How Investors Are Reacting To Zscaler (ZS) Raising 2026 Guidance Despite a Wider Quarterly Loss

Zscaler, Inc. ZS | 134.33 | +2.53% |

- In late February 2026, Zscaler reported second-quarter results showing revenue rising to US$815.75 million while its net loss widened to US$34.31 million, and the company raised both third-quarter and full-year fiscal 2026 revenue and annual recurring revenue guidance.

- At the same time, Zscaler’s higher spending in a competitive market and concerns around billings, new customer growth, and integration of acquired businesses have led investors to question how durable its growth and path toward profitability may be.

- Given Zscaler’s updated guidance and wider quarterly loss, we’ll now examine how these results reshape its Zero Trust and AI security-led investment narrative.

Uncover the next big thing with 30 elite penny stocks that balance risk and reward.

Zscaler Investment Narrative Recap

To own Zscaler, you need to believe its Zero Trust and AI security platform can turn strong revenue growth into a clear path to sustainable profitability. Right now, the key near term catalyst is whether raised fiscal 2026 revenue and ARR guidance translate into healthier billings and net new ARR, while the biggest risk is that higher spending and integration challenges around acquisitions keep losses elevated. The latest quarter reinforces both the opportunity and these execution questions.

Among the recent announcements, the AI & Cyber Threat Research Center in India stands out as closely linked to Zscaler’s AI security and Zero Trust thesis. By expanding research and threat intelligence capabilities with Bharti Airtel, Zscaler is deepening its presence in a large, rapidly digitizing market, which could support its AI security offerings and Zero Trust Everywhere adoption over time, even as investors focus on billings trends, customer growth, and integration of acquired assets.

Yet against this stronger AI story, concerns around higher losses, billings and Red Canary integration are information investors should be aware of before...

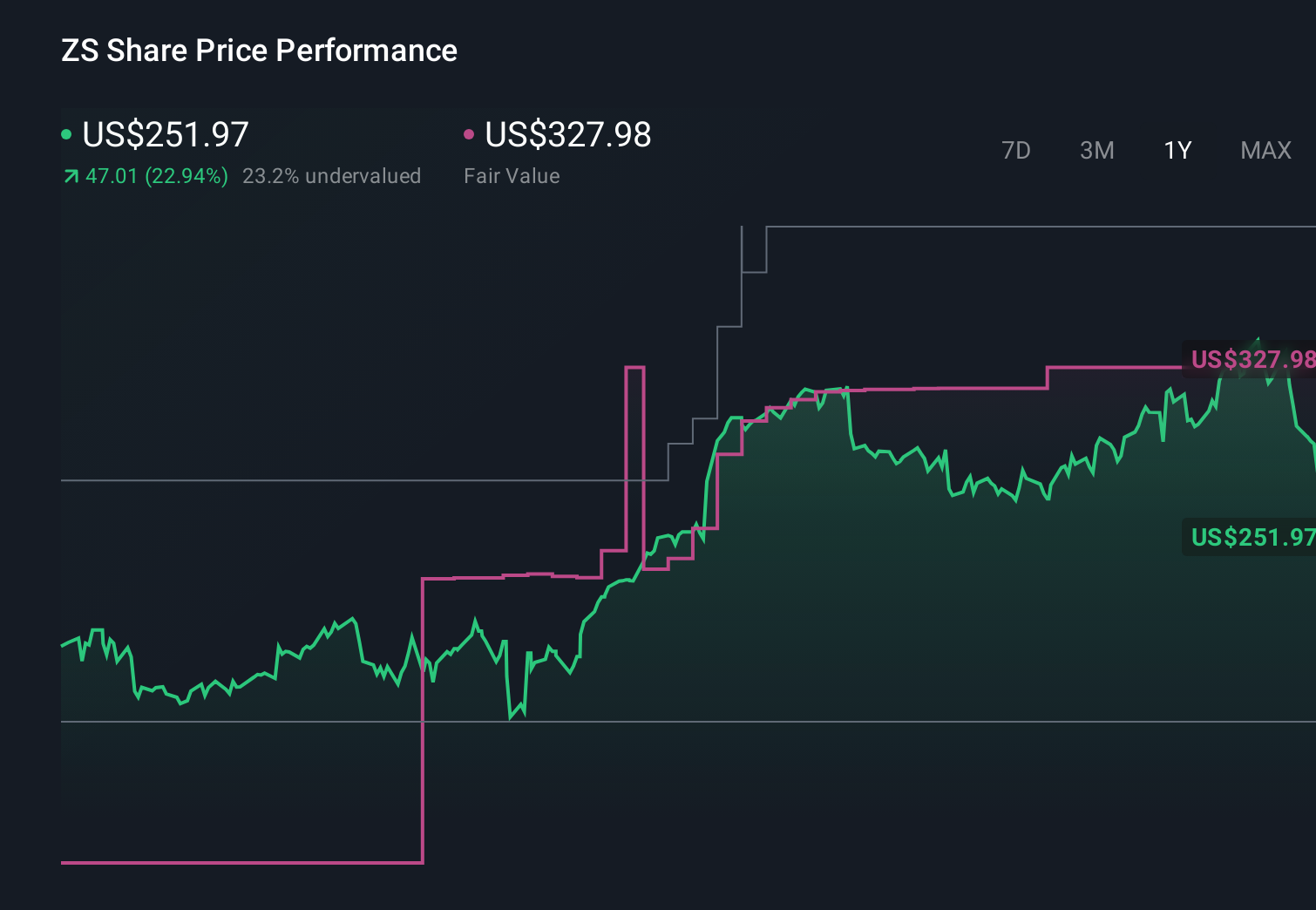

Zscaler's narrative projects $4.7 billion revenue and $139.8 million earnings by 2028. This requires 20.5% yearly revenue growth and a $181.3 million earnings increase from -$41.5 million today.

Uncover how Zscaler's forecasts yield a $304.23 fair value, a 105% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much tougher picture, assuming about 19.7% annual revenue growth and no profits within three years, so if you are weighing this quarter’s higher spending and integration risks, it is worth comparing their more cautious expectations around AI rich products and margins with more optimistic views to see how the story might shift after these results.

Explore 9 other fair value estimates on Zscaler - why the stock might be worth 38% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Zscaler research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.