How Investors Are Reacting To Boot Barn (BOOT) Strong Same-Store Gains And Healthier Free Cash Flow Margin

Boot Barn Holdings, Inc. BOOT | 0.00 |

- In recent days, Boot Barn Holdings reported strong organic growth in its western-inspired apparel and footwear business, with same-store sales rising year-on-year and free cash flow margins improving, underscoring healthier operations and cash generation.

- Beneath these operational gains, management’s emphasis on firm consumer demand and confidence in the current business trajectory highlights how the retailer’s brand positioning and merchandising focus are resonating with its expanding customer base.

- Next, we’ll explore how Boot Barn’s improved free cash flow margin may influence its existing investment narrative around expansion and profitability.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn, you need to believe its western and workwear niche can keep drawing customers as the chain adds more stores and deepens its brand mix. The latest update of 6.3% same store sales growth and stronger free cash flow margin supports the near term catalyst of store-led expansion, while not materially changing the biggest risk that aggressive new openings could eventually pressure returns if newer markets underperform.

Among recent announcements, the plan to open 70 new stores sits closest to this story. Strong organic sales and better cash generation give Boot Barn more room to fund this expansion, but they also heighten the importance of avoiding cannibalization and making sure new locations match the current productivity of its existing footprint.

Yet against these positives, investors should be aware that Boot Barn’s growth still leans heavily on physical stores and concentrated western styles...

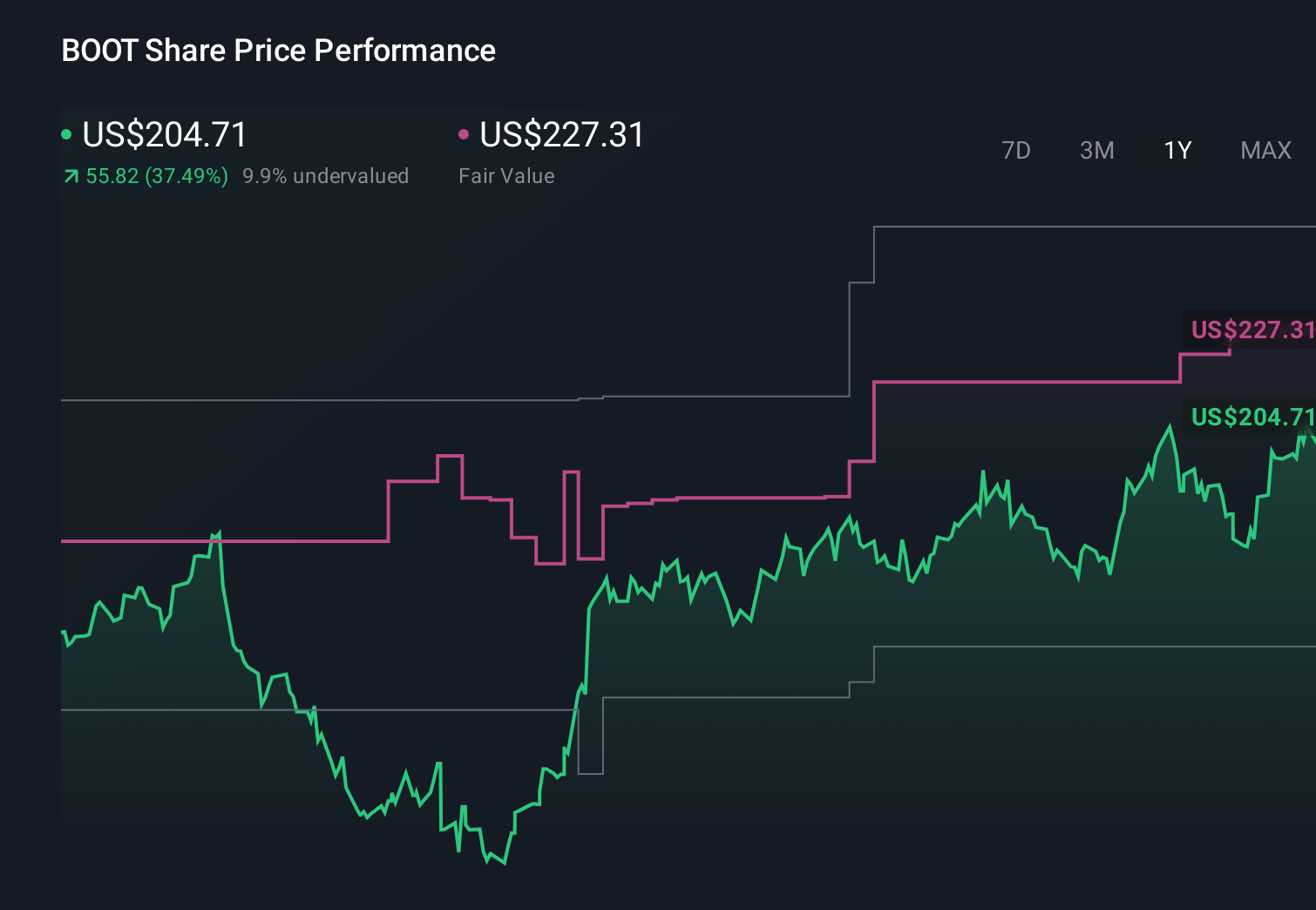

Boot Barn Holdings' narrative projects $3.3 billion revenue and $350.9 million earnings by 2029.

Uncover how Boot Barn Holdings' forecasts yield a $225.14 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Some bullish analysts were assuming revenue could reach about US$3.3 billion and earnings about US$370 million, yet this optimism sits against the risk that e commerce growth outpaces Boot Barn’s store heavy model, reminding you that views on the same sales and cash flow data can diverge sharply and may shift again after this latest update.

Explore 4 other fair value estimates on Boot Barn Holdings - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.