How Investors Are Reacting To Tyson Foods (TSN) Expanding Buybacks and Adding a Technology Leader

Tyson Foods, Inc. Class A TSN | 0.00 |

- Earlier this month, Tyson Foods expanded its share buyback program by an additional 43 million shares, declared quarterly dividends for both Class A and B shares, and appointed Xbox President Sarah Bond as a new independent director following its third-quarter financial results and a reported $343 million goodwill impairment.

- The addition of a technology executive to Tyson’s board and continuation of shareholder returns underscore the company’s focus on board diversification and capital allocation just after mixed earnings and a significant write-down.

- We’ll examine how Tyson’s expanded share repurchase program and recent board appointment could influence the company’s investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Tyson Foods Investment Narrative Recap

To be a Tyson Foods shareholder in the current environment, you have to believe that consistent consumer demand for branded proteins and multiyear efforts in product innovation, operational efficiency, and international markets will eventually outweigh persistent margin pressures and cyclical swings in the Beef segment. The recent board appointment and buyback expansion are positive for governance and capital allocation, but these developments do not fundamentally alter the near-term focus on beef supply constraints and margin recovery, which remain the main catalyst and risk for the business.

Among recent announcements, Tyson’s $343 million goodwill impairment reported in the third quarter is especially relevant, as it highlights the risk of further asset write-downs tied to ongoing weakness in its Beef segment. This write-down underscores the significant headwinds faced by Tyson’s most challenged business unit and reinforces the importance of sustainable margin improvement as a short- to medium-term driver for the stock.

By contrast, investors should be mindful of the risk that persistent beef supply constraints may...

Tyson Foods is projected to reach $57.7 billion in revenue and $2.3 billion in earnings by 2028. This forecast relies on a 2.1% annual revenue growth rate and reflects a $1.5 billion increase in earnings from the current level of $784 million.

Uncover how Tyson Foods' forecasts yield a $63.25 fair value, a 11% upside to its current price.

Exploring Other Perspectives

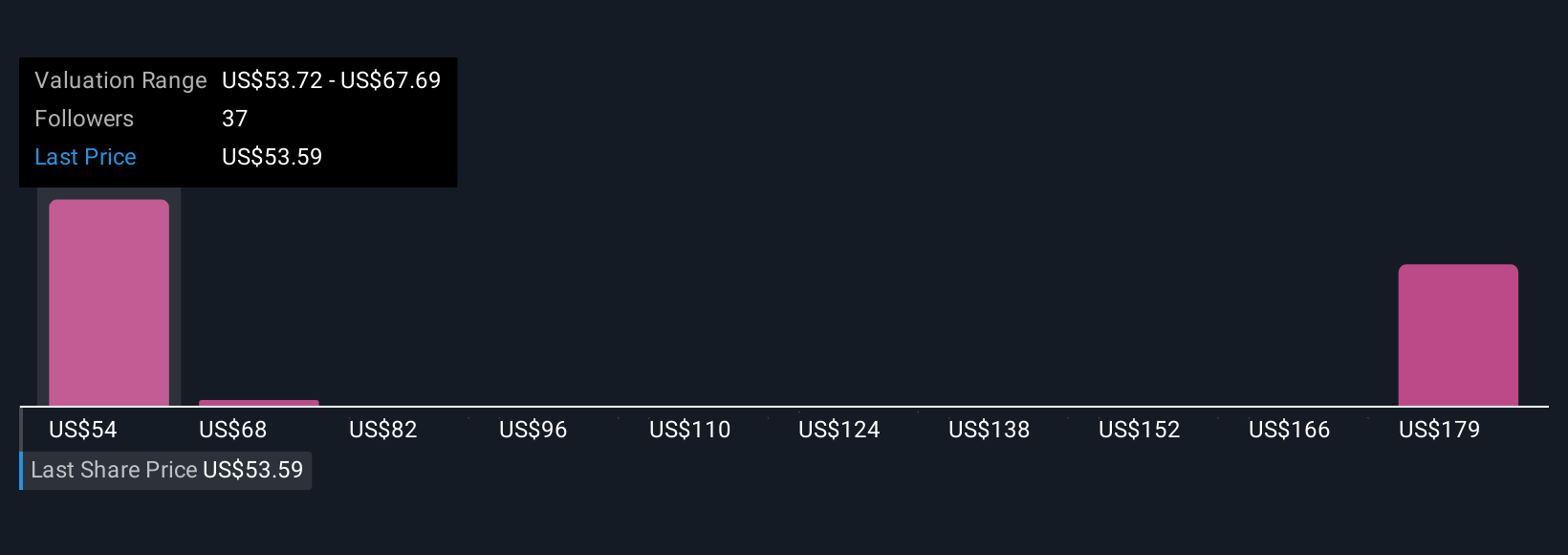

Ten Simply Wall St Community valuations for Tyson Foods span a wide US$53.72 to US$165.69, showing broad disagreement on fair value. While many believe in margin and earnings recovery, ongoing beef supply issues could weigh on future performance and are important context when comparing viewpoints.

Explore 10 other fair value estimates on Tyson Foods - why the stock might be worth 5% less than the current price!

Build Your Own Tyson Foods Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tyson Foods research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Tyson Foods research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tyson Foods' overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find companies with promising cash flow potential yet trading below their fair value.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 28 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.