How Investors May Respond To Bank of America (BAC) Stress Test Win, New Debt Issuance and Q2 Earnings

Bank of America Corp BAC | 0.00 |

- In recent weeks, Bank of America has passed the Federal Reserve’s 2026 stress tests, redeemed US$2.60 billion of senior notes, and issued multiple new senior unsecured fixed‑income offerings across currencies and maturities.

- Together with extending large credit facilities to AI firms, exploring a purchase of Fiserv’s debit network, and activating its FIFA World Cup 2026 sponsorship, the bank is sharpening its focus on payments infrastructure, funding flexibility and brand reach across retail and institutional clients.

- We’ll now examine how Bank of America’s expanded fixed‑income funding and forthcoming Q2 earnings could influence its existing investment narrative.

The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Bank of America Investment Narrative Recap

To own Bank of America, you need to believe in its ability to compound earnings through a broad, diversified franchise while managing credit quality and funding costs. The near term catalyst is Q2 earnings and any update on capital returns, while key risks still center on credit conditions, deposit competition and litigation expenses. The latest wave of senior note issuance and redemptions fine tunes its funding profile but does not materially change these near term drivers.

The decision to redeem US$2.60 billion of senior bank notes due August 2026 sits most directly alongside the new fixed income offerings. Together, these show Bank of America actively refreshing its debt stack across currencies and maturities, which interacts with the existing catalyst around asset repricing and interest rate management by shaping future net interest income and overall funding flexibility.

Yet even as funding looks orderly, investors still need to be aware of how rising competition for deposits could...

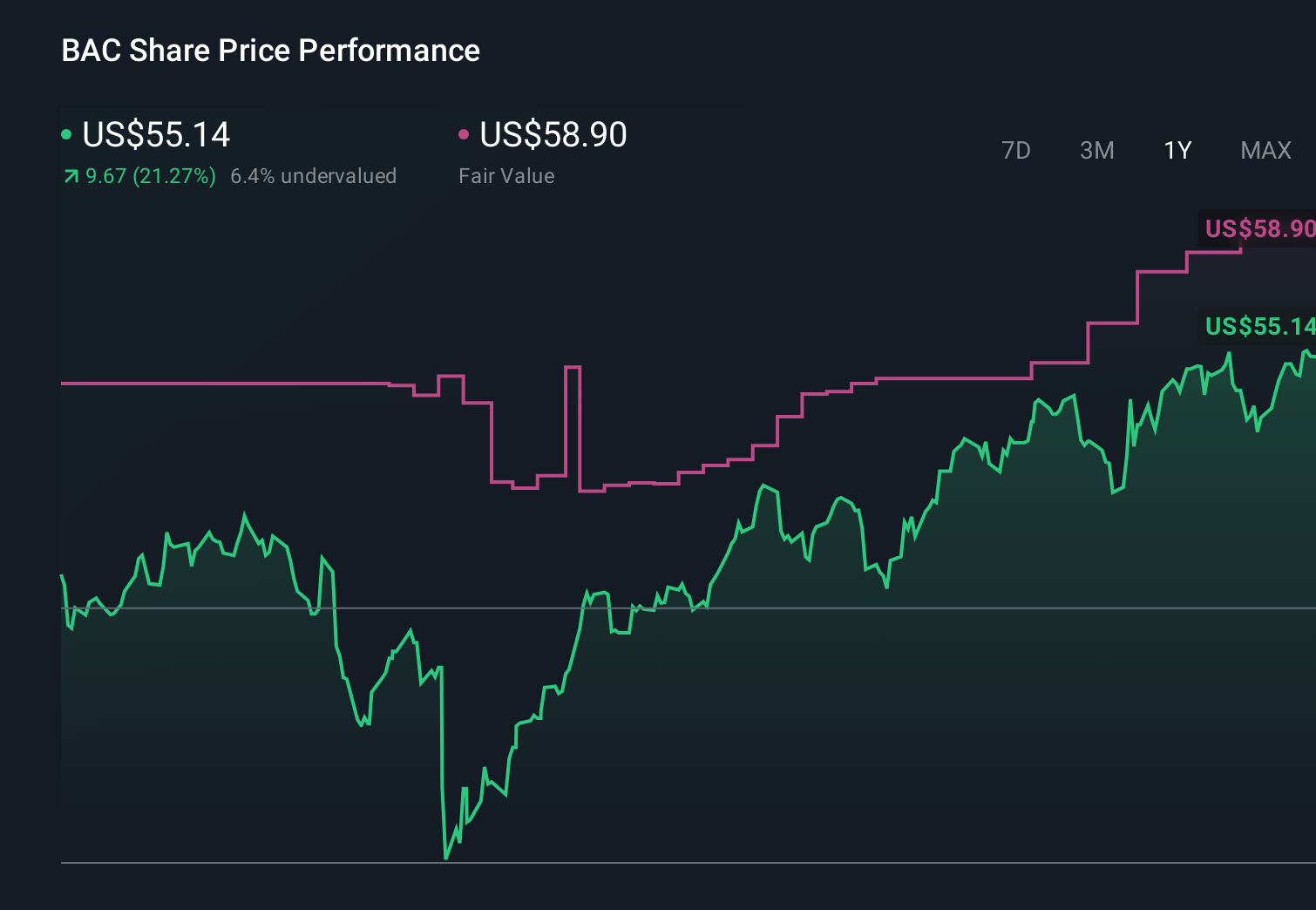

Bank of America's narrative projects $133.8 billion revenue and $36.9 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $6.6 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $64.83 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community cluster between US$64.83 and US$71.86, underlining how differently individual investors can view the same bank. Against this spread, the baseline catalyst around digital and AI driven efficiency gains raises important questions about how you think Bank of America’s earnings power could evolve over time, so it is worth comparing several viewpoints before deciding what the stock is really worth.

Explore 3 other fair value estimates on Bank of America - why the stock might be worth as much as 20% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.