How Investors May Respond To DoorDash (DASH) Exiting Markets While Doubling Down On AI Pizza Customization

DoorDash, Inc. Class A DASH | 148.01 149.86 | +0.96% +1.25% Pre |

- In late February 2026, DoorDash said it would exit Qatar, Singapore, Japan and Uzbekistan while simultaneously rolling out new platform capabilities across advertising, AI-powered pizza customization, restaurant reservations, loyalty integrations and delivery partnerships.

- This mix of market exits and product launches underlines DoorDash’s effort to concentrate resources on offerings and geographies where it sees clearer long-term leadership potential.

- We’ll now examine how DoorDash’s AI-powered pizza customization rollout may influence its previously outlined investment narrative and long-term thesis.

Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

DoorDash Investment Narrative Recap

To own DoorDash, you need to believe its logistics and software platform can keep widening its role in how consumers buy food and everyday goods, while new revenue streams help offset rising labor and regulatory pressures. The recent exits from Qatar, Singapore, Japan and Uzbekistan look immaterial to the near term catalyst around improving profitability and ad growth, but they do slightly reduce the execution risk of spreading resources across too many small markets.

The AI powered pizza customization rollout is the clearest tie to this shift, because it speaks directly to DoorDash’s core catalyst: using software to deepen consumer engagement and help merchants sell more without adding complexity. If this type of experience scales into other cuisines and verticals, it could strengthen order frequency and ad relevance at the same time, which is where a lot of the long term earnings thesis is currently anchored.

Yet beneath this optimism, investors should be aware that rising labor and regulatory costs could still...

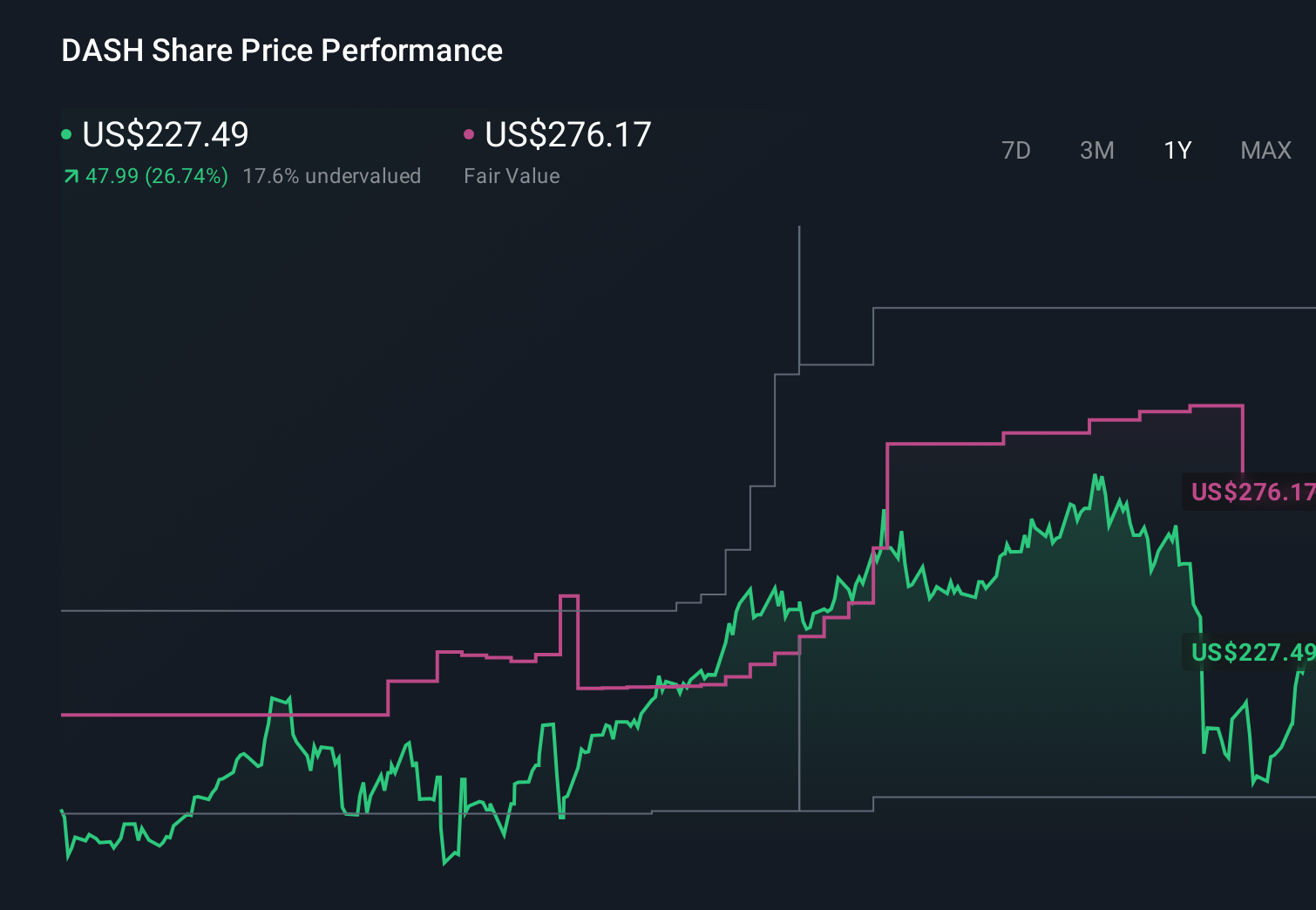

DoorDash's narrative projects $20.4 billion revenue and $3.2 billion earnings by 2028. This requires 19.6% yearly revenue growth and a $2.4 billion earnings increase from $781.0 million today.

Uncover how DoorDash's forecasts yield a $260.90 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were modeling revenue around US$21.9 billion and earnings near US$4.8 billion by 2028, but if you are counting on aggressive AI driven cost savings to get there, the latest exits and product shifts are a reminder that these bullish views might need updating as the real world impact of DoorDash’s investments becomes clearer.

Explore 14 other fair value estimates on DoorDash - why the stock might be worth just $212.04!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your DoorDash research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DoorDash research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DoorDash's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.