How Investors Are Reacting To Life Time (LTH) $500 Million Buyback And Strengthening Member Engagement

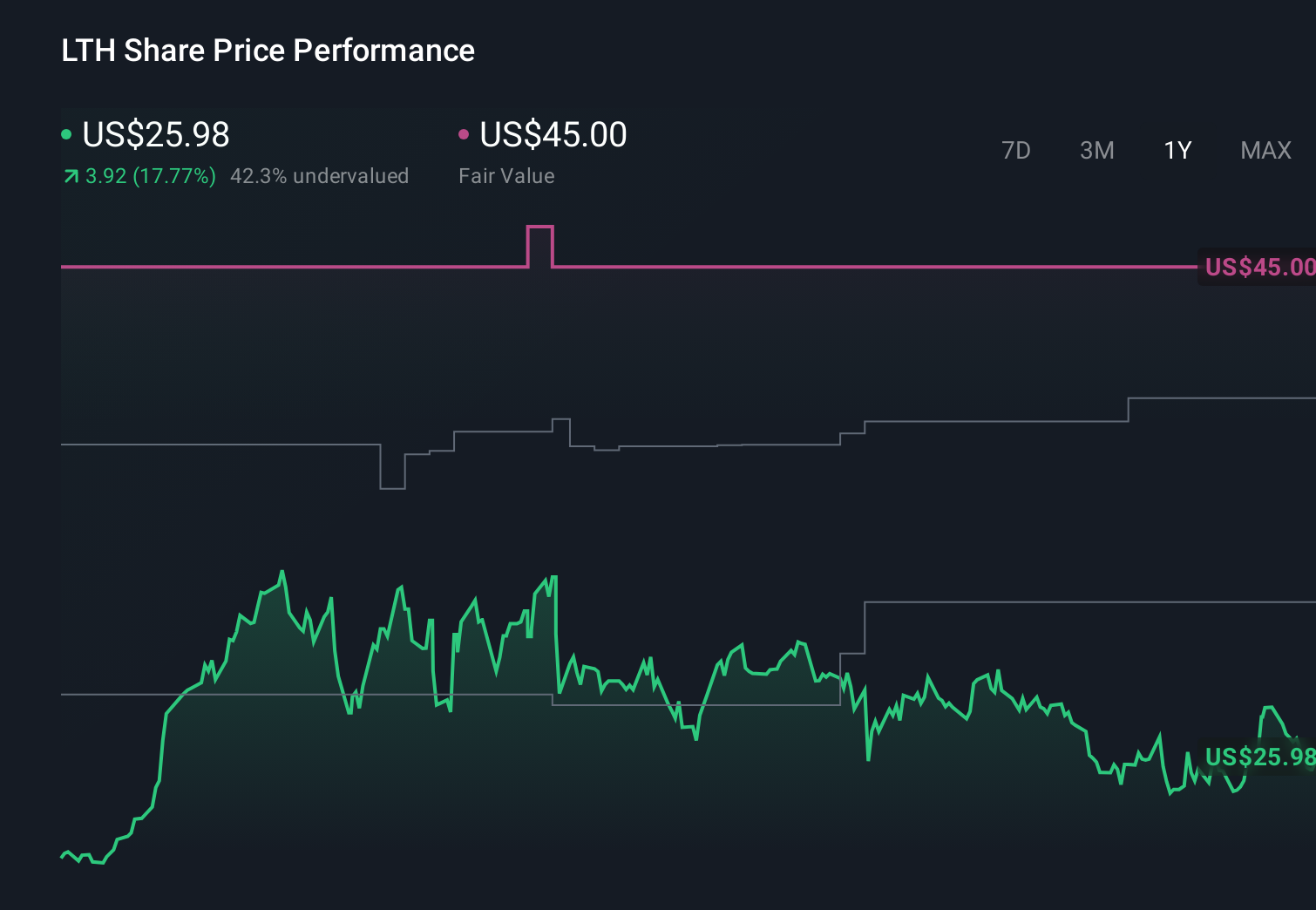

Life Time Group Holdings, Inc. LTH | 27.94 | +0.43% |

- In recent days, Life Time Group Holdings announced a US$500 million share repurchase program, highlighted strong member engagement in its new 60XT fitness challenge, and received supportive analyst coverage, including an Overweight initiation from Wells Fargo.

- This combination of capital return plans, healthier club utilization trends, and growing institutional interest points to improving confidence in the company’s long-term business trajectory.

- We’ll now examine how the US$500 million share repurchase program could influence Life Time’s existing investment narrative and risk-reward profile.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Life Time Group Holdings Investment Narrative Recap

To own Life Time Group Holdings, you have to believe its premium health clubs, expanding ancillary services, and digital tools can support durable membership and revenue growth without overburdening the balance sheet. The US$500 million buyback and healthier member engagement are supportive for the near term, but they do not fully resolve the key risk around heavy capital needs and reliance on real estate and credit markets.

The new buyback authorization is the most relevant development here, because it directly interacts with that capital intensity and debt profile. While analysts previously expected earnings growth to be steady rather than rapid, this capital return plan could reshape how you view the trade off between reinvestment, leverage, and potential per share value creation if operating trends hold.

However, investors should also be aware that if credit markets tighten or sale leaseback financing becomes less attractive, the combination of high debt and a large buyback could...

Life Time Group Holdings’ narrative projects $4.1 billion revenue and $448.6 million earnings by 2029. This requires 10.8% yearly revenue growth and about a $74.9 million earnings increase from $373.7 million.

Uncover how Life Time Group Holdings' forecasts yield a $40.00 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming revenue of about US$3.6 billion and earnings of roughly US$361 million by 2028, yet they still saw risk that high capital spending and digital execution might cap returns, underscoring how differently you can interpret the same growth story and why this new buyback and member engagement update could eventually shift those more pessimistic views.

Explore 3 other fair value estimates on Life Time Group Holdings - why the stock might be worth as much as 67% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.