How Investors May Respond To Boeing (BA) Asia-Pacific Jet Orders And Backlog-Driven Earnings Recovery Hopes

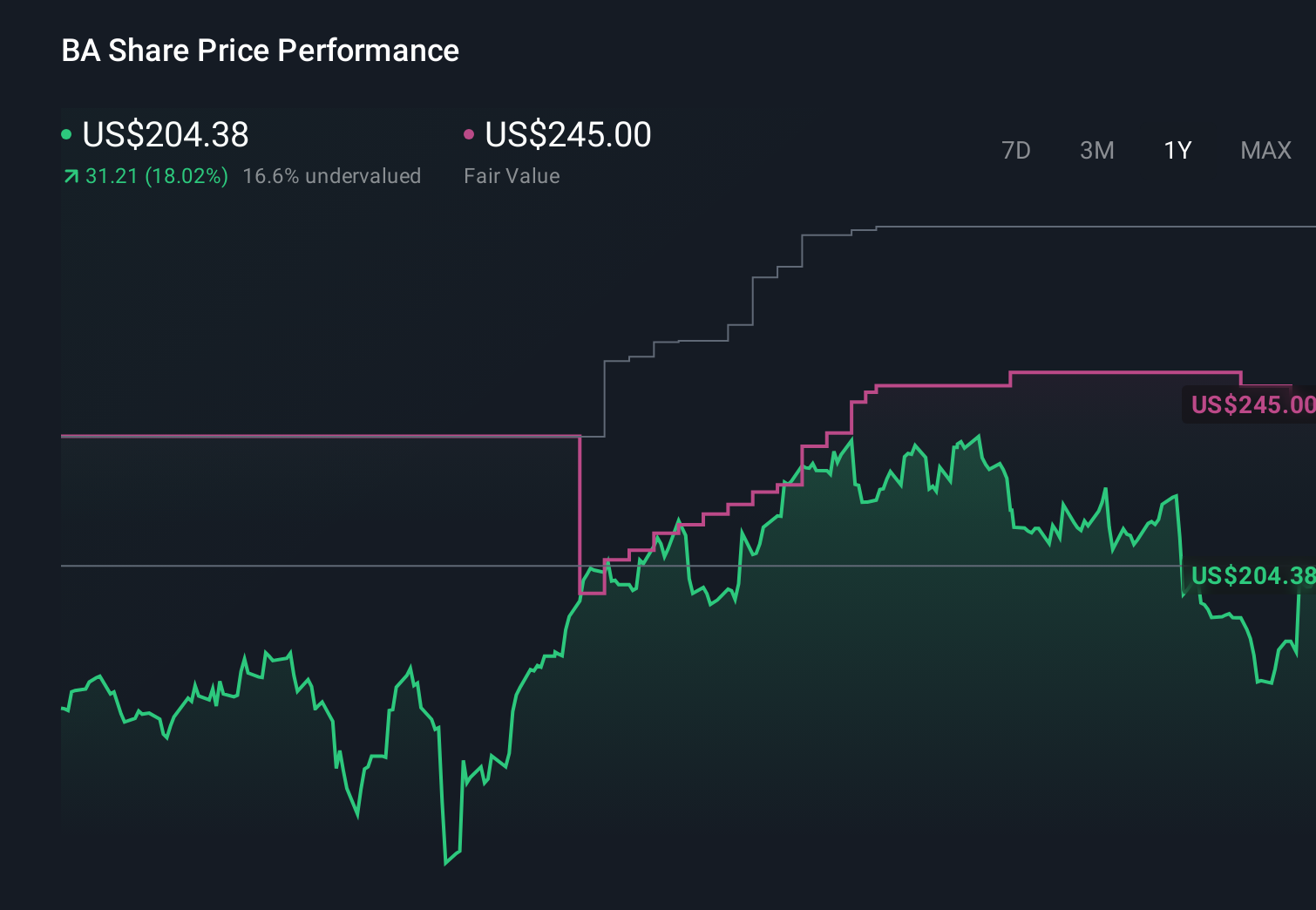

Boeing Company BA | 208.22 | +0.43% |

- Boeing recently confirmed major commercial aircraft deals, including up to 40 787 Dreamliners for Sun PhuQuoc Airways and 50 737 MAX jets for Vietnam Airlines, adding to its reported US$682.00 billion order backlog.

- These widebody and narrowbody commitments highlight how demand across both long- and short-haul fleets could influence Boeing's efforts to improve profitability and production consistency after weak core margins and reliance on one-off gains.

- Now we’ll examine how these substantial Asia-Pacific aircraft orders might reshape Boeing’s investment narrative around backlog quality and earnings recovery.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Boeing Investment Narrative Recap

To own Boeing today, you need to believe that its large commercial backlog and improving cash generation can eventually offset weak core margins, high debt and ongoing certification and quality challenges. The recent Asia Pacific orders add useful visibility, but they do not materially change the near term catalyst, which remains evidence of cleaner, recurring earnings from Boeing Commercial Airplanes, or the key risk around execution on 737 and 787 production and certification.

Among recent announcements, the finalized order for 50 737 MAX jets from Vietnam Airlines is most relevant. It directly links to Boeing’s need to prove it can convert strong single aisle demand into timely deliveries and better margins, while managing certification issues on other 737 variants. How efficiently Boeing executes on deals like this will be central to whether its large backlog translates into healthier earnings rather than more pressure on working capital.

Yet beneath these headline orders, investors should also be aware that Boeing’s high debt load could still ...

Boeing's narrative projects $114.4 billion revenue and $7.1 billion earnings by 2028. This requires 14.9% yearly revenue growth and an earnings increase of about $18.0 billion from $-10.9 billion today.

Uncover how Boeing's forecasts yield a $247.04 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far more cautious picture, assuming only about US$109.7 billion of revenue and US$4.0 billion of earnings by 2028, so you should weigh this more pessimistic view against the recent orders and consider how your own expectations might differ if these forecasts prove too low or need revising after the latest news.

Explore 10 other fair value estimates on Boeing - why the stock might be worth just $247.04!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.