How Investors Are Reacting To Lumentum (LITE) Expanding U.S. InP Manufacturing For AI Data Centers

Lumentum Holdings, Inc. LITE | 0.00 |

- Lumentum Holdings recently announced plans to establish a new 240,000-square-foot manufacturing facility in Greensboro, North Carolina, acquired from Qorvo, to produce indium phosphide-based optical devices for large AI data centers and to invest hundreds of millions of US dollars while preserving or creating over 400 US manufacturing jobs.

- The facility, which will be retrofitted to make continuous wave and ultra-high-power lasers on 6-inch InP wafers and is expected to ramp production by mid-2028, marks a major step in Lumentum’s onshoring and supply chain resilience efforts for hyperscale AI infrastructure customers such as NVIDIA.

- Next, we’ll examine how this new Greensboro InP manufacturing footprint could reshape Lumentum’s AI-focused investment narrative and risk profile.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Lumentum Holdings Investment Narrative Recap

To own Lumentum today, you need to believe that AI data centers and cloud demand will keep pulling more high end optics, and that the company can turn that demand into profitable growth despite customer concentration and margin pressure in cloud modules. The Greensboro InP facility increases onshoring and long term capacity for hyperscale buyers like NVIDIA, but it also raises near term execution and cost risk around Lumentum’s biggest current catalyst and constraint, which is ramping manufacturing efficiently.

The most relevant recent announcement here is Lumentum’s collaboration with Marvell at OFC 2026 on an optical circuit switching system for large AI fabrics, using Marvell’s 1.6T DSPs with Lumentum’s R300 OCS. It highlights how Lumentum’s AI thesis is not just about more lasers, but about higher value switching and interconnect platforms that could benefit from the Greensboro fab over time if the company executes on yields, costs, and customer qualification.

Yet, investors should also be aware that heavy reliance on a few hyperscale customers could turn sharply against expectations if any one of them decides to shift even part of their orders...

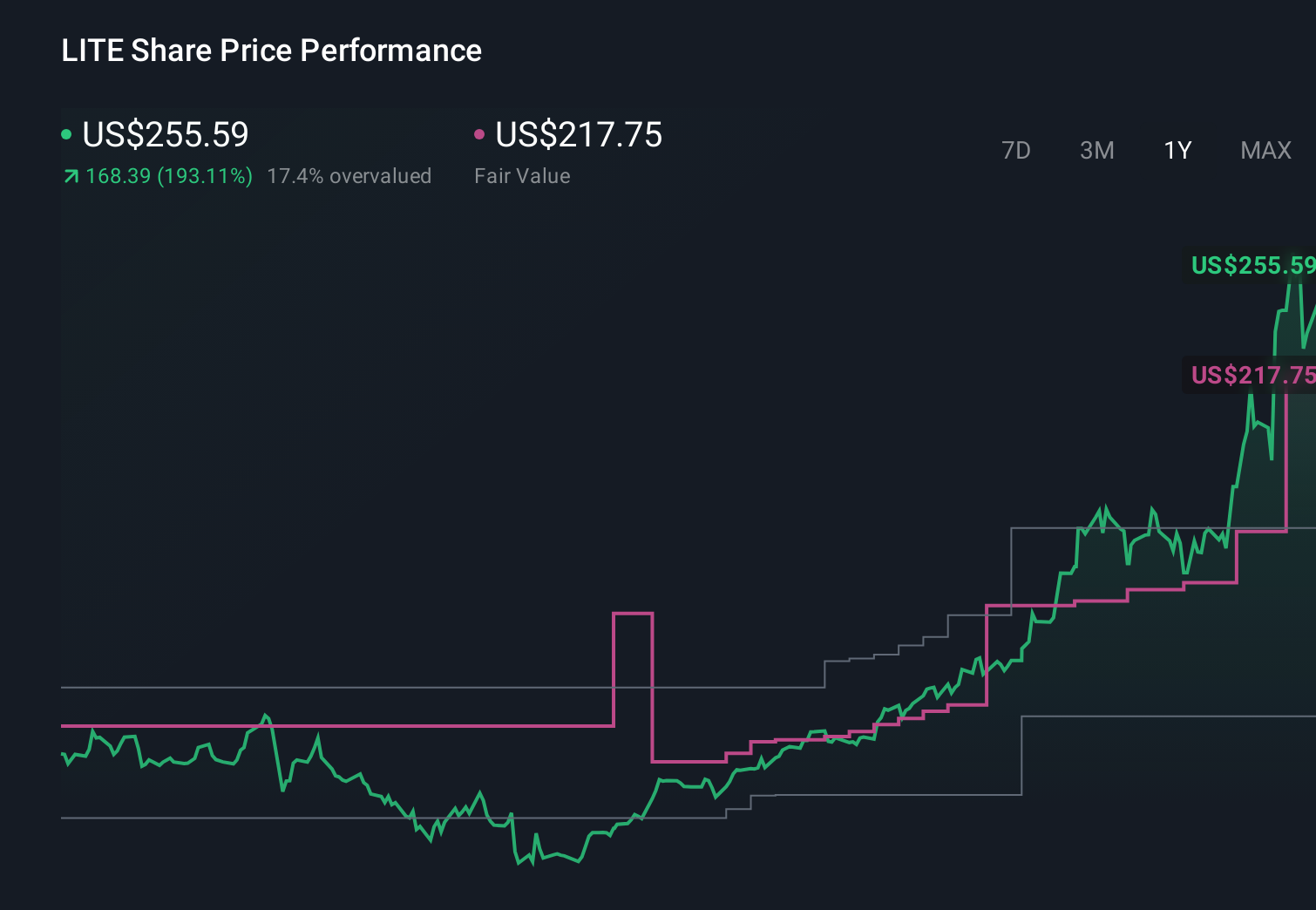

Lumentum Holdings' narrative projects $3.1 billion revenue and $389.1 million earnings by 2028. This requires 23.4% yearly revenue growth and about a $363.2 million earnings increase from $25.9 million today.

Uncover how Lumentum Holdings' forecasts yield a $655.55 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Compared with the consensus view, the most optimistic analysts were already assuming revenue could reach about US$10.7 billion and earnings US$2.7 billion by 2029, so this new Greensboro capacity and the concentration risk around a few hyperscalers may either strengthen that bullish case or force a rethink, depending on how you weigh both upside and execution risk.

Explore 12 other fair value estimates on Lumentum Holdings - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Lumentum Holdings research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Lumentum Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lumentum Holdings' overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.