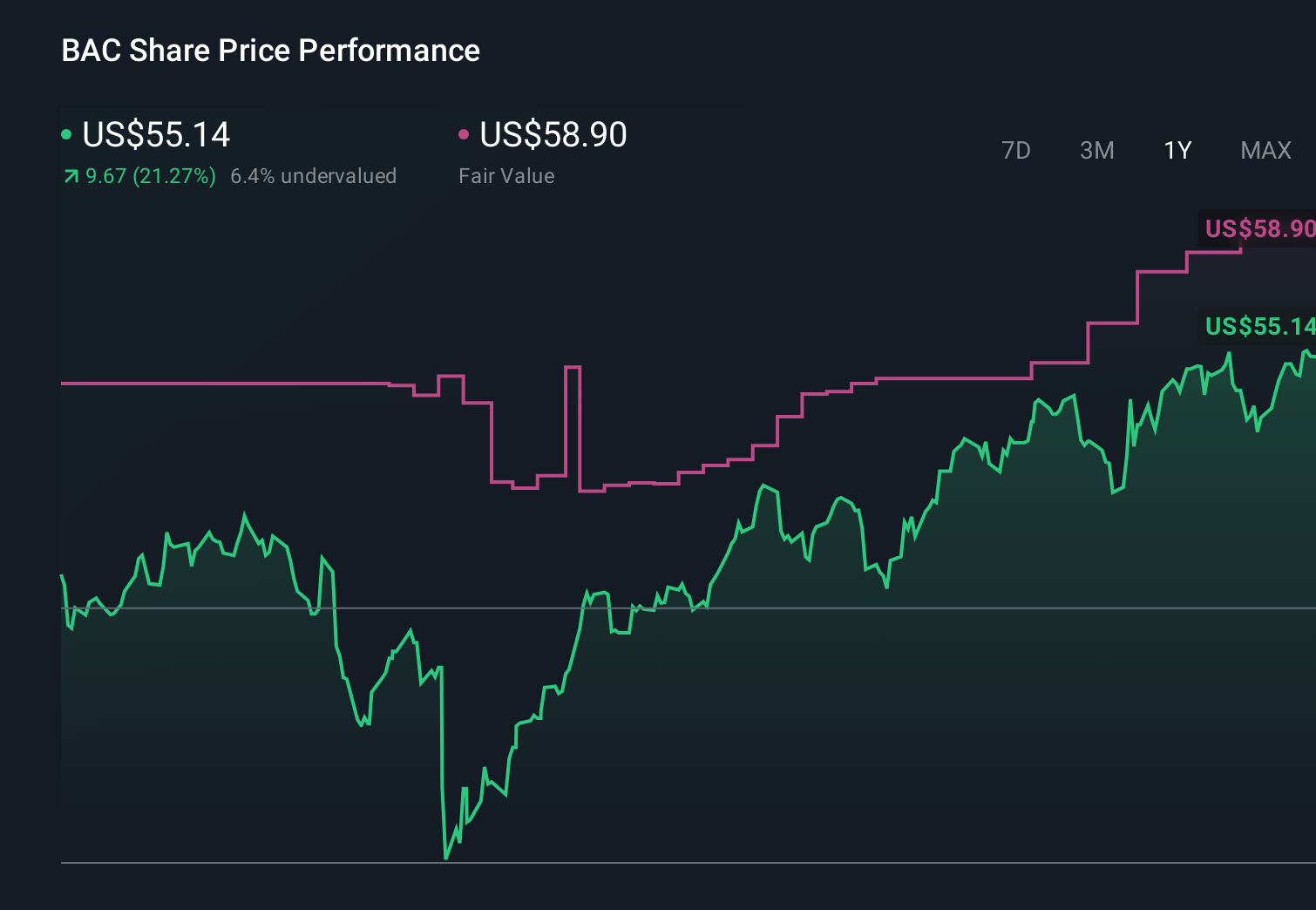

Bank of America's narrative projects $133.8 billion revenue and $36.7 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $6.4 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $62.98 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently value Bank of America between US$58.69 and US$67.64 per share, underscoring how far opinions can stretch. You should weigh those views against the risk that funding costs and credit quality could shift with broader economic conditions, and explore how different assumptions on these factors change the bank’s potential performance.

Explore 5 other fair value estimates on Bank of America - why the stock might be worth just $58.69!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.