How Investors Are Reacting To Eversource Energy (ES) Regulatory Recovery and Portfolio Shifts

Eversource Energy ES | 69.47 | -0.26% |

- In recent days, Wells Fargo initiated coverage on Eversource Energy with an Overweight rating, citing upcoming regulatory recovery in Connecticut, anticipated project completions, and continued progress on the sale of non-core assets as key positives for the company. Eversource also announced an after-tax charge related to increased liabilities from the sale of two wind projects and narrowed its full-year adjusted earnings guidance, offering greater clarity on its financial outlook.

- This sequence of events underscores how Eversource’s shifting asset portfolio and regulatory developments could meaningfully affect its long-term risk profile and earnings trajectory.

- We'll examine how Wells Fargo's recognition of expected regulatory recovery in Connecticut influences the company’s broader investment outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Eversource Energy Investment Narrative Recap

To be a shareholder in Eversource Energy, you generally need to believe that regulatory recovery in Connecticut and major asset sales, like the Aquarion transaction, will stabilize the company’s balance sheet and support future earnings growth. The recent Wells Fargo coverage and Eversource’s after-tax charge from wind asset sales don’t materially impact the near-term catalyst of regulatory cost recovery approval in Connecticut, but ongoing regulatory risk remains the biggest concern for investors.

Of the recent developments, the narrowing of full-year adjusted earnings guidance stands out, providing investors with greater clarity on expected results as the company manages transitional events such as asset divestitures and project completions. This increased transparency may help support confidence around regulatory and financial catalysts, at least in the immediate term. However, in contrast, investors should be aware that unresolved regulatory uncertainty in Connecticut could...

Eversource Energy's narrative projects $14.8 billion revenue and $2.1 billion earnings by 2028. This requires 4.4% yearly revenue growth and a $1.24 billion earnings increase from the current $858.0 million.

Uncover how Eversource Energy's forecasts yield a $74.60 fair value, in line with its current price.

Exploring Other Perspectives

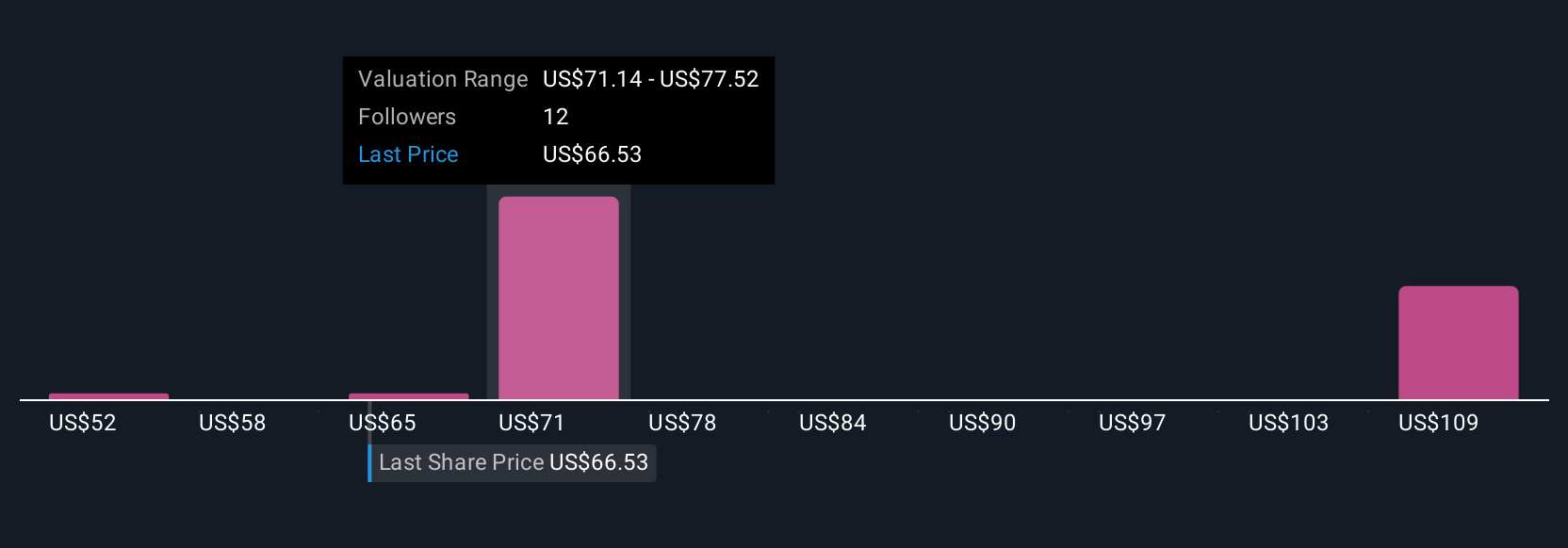

Analysis from four Simply Wall St Community members puts Eversource’s fair value estimate as low as US$52 or as high as US$211.80. Such a wide range highlights how views on regulatory outcomes and earnings clarity can sharply influence expectations for the company’s longer-term performance, so you may want to consider these differing viewpoints carefully.

Explore 4 other fair value estimates on Eversource Energy - why the stock might be worth 30% less than the current price!

Build Your Own Eversource Energy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Eversource Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Eversource Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Eversource Energy's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.