How Investors May Respond To ArcBest (ARCB) Rising Sales, Small Loss, And Climate Governance Pushback

ArcBest Corporation ARCB | 0.00 |

- ArcBest Corporation has reported past first-quarter 2026 results showing sales of US$998.79 million versus US$967.08 million a year earlier, alongside a shift from US$3.13 million in net income to a US$1.04 million net loss, while also continuing share repurchases, maintaining its US$0.12 dividend, and facing a failed shareholder proposal on GHG emissions targets.

- This combination of higher revenue but a small loss, ongoing capital returns through buybacks and dividends, and shareholder pushback on climate targets gives investors a multi-faceted view of ArcBest’s financial discipline and governance priorities.

- Now we’ll examine how ArcBest’s higher revenue but modest quarterly loss may influence its existing investment narrative and outlook.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

ArcBest Investment Narrative Recap

To own ArcBest, you need to believe it can translate its LTL and logistics footprint, plus its tech investments, into healthier margins over time despite freight cyclicality and cost pressure. The latest quarter’s higher sales but US$1.04 million net loss is small in absolute terms and does not materially change that bigger picture, though it does keep near term profitability and rate pressure firmly in focus as key risks.

The continued US$0.12 quarterly dividend is the most relevant recent announcement here, because it sits alongside share repurchases and a modest loss. Together, these moves show ArcBest still returning cash while earnings remain under pressure, which matters if you see capital returns as a short term support for the stock even as freight demand, pricing, and cost control remain the main catalysts to watch.

Yet against this steady dividend, investors should be aware of the risk that soft freight conditions and rising costs could...

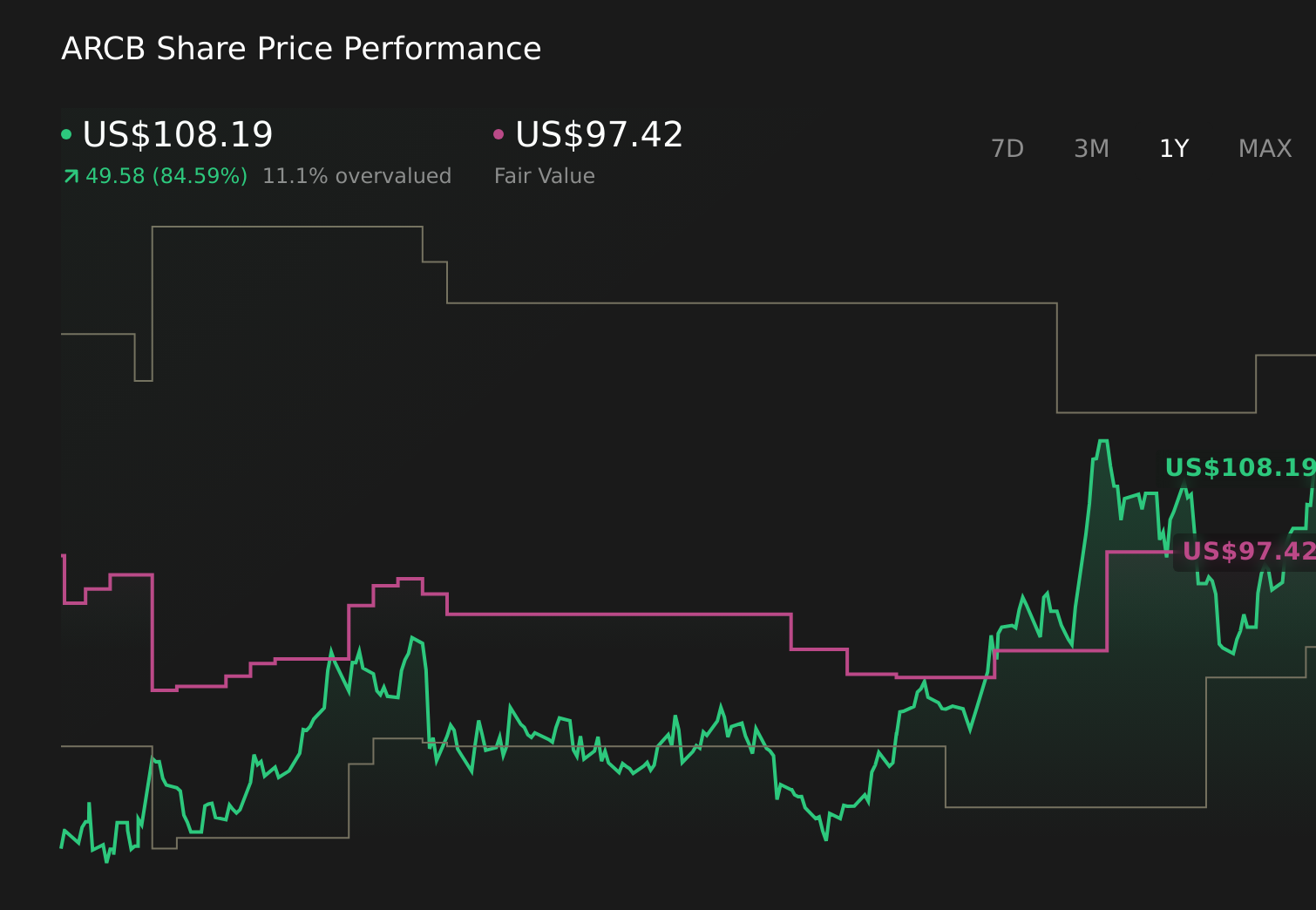

ArcBest’s narrative projects $4.5 billion revenue and $147.2 million earnings by 2028. This requires 3.9% yearly revenue growth and a $11.1 million earnings decrease from $158.3 million today.

Uncover how ArcBest's forecasts yield a $97.42 fair value, a 20% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously penciling in about US$5.2 billion of revenue and US$213.7 million of earnings by 2029, which is far more positive than the baseline view, but results like this quarter’s small loss and the risk of larger e commerce players building their own logistics networks may lead you to question whether that faster growth path still feels realistic.

Explore 3 other fair value estimates on ArcBest - why the stock might be worth 39% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your ArcBest research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ArcBest research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ArcBest's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.