How Investors May Respond To Credit Acceptance (CACC) Hiring a New Chief Sales Officer

Credit Acceptance Corporation CACC | 0.00 |

- In late April 2026, Credit Acceptance Corporation reported that Robert Bourrier has joined as Chief Sales Officer, tasked with leading and scaling the national sales organization to drive disciplined revenue growth, market share expansion, and consistent execution across all markets.

- This hire brings more than 25 years of sales and commercial leadership experience from sectors such as private aviation and global airlines, signaling a push to tighten sales execution, strengthen performance management, and support disciplined growth in Credit Acceptance’s core auto finance business.

- We’ll now examine how Bourrier’s mandate to strengthen national sales execution and dealer-facing go-to-market efforts could influence Credit Acceptance’s investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Credit Acceptance Investment Narrative Recap

To own Credit Acceptance, you need to believe its non prime auto finance model can still generate attractive returns despite credit and competitive pressures, and that recent leadership changes will sharpen execution. The Bourrier hire appears directionally helpful for addressing softer dealer volumes and competition, but it does not materially change the near term catalyst around loan performance trends or the key risk that weaker 2022 to 2024 vintages could pressure margins and returns.

The most relevant nearby announcement is the upcoming first quarter 2026 earnings release and webcast on May 5, which should give investors fresh insight into loan performance, unit volumes, and how the expanded leadership bench, including the new Chief Sales Officer, is influencing dealer engagement and national sales productivity.

Yet even with this new sales leadership, investors should be aware that...

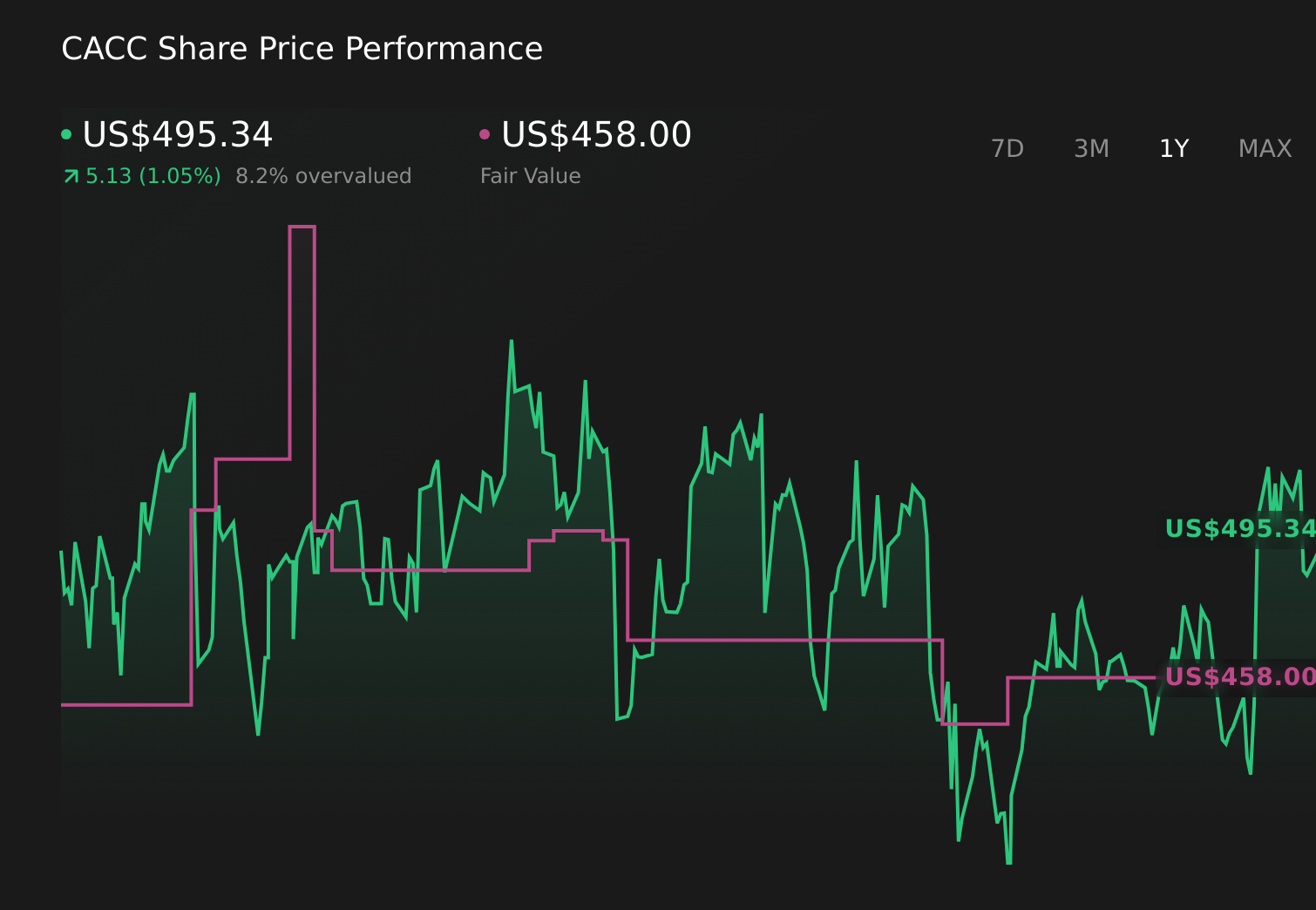

Credit Acceptance's narrative projects $3.3 billion revenue and $659.5 million earnings by 2029.

Uncover how Credit Acceptance's forecasts yield a $481.67 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have only two fair value estimates for Credit Acceptance, ranging from about US$318 to US$482 per share, highlighting very different conclusions about upside. When you set those views against the risk that recent loan vintages continue to underperform and compress margins, it becomes clear that you should compare several perspectives before forming your own view.

Explore 2 other fair value estimates on Credit Acceptance - why the stock might be worth as much as $481.67!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Credit Acceptance research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Credit Acceptance research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Credit Acceptance's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.