How Investors Are Reacting To Philip Morris International (PM) FDA Scrutiny Of ZYN And ZYN Ultra

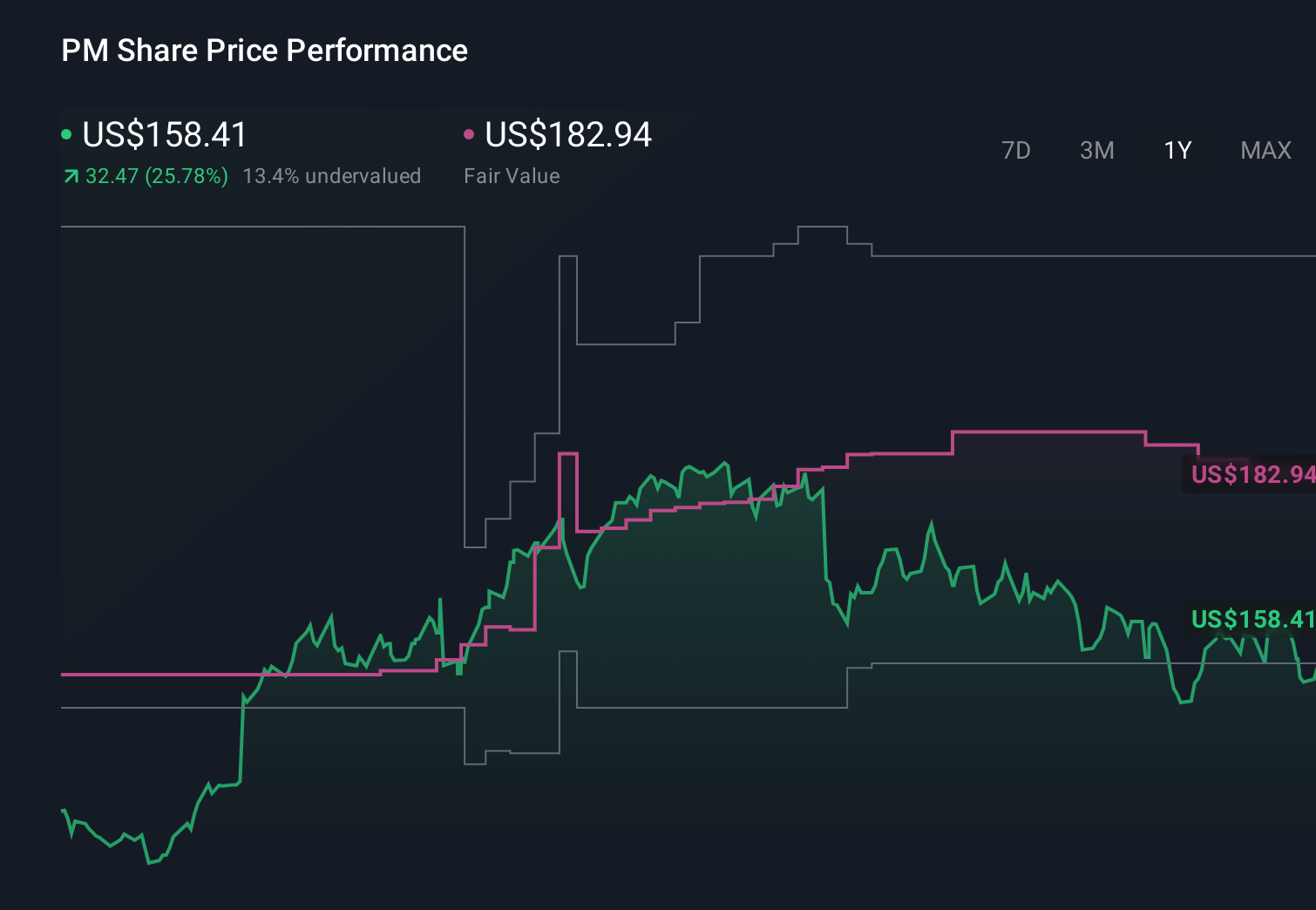

Philip Morris International Inc. PM | 157.79 | +0.99% |

- In the lead-up to its 22 April 2026 Q1 earnings release, Philip Morris International faced heightened FDA scrutiny of its ZYN nicotine pouches, including delays around the ZYN Ultra application amid concerns about youth access and the strength of safety data for adolescents.

- This regulatory uncertainty, combined with Altria’s competing On! PLUS launch in higher-strength pouches, brings PMI’s smoke-free growth ambitions and competitive positioning under closer investor review.

- We’ll now examine how FDA scrutiny of ZYN and the stalled ZYN Ultra application may alter Philip Morris International’s broader investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Philip Morris International Investment Narrative Recap

To own Philip Morris International today, you generally need to believe its shift toward smoke free products like ZYN can offset pressure on traditional cigarettes and support long term earnings. The key near term catalyst is Q1 2026 results on April 22, where any update on ZYN’s US regulatory path will be closely watched. FDA scrutiny of ZYN and the delayed ZYN Ultra decision directly raises the biggest current risk that smoke free growth could slow or become more volatile.

Against this backdrop, PMI’s decision on 18 February 2026 to reaffirm full year 2026 diluted EPS guidance of US$7.87 to US$8.02 stands out. That affirmation came before the latest FDA questions on ZYN and ZYN Ultra and was based on an outlook that assumed continued contribution from smoke free products. How management frames that guidance on the upcoming call, in light of regulatory delays and intensifying competition from Altria’s On! PLUS, will be important for...

Philip Morris International's narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International's forecasts yield a $180.38 fair value, a 12% upside to its current price.

Exploring Other Perspectives

While consensus expects steady progress, the most pessimistic analysts already flagged that tougher nicotine regulation could squeeze margins, even as they projected about US$47.1 billion of revenue and US$14.4 billion of earnings by 2028, so you should weigh how far stricter FDA scrutiny of ZYN might push Philip Morris International closer to that downside path.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth as much as 30% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Philip Morris International research is our analysis highlighting 5 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 62 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.