How Investors May Respond To Boeing (BA) Securing Fresh China Southern Freighter Orders

Boeing Company BA | 0.00 |

- In late June 2026, China Southern Airlines announced that its 55%-owned cargo subsidiary agreed to buy five new Boeing 777‑8F and two 777F freighters, plus options for three more 777‑8F aircraft, with catalogue pricing for the initial seven jets totaling about US$3.62 billion before undisclosed concessions.

- This sizeable long-haul freighter order signals renewed commercial traction for Boeing in China’s aviation market, while also reinforcing the company’s role in supporting expanding cross‑border e‑commerce and cargo demand along key trade corridors.

- We’ll now examine how this fresh China Southern freighter commitment could influence Boeing’s investment narrative built around backlog strength and operational recovery.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Boeing Investment Narrative Recap

To own Boeing today, you need to believe that its large backlog and production recovery can translate into sustained profitability while the company manages high debt and lingering execution issues. The China Southern 777 freighter deal strengthens the backlog story and hints at improved access to China, but it does not fundamentally change the near term focus on stabilizing 737 programs and protecting margins, nor does it remove the key risk around quality, certification, and production disruptions.

Among recent announcements, the unplanned IT outage that disrupted quarter end deliveries is most relevant here, because it highlights how operational hiccups can still interfere with Boeing’s ability to convert backlog into completed aircraft and cash. In that context, new widebody orders like China Southern’s help on the demand side, but the investment narrative still depends on Boeing proving it can execute consistently at higher production rates.

Yet behind the backlog headlines, investors should also be aware that Boeing’s elevated debt and operational setbacks could still...

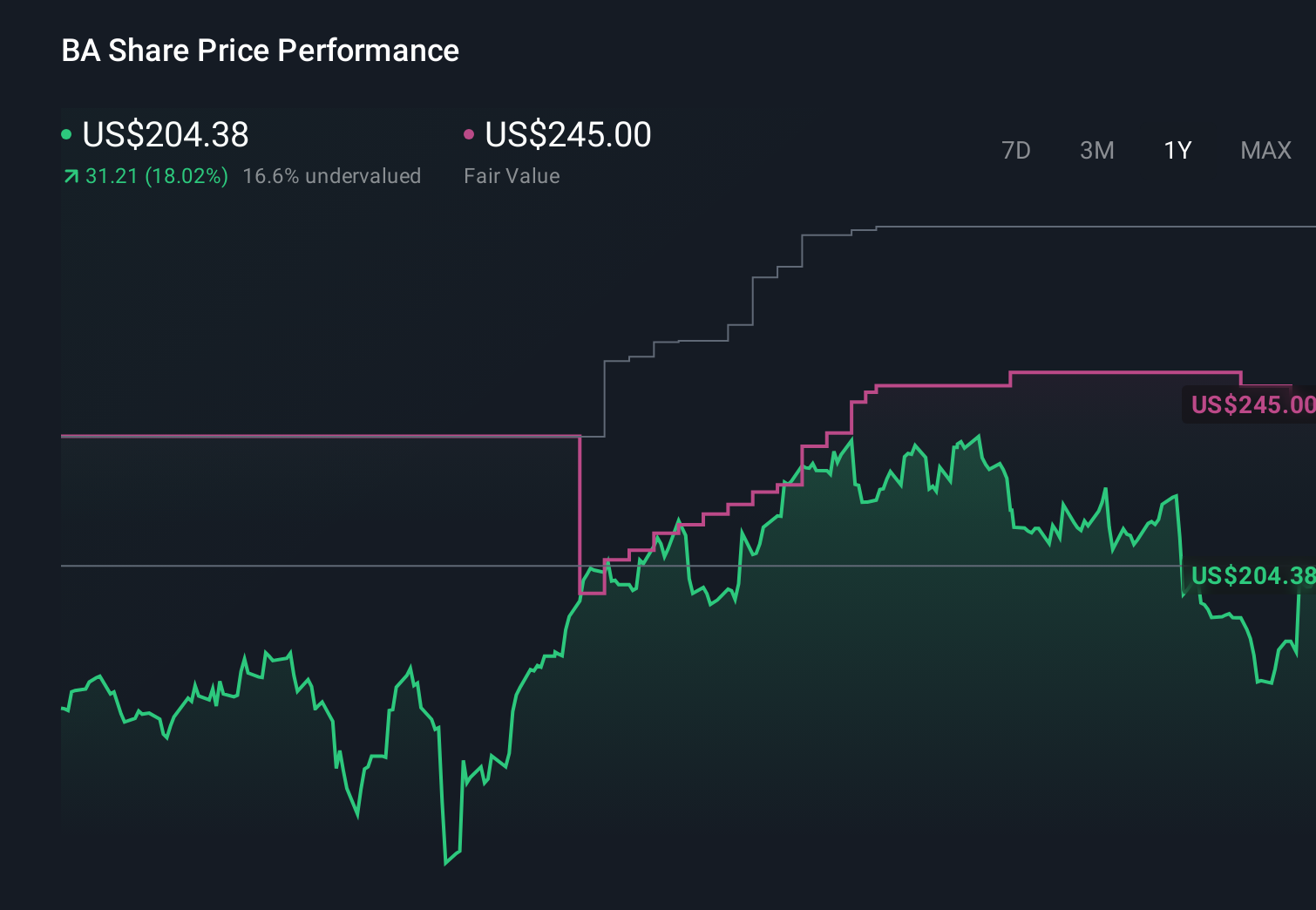

Boeing's narrative projects $125.6 billion revenue and $7.9 billion earnings by 2029. This requires 10.9% yearly revenue growth and a $6.0 billion earnings increase from $1.9 billion today.

Uncover how Boeing's forecasts yield a $270.00 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already baking in revenue near US$132.7 billion and earnings of about US$11.7 billion by 2028, but this China Southern order and the ongoing operational risks you just read about could either support that bullish view or reinforce the more cautious one you have seen here, which is why it is worth comparing how differently analysts weigh supply chain and execution risk around Boeing’s recovery story.

Explore 8 other fair value estimates on Boeing - why the stock might be worth as much as 81% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boeing research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

No Opportunity In Boeing?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.