How Investors Are Reacting To Sempra (SRE) Pairing New Debt With Major Texas Grid Expansion

Sempra SRE | 0.00 |

- Sempra recently completed a US$1.00 billion floating-rate note offering due January 2028 and brought its Port Arthur Pipeline Louisiana Connector into service, while ERCOT endorsed over US$7.00 billion of future high-voltage transmission projects in Texas largely expected to be built by Sempra-controlled Oncor.

- Together, these developments highlight how Sempra is pairing fresh financing with large-scale electric and gas infrastructure build-outs that could reshape its long-term regulated and export-focused asset base.

- Next, we will examine how ERCOT’s backing of major Texas transmission upgrades may influence Sempra’s investment narrative and future capital deployment.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Sempra Investment Narrative Recap

To own Sempra, you need to be comfortable with a capital‑intensive, regulated utility that is steadily reshaping its grid and LNG footprint while managing political, regulatory, and project‑execution risk. The latest US$1.0 billion note issuance and ERCOT‑backed Texas projects reinforce the near term catalyst around deploying large amounts of capital into regulated assets, while also underscoring the key risk that future regulatory decisions or cost‑of‑capital changes could materially affect returns on that spending.

Among the recent updates, ERCOT’s endorsement of more than US$7.0 billion in high voltage transmission projects that Oncor expects to build stands out as most relevant. It ties directly into Sempra’s current catalyst of expanding its regulated rate base in Texas, but it also amplifies exposure to long duration regulatory and permitting processes, where any shift in approval timelines or allowed returns could influence how attractive this investment cycle ultimately proves to be.

Yet investors should also weigh how much long term Texas regulatory risk they are really taking on, because...

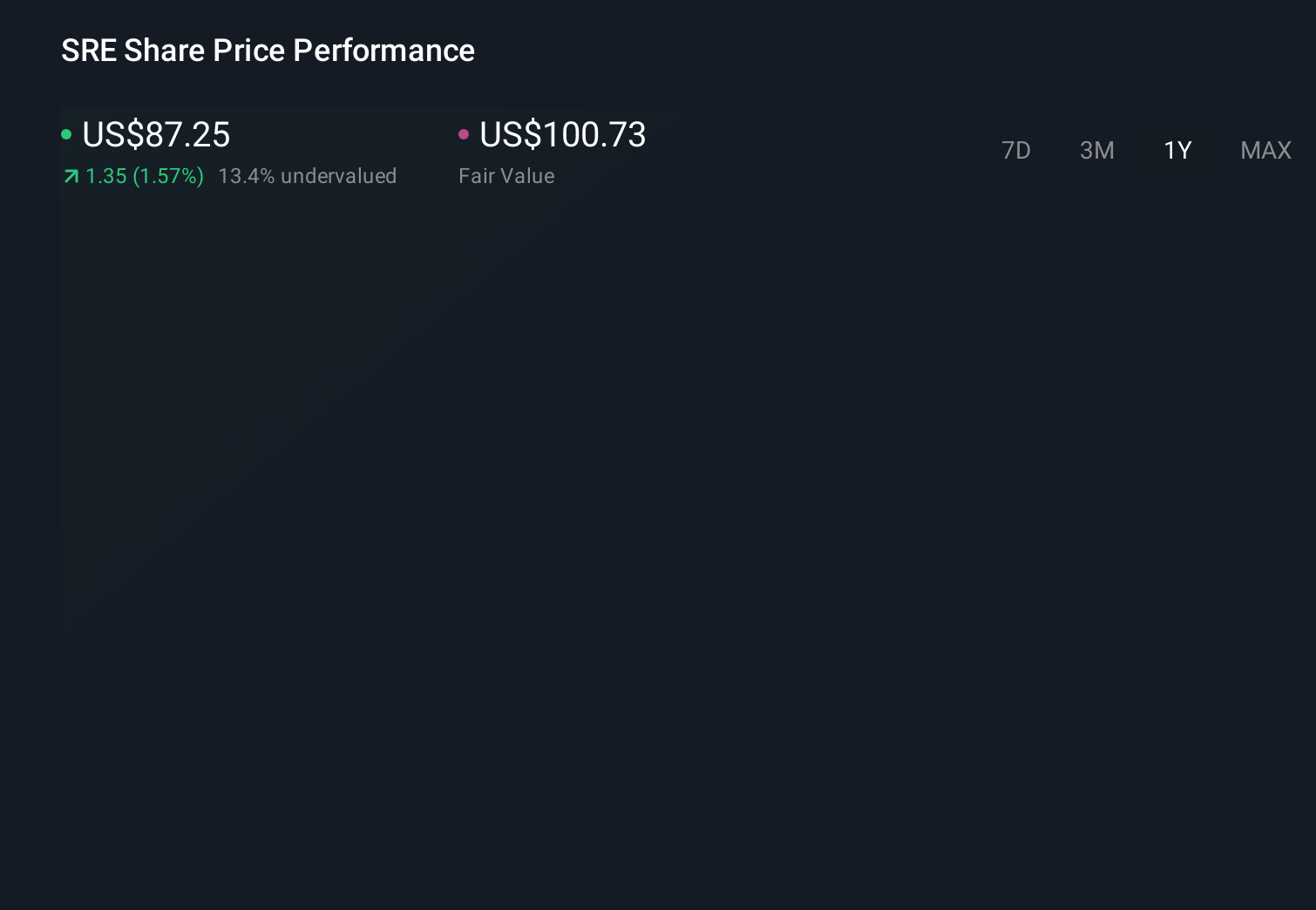

Sempra's narrative projects $14.3 billion revenue and $4.1 billion earnings by 2029. This requires 1.8% yearly revenue growth and a $2.2 billion earnings increase from $1.9 billion today.

Uncover how Sempra's forecasts yield a $103.62 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$51 to US$104 per share, showing how widely individual views on Sempra can differ. You are weighing those opinions against a company that is committing to very large, long lived Texas transmission and LNG related investments, where future regulatory shifts or capital cost pressures could meaningfully affect how those projects perform over time.

Explore 2 other fair value estimates on Sempra - why the stock might be worth as much as 13% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Sempra research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Sempra research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sempra's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.