How Investors Are Reacting To SoFi Technologies (SOFI) Fee-Driven Pivot After Strong Q1 And PrimaryBid Deal

SoFi SOFI | 0.00 |

- In the past week, SoFi Technologies reported Q1 2026 revenue of US$1.10 billion, GAAP net income growth of 135%, record US$12.18 billion in loan originations, and announced the acquisition of UK fintech PrimaryBid’s assets to bolster retail access to capital markets.

- Beneath the headlines, SoFi is pushing a capital-light shift toward fee-based growth, deposits, and third-party partnerships, aiming to build a more resilient, diversified financial services ecosystem less tied to traditional lending cycles.

- Now we’ll examine how this emphasis on capital-light, fee-based growth may reshape SoFi Technologies’ investment narrative for long-term investors.

Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

SoFi Technologies Investment Narrative Recap

To own SoFi Technologies, you need to believe it can evolve from a lending-centric fintech into a broad, capital-light financial platform that leans on fee income, deposits, and partnerships. The latest results, with US$1.10 billion in Q1 2026 revenue and strong loan originations, support that shift, but the key near term catalyst remains execution in fee-based businesses while the biggest risk is pressure on its Technology Platform and loan quality in a higher rate backdrop.

The PrimaryBid asset acquisition feels most relevant here, because it sits at the intersection of SoFi’s push into fee-based services and its ambition to deepen retail access to capital markets. If SoFi can integrate IPO allocation technology into its existing member base, it could reinforce the move away from balance sheet heavy growth and support its capital-light narrative, even as investors watch closely how Technology Platform revenue and credit performance evolve.

Yet beneath the headline growth and new products, investors should be aware that rising credit losses or partnership disruptions could still...

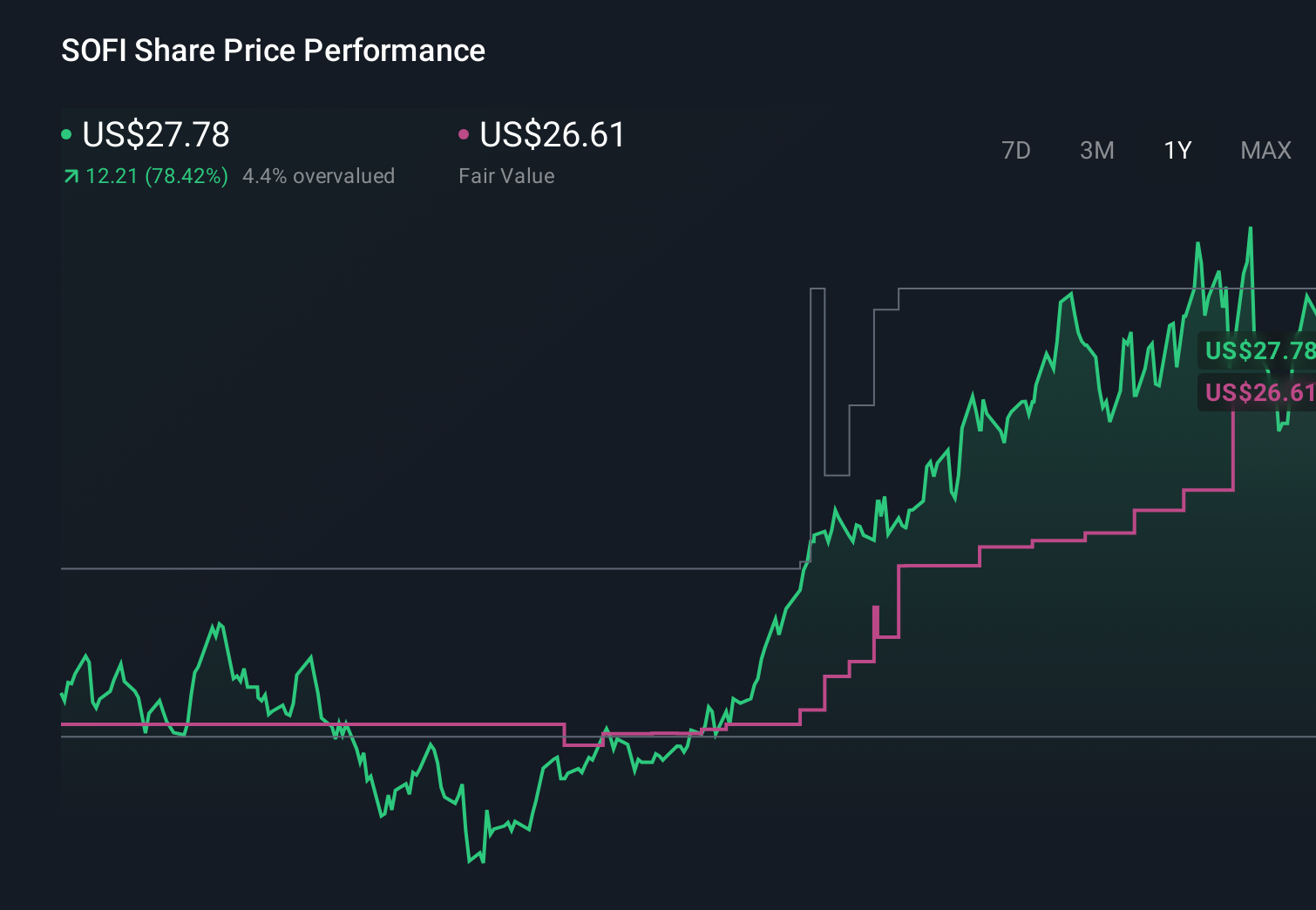

SoFi Technologies' narrative projects $5.1 billion revenue and $954.1 million earnings by 2028.

Uncover how SoFi Technologies' forecasts yield a $26.75 fair value, a 71% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming SoFi could reach about US$8.3 billion in revenue and US$1.8 billion in earnings by 2029, which is far more upbeat than consensus and could either look realistic or stretched once the impact of SoFi’s Q1 results and PrimaryBid deal on loan platform scaling and earnings quality becomes clearer.

Explore 50 other fair value estimates on SoFi Technologies - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your SoFi Technologies research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free SoFi Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate SoFi Technologies' overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.