How Investors Are Reacting To Royal Caribbean Cruises (RCL) Earnings Beat And Fleet Expansion Plan

Royal Caribbean Group RCL | 0.00 |

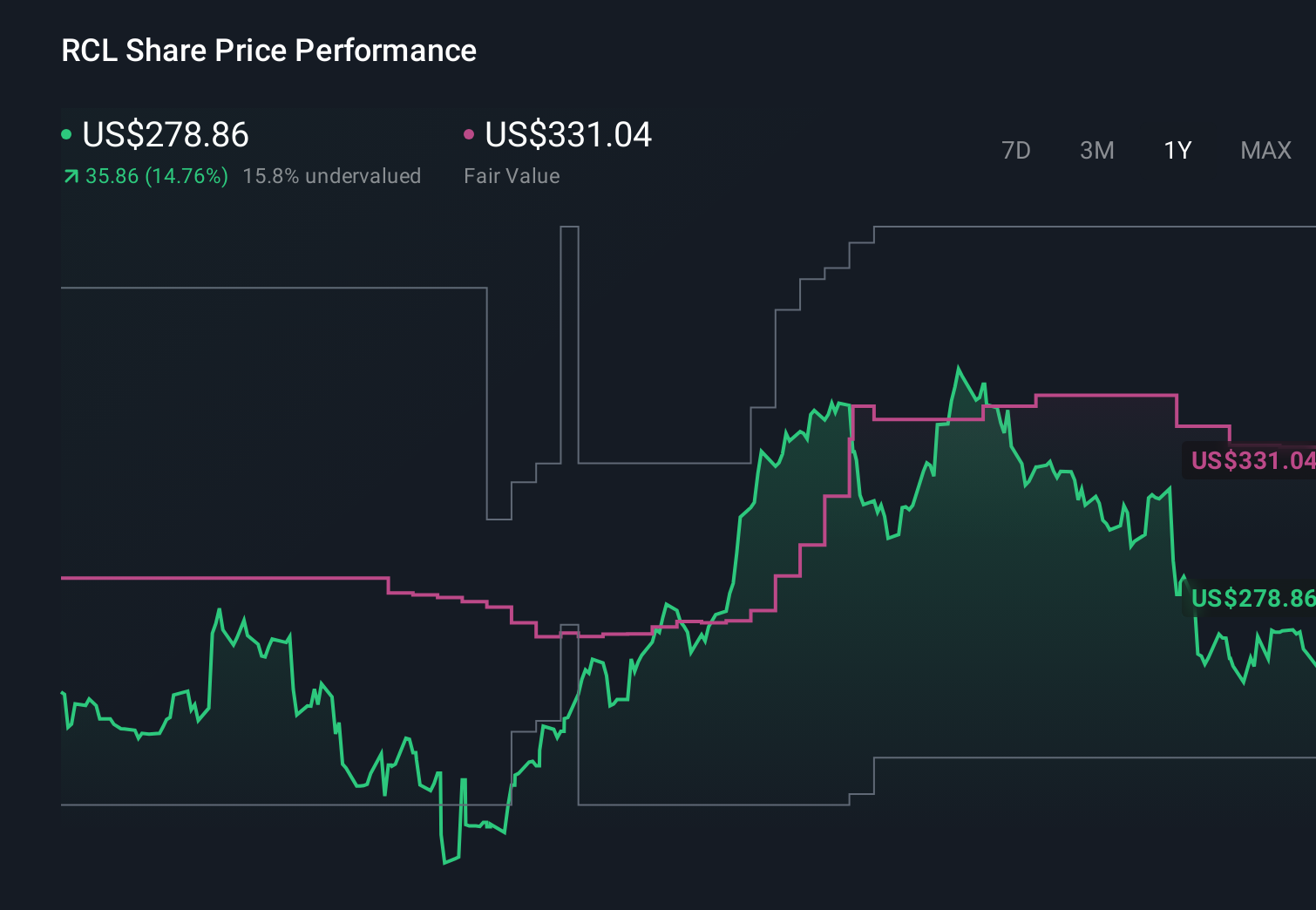

- Royal Caribbean Cruises Ltd. reported past first‑quarter 2026 results with revenue of US$4,452 million and net income of US$941 million, lifting diluted EPS from continuing operations to US$3.48 from US$2.70 a year earlier.

- Alongside the earnings beat, the company confirmed orders for sixth and seventh Icon Class ships and updated full‑year adjusted EPS guidance to US$17.10–US$17.50, tying near‑term performance to a multi‑year fleet expansion and product investment plan.

- With first‑quarter earnings surpassing expectations and full‑year guidance raised, we’ll examine how this stronger outlook reshapes Royal Caribbean’s investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Royal Caribbean Cruises Investment Narrative Recap

To own Royal Caribbean today, you need to believe cruise demand can stay resilient enough to support heavy investment in new ships while offsetting macro and fuel headwinds. The latest earnings beat and updated full year EPS guidance of US$17.10–US$17.50 sharpen the near term focus on execution and pricing, while higher fuel costs and geopolitical disruptions remain the most immediate risks to margins and close in bookings. Overall, this news reinforces rather than changes the core thesis.

The confirmation of sixth and seventh Icon Class ships, on top of strong first quarter results, ties Royal Caribbean’s story even more tightly to its multi year fleet and destination build out. For investors watching catalysts, this order underlines how future earnings will lean on filling and profitably pricing these larger ships, even as the company balances elevated capital spending with shareholder returns such as dividends and buybacks.

Yet while the recent quarter looked strong, investors should still pay close attention to how higher fuel costs and geopolitical disruptions could...

Royal Caribbean Cruises' narrative projects $23.0 billion revenue and $6.1 billion earnings by 2029. This requires 8.6% yearly revenue growth and a $1.8 billion earnings increase from $4.3 billion today.

Uncover how Royal Caribbean Cruises' forecasts yield a $348.46 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue near US$24 billion and earnings around US$6.9 billion by 2029, so this earnings beat and fuel related guidance tweak may either support that upside view or force a rethink of how rising costs, including the risk of higher interest and regulatory pressures, could shape Royal Caribbean’s longer term profit path.

Explore 6 other fair value estimates on Royal Caribbean Cruises - why the stock might be worth as much as 60% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Royal Caribbean Cruises research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Royal Caribbean Cruises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Royal Caribbean Cruises' overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 37 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.