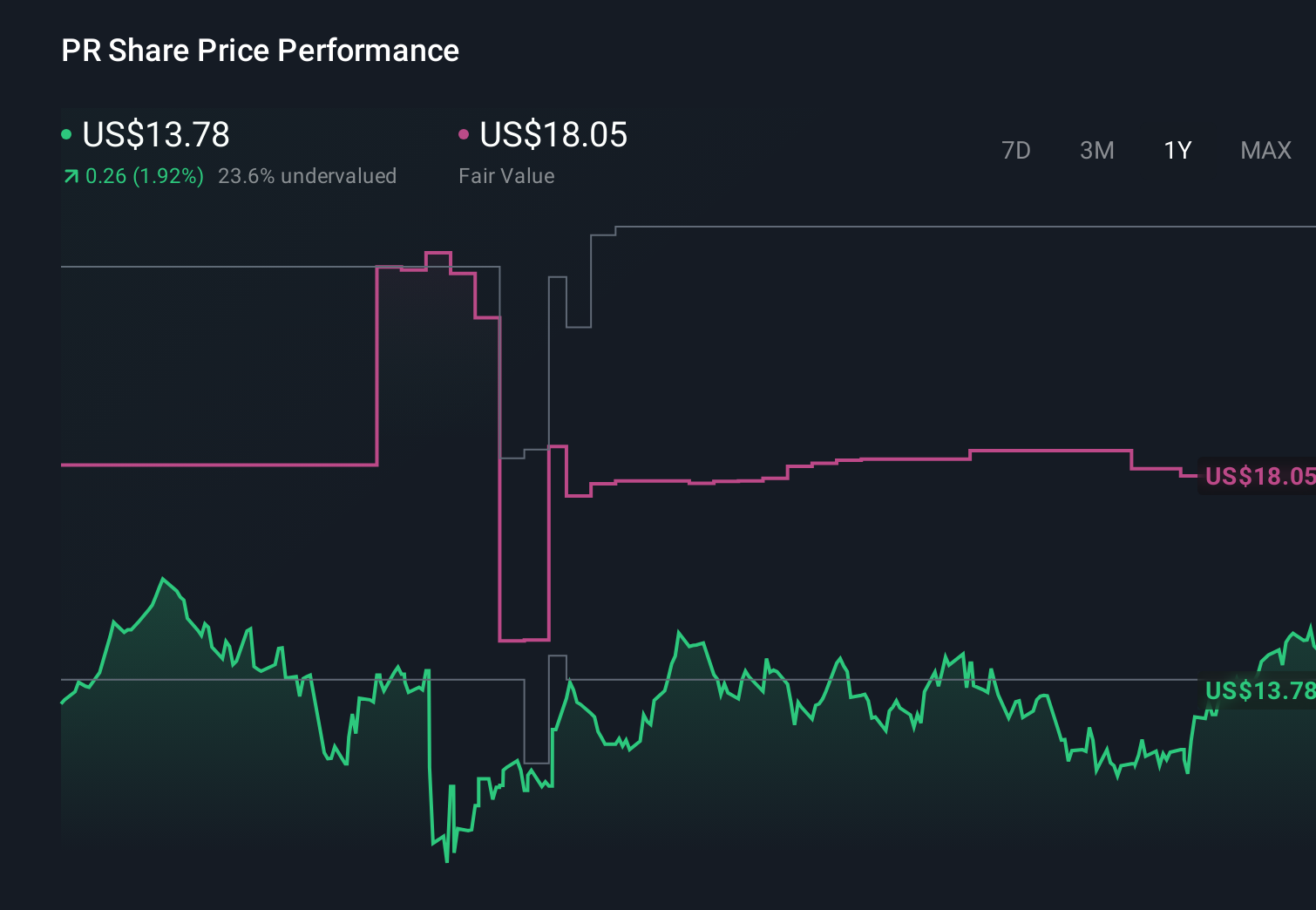

How Investors Are Reacting To Permian Resources (PR) Record Free Cash Flow And Stronger Credit Profile

Permian Resources PR | 0.00 |

- In its latest quarterly update, Permian Resources reported record free cash flow, continued cost discipline, and confirmation of investment-grade credit ratings from all three major agencies, alongside roughly US$1.20 billion of debt reduction since early 2025.

- An interesting angle is how management is using this stronger balance sheet to keep capital allocation flexible across dividends, debt repayment, and potential acquisitions while still prioritizing long-term free cash flow.

- We'll now explore how this record free cash flow and improved credit profile could influence Permian Resources' existing investment narrative and outlook.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Permian Resources Investment Narrative Recap

To own Permian Resources, you need to believe its Permian Basin scale, cost efficiency, and disciplined capital returns can support resilient free cash flow even through commodity swings. The latest record free cash flow and investment grade ratings strengthen that case, but they do not remove the key short term swing factor, which is exposure to oil and gas prices. They also ease, but do not eliminate, balance sheet risk if drilling and acquisition spending stay elevated.

Among recent developments, the May 6 guidance update is most directly connected to this quarter’s strong free cash flow. Management lifted 2026 oil production targets and total volume guidance, which ties back to the operational outperformance that helped generate record cash this quarter. For investors focused on near term catalysts, higher expected volumes, combined with a stronger balance sheet and ongoing dividends, sharpen the focus on how sensitive future results remain to commodity prices.

Yet, against this stronger balance sheet, investors should still pay close attention to how sensitive free cash flow remains to swings in commodity prices and...

Permian Resources' narrative projects $6.4 billion revenue and $1.3 billion earnings by 2029.

Uncover how Permian Resources' forecasts yield a $23.90 fair value, a 18% upside to its current price.

Exploring Other Perspectives

While recent results highlight balance sheet strength and investment grade flexibility, the most bearish analysts were assuming only about US$5.8 billion revenue and roughly US$983 million earnings by 2029, so you should recognize how differently others viewed the same risks and catalysts before this news and consider how those views might now evolve.

Explore 5 other fair value estimates on Permian Resources - why the stock might be worth 6% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Permian Resources research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Permian Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Permian Resources' overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.