How Investors Are Reacting To Vulcan Materials (VMC) Reaffirmed EBITDA Guidance And Expanding Infrastructure Backlog

Vulcan Materials Company VMC | 0.00 |

- Earlier in 2025, Vulcan Materials reported solid safety and financial results for the first half of the year, with expanding margins and higher adjusted EBITDA despite challenging weather, and reaffirmed its full-year adjusted EBITDA guidance supported by improving public and private demand.

- The company highlighted accelerating bookings and growing backlogs tied to infrastructure spending, data center work, and a recovering private nonresidential sector, underlining the breadth of demand supporting its aggregates business.

- We’ll now examine how reaffirmed full-year EBITDA guidance, underpinned by accelerating bookings and backlogs, may influence Vulcan Materials’ investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you need to believe that steady demand for aggregates from public infrastructure, data centers, and recovering private construction can support margins through cycles. The reaffirmed full year EBITDA guidance suggests the recent update modestly reinforces the near term catalyst of growing infrastructure driven backlogs, while the biggest current risk remains weather and regional concentration, which can still disrupt volumes even when demand fundamentals look solid.

Among recent announcements, the planned CEO transition to Ronnie Pruitt on 1 January 2026 stands out in this context. With Vulcan leaning on infrastructure and data center demand to support its guidance, investors will be watching how the new leadership team executes on pricing, cost discipline, and any future acquisitions against a backdrop of accelerating bookings but still meaningful weather and permitting risks.

Yet, beneath the reaffirmed guidance and robust backlogs, there is a less visible risk investors should be aware of around...

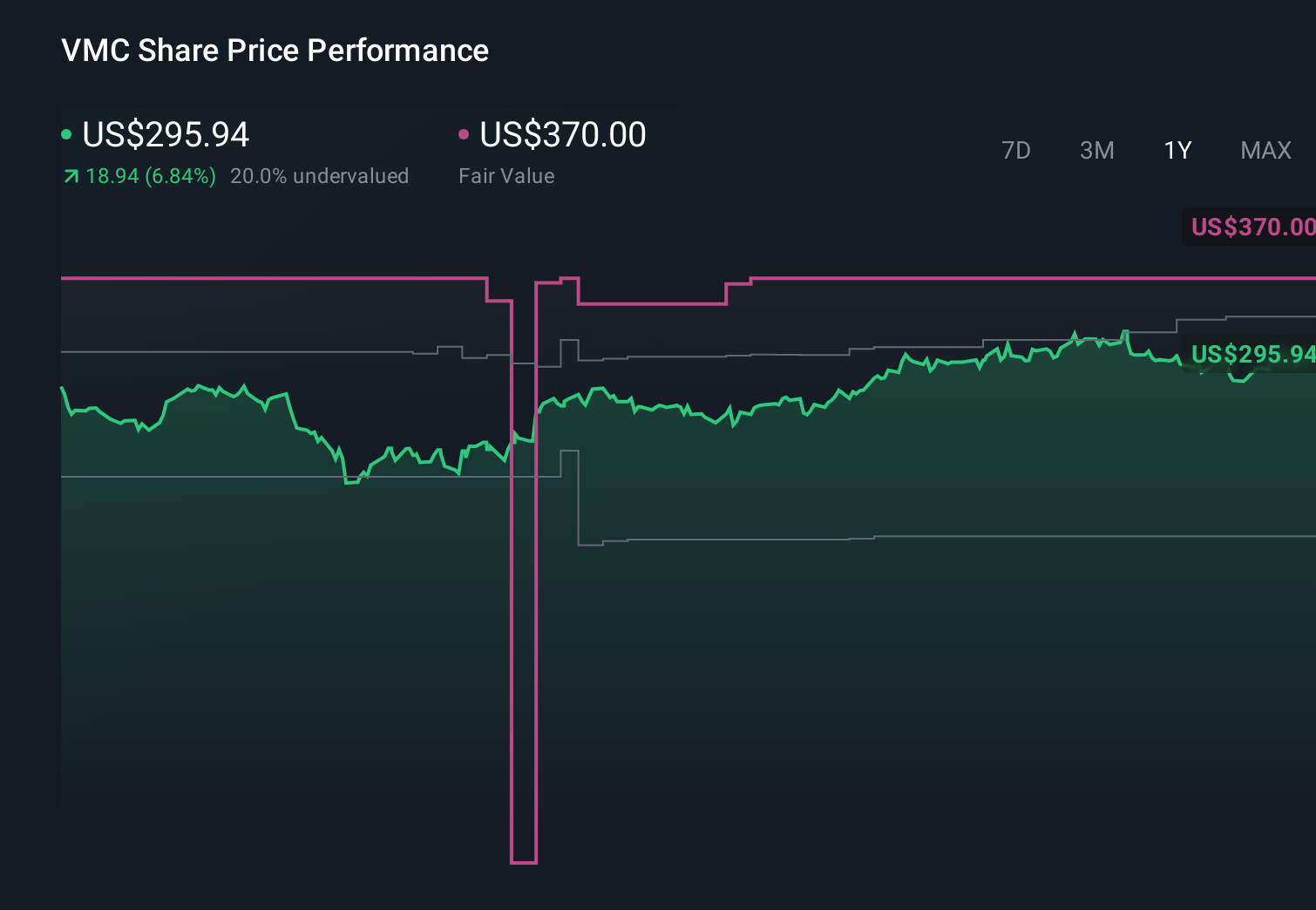

Vulcan Materials' narrative projects $9.6 billion revenue and $1.5 billion earnings by 2028.

Uncover how Vulcan Materials' forecasts yield a $327.57 fair value, a 12% upside to its current price.

Exploring Other Perspectives

While consensus focuses on solid demand and reaffirmed guidance, the most optimistic analysts once projected Vulcan reaching about US$10.0 billion in revenue and US$1.9 billion in earnings, which contrasts sharply with concerns about stricter environmental regulation and geographic concentration, and this new update could shift how you weigh those very different futures.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth as much as 25% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.