How Investors Are Reacting To Fortinet (FTNT) Margin Concerns After a Strong Earnings Beat

Fortinet, Inc. FTNT | 76.70 | -4.91% |

- Fortinet recently delivered fourth-quarter 2025 results that surpassed its own guidance and market expectations, yet Freedom Capital Markets downgraded the company citing margin risks from rising memory costs, foreign exchange volatility, and heightened competition.

- While Fortinet’s services segment benefited from growth in Unified SASE cloud solutions and recent acquisitions, the downgrade highlights investor concern that customer caution on contract duration and cost pressures could challenge the company’s ability to sustain profitability improvements.

- Next, we’ll examine how concerns over margin pressure, despite strong recent results, may affect Fortinet’s existing investment narrative and risk profile.

Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Fortinet Investment Narrative Recap

To own Fortinet, you need to believe that its integrated cybersecurity platform and pivot toward higher value services can offset hardware cyclicality and rising cost pressures. The latest downgrade underscores that the most important near term catalyst, the ongoing firewall refresh and SASE adoption, now sits beside a sharper focus on margin risk from memory prices and competition. For now, the news challenges confidence in margin resilience more than the core demand story, but the concern is material.

Among recent developments, Fortinet’s strong full year 2025 results, with revenue of US$6,799.6 million and net income of US$1,853.4 million, are most relevant here. They show that, heading into this period of bearish options activity and a more cautious analyst stance, the company was still growing earnings and buying back shares, even as investors questioned how sustainable its profitability would be if memory costs, FX and competitive intensity continue to weigh on margins.

Yet investors should also be aware that margin pressure from rising memory costs and shifting security architectures could...

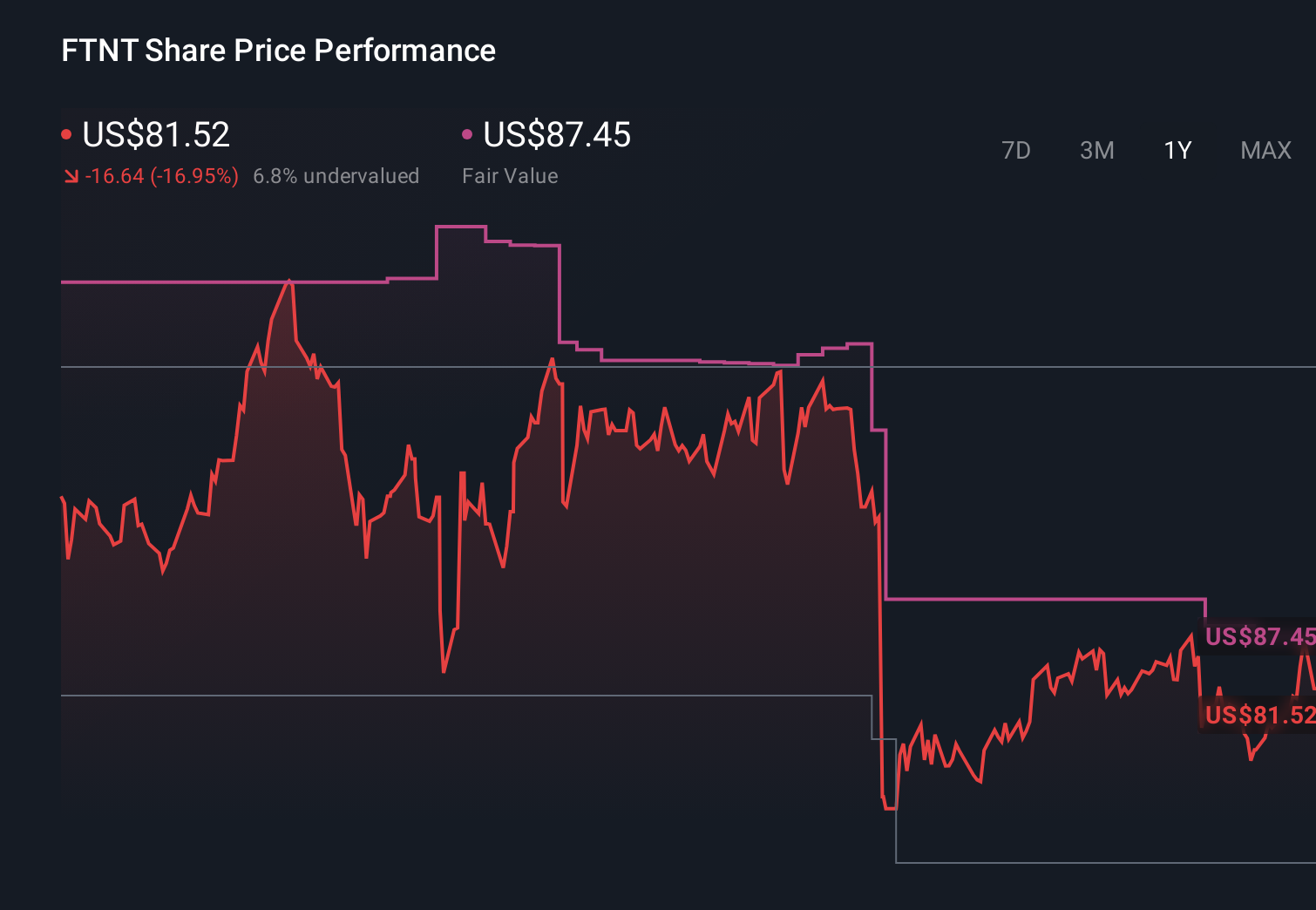

Fortinet's narrative projects $9.2 billion revenue and $2.4 billion earnings by 2028. This requires 13.1% yearly revenue growth and a roughly $0.5 billion earnings increase from $1.9 billion today.

Uncover how Fortinet's forecasts yield a $87.04 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already more cautious, assuming revenue of about US$8.4 billion and earnings of roughly US$2.0 billion by 2028, and their view that platform consolidation could pressure Fortinet’s hardware centric model may feel more relevant after this margin focused downgrade, which shows how sharply opinions can differ and why it is worth comparing several viewpoints before you decide what this news means for you.

Explore 21 other fair value estimates on Fortinet - why the stock might be worth just $85.73!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Fortinet research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Fortinet research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fortinet's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.