How Investors Are Reacting To Baxter International (BAX) Mounting Earnings Pressure And Questions On Core Profit Engines

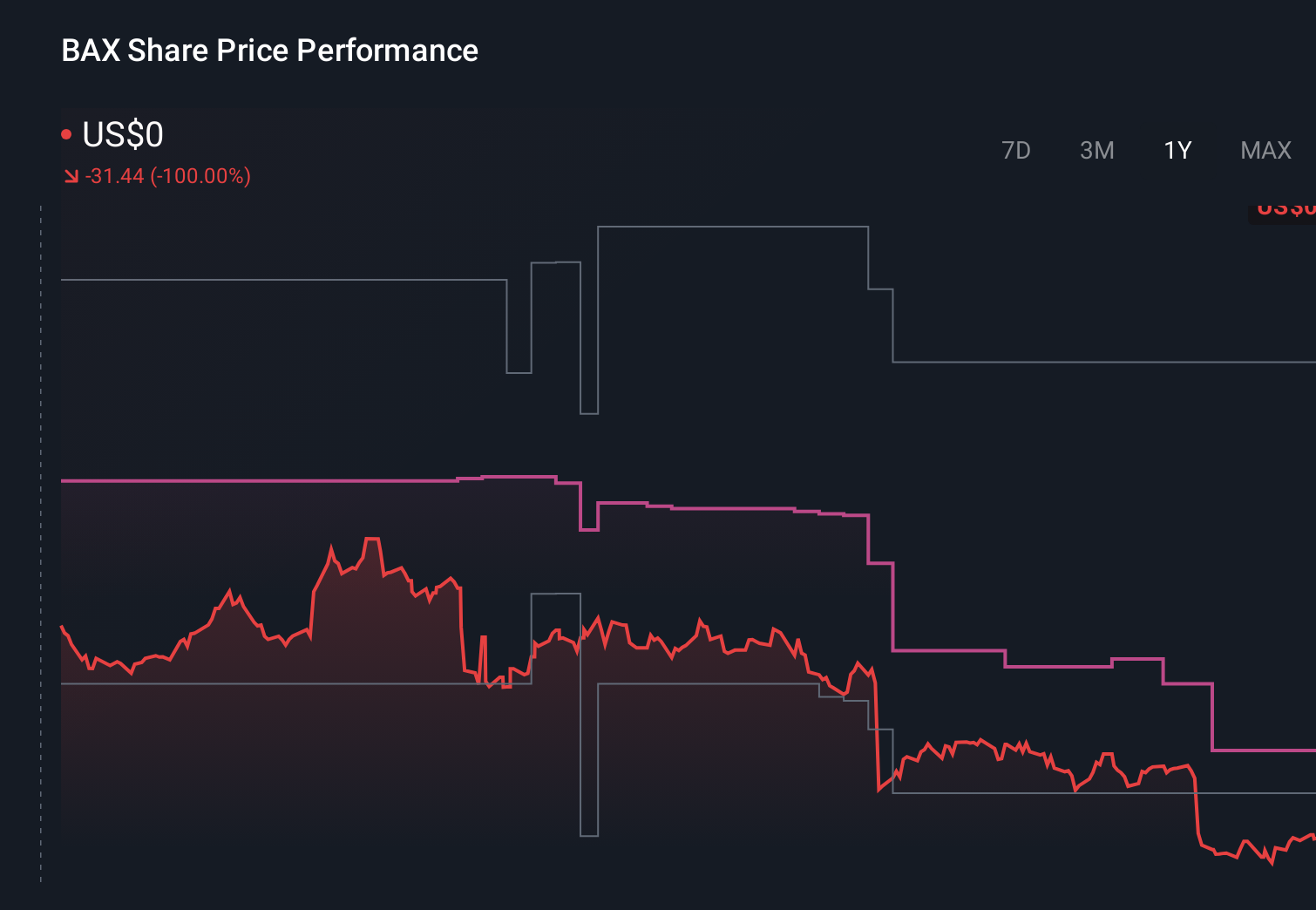

Baxter International Inc. BAX | 0.00 |

- Recently, analysts highlighted that Baxter International is expected to report March-quarter earnings showing a year-over-year decline, with consensus EPS estimates trimmed and indicators such as a negative Earnings ESP and Zacks Rank #4 (Sell) pointing to a challenging setup for an earnings surprise.

- This comes on top of two years of weaker constant-currency revenue trends, declining earnings per share, and low returns on capital, raising fresh questions about how effectively Baxter is investing in and sustaining its core profit engines.

- We’ll now explore how mounting concern over Baxter’s lowered earnings estimates and financial underperformance could influence its existing investment narrative.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Baxter International Investment Narrative Recap

To own Baxter today, you need to believe its broad hospital product portfolio and new devices can eventually translate into better profitability, despite recent earnings pressure and years of weak returns on capital. The latest cut to consensus EPS estimates and indicators pointing to a difficult earnings surprise setup reinforce that the most immediate catalyst is a clearer path back to sustainable earnings, while the key near term risk remains further margin strain if volumes and mix do not improve meaningfully.

Against this backdrop, the upcoming Q1 2026 earnings release on April 30 stands out as the most relevant near term event. It will give investors a fresh read on how far the recent revenue softness, impairments, and low returns are still weighing on the business, and whether newer offerings like the Dynamo stretcher line and advanced surgery products are yet doing enough to offset ongoing pressures in IV solutions, injectables, and Baxter’s integrated supply chain.

Yet beneath the product launches, investors should be aware of how persistent margin compression and post divestiture cost challenges could still...

Baxter International's narrative projects $12.1 billion revenue and $913.6 million earnings by 2028. This requires 3.7% yearly revenue growth and a $1,160.6 million earnings increase from -$247.0 million today.

Uncover how Baxter International's forecasts yield a $21.63 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts see a much tougher road ahead, even before this earnings news, with revenue growth around 1.9 percent a year and earnings only reaching about US$752.8 million by 2029, so it is worth weighing that more pessimistic view against the latest signs of weaker near term profitability.

Explore 6 other fair value estimates on Baxter International - why the stock might be worth 18% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Baxter International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Baxter International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Baxter International's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.