How Investors May Respond To Ameris Bancorp (ABCB) A+ EPS Upgrade And Steady Insider Activity

Ameris Bancorp ABCB | 0.00 |

- Earlier this week, analysts upgraded Ameris Bancorp to an A+ EPS Revision Grade, citing stronger earnings momentum and a more favorable earnings outlook for the bank.

- An interesting angle is that this upgrade comes alongside steady insider activity, with no recent buying or selling, pointing to management’s apparent comfort with current performance trends.

- Next, we’ll consider how this stronger earnings momentum, reflected in the A+ EPS Revision Grade, may influence Ameris Bancorp’s existing investment narrative.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Ameris Bancorp Investment Narrative Recap

To own Ameris Bancorp, you need to be comfortable with a regional bank story built on net interest income, credit quality and disciplined growth in its core Southeastern footprint. The A+ EPS Revision Grade reinforces the near term earnings momentum that many shareholders are already focused on, but it does not remove the key risk that rising competition for deposits and loans could pressure net interest margins if pricing becomes more aggressive.

The recent Q1 2026 results are particularly relevant here, with higher net interest income of US$244.44 million and net income of US$110.49 million supporting the stronger earnings outlook reflected in the EPS upgrade. At the same time, net charge offs of US$11.354 million remind you that credit costs remain an important swing factor for how much of that earnings momentum ultimately reaches the bottom line and shapes the Ameris investment case.

But while the earnings revisions look encouraging, investors should be aware of rising competitive pressure on Ameris Bancorp’s deposit and loan pricing, which...

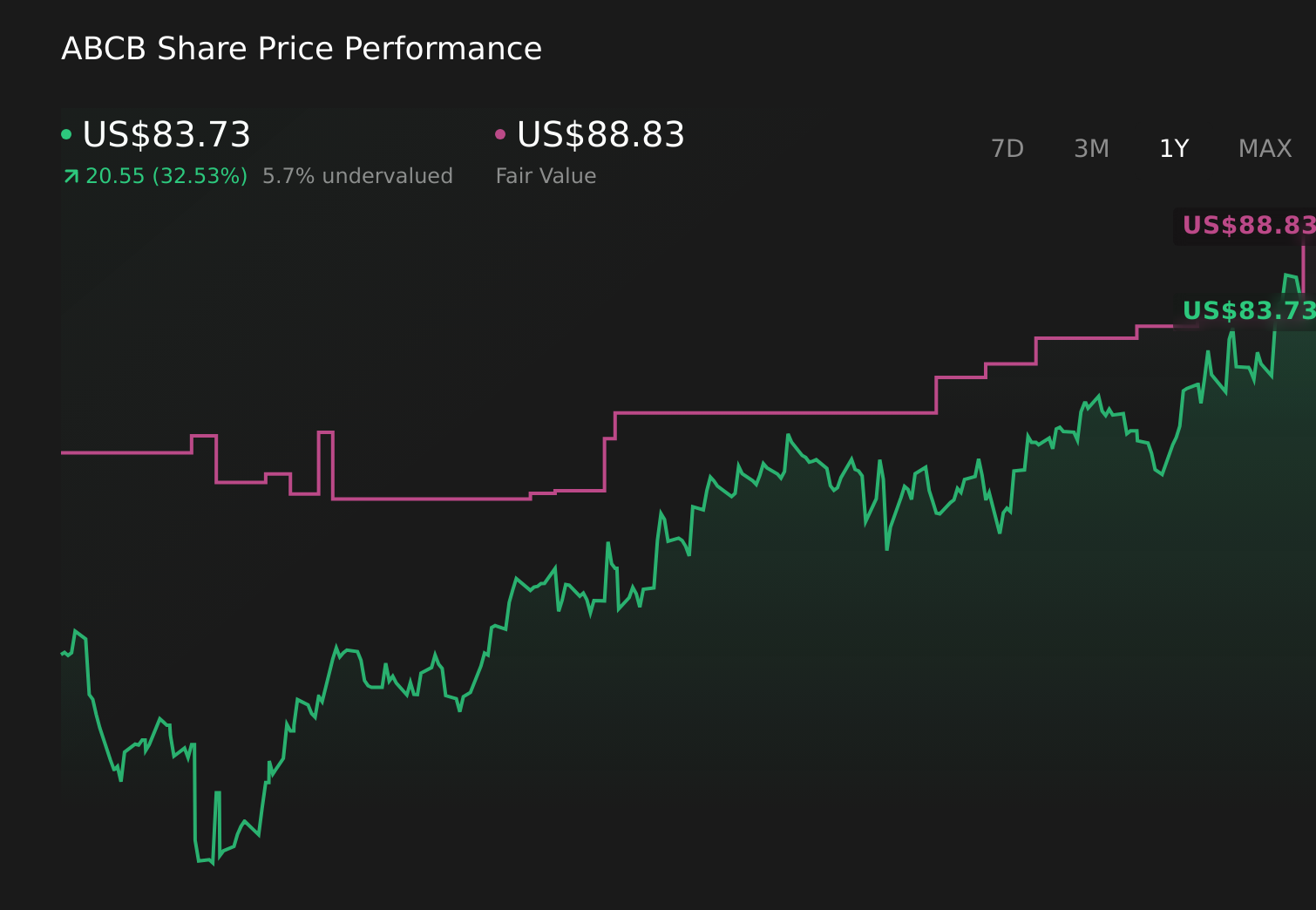

Ameris Bancorp's narrative projects $1.6 billion revenue and $502.9 million earnings by 2029. This requires 9.9% yearly revenue growth and about a $68.2 million earnings increase from $434.7 million today.

Uncover how Ameris Bancorp's forecasts yield a $93.86 fair value, a 10% upside to its current price.

Exploring Other Perspectives

One Simply Wall St Community member currently pegs Ameris Bancorp’s fair value at US$93.86, highlighting how a single view can differ from prevailing market pricing. Against that, the recent A+ EPS Revision Grade puts the focus firmly on whether competitive pressure on deposits and loans could alter the bank’s earnings trajectory, so it is worth comparing multiple viewpoints before deciding how you see the story.

Explore another fair value estimate on Ameris Bancorp - why the stock might be worth as much as 10% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ameris Bancorp research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Ameris Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ameris Bancorp's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.