How Investors May Respond To Dow (DOW) Deeper Q1 Losses And New ESOP-Linked Equity Shelf

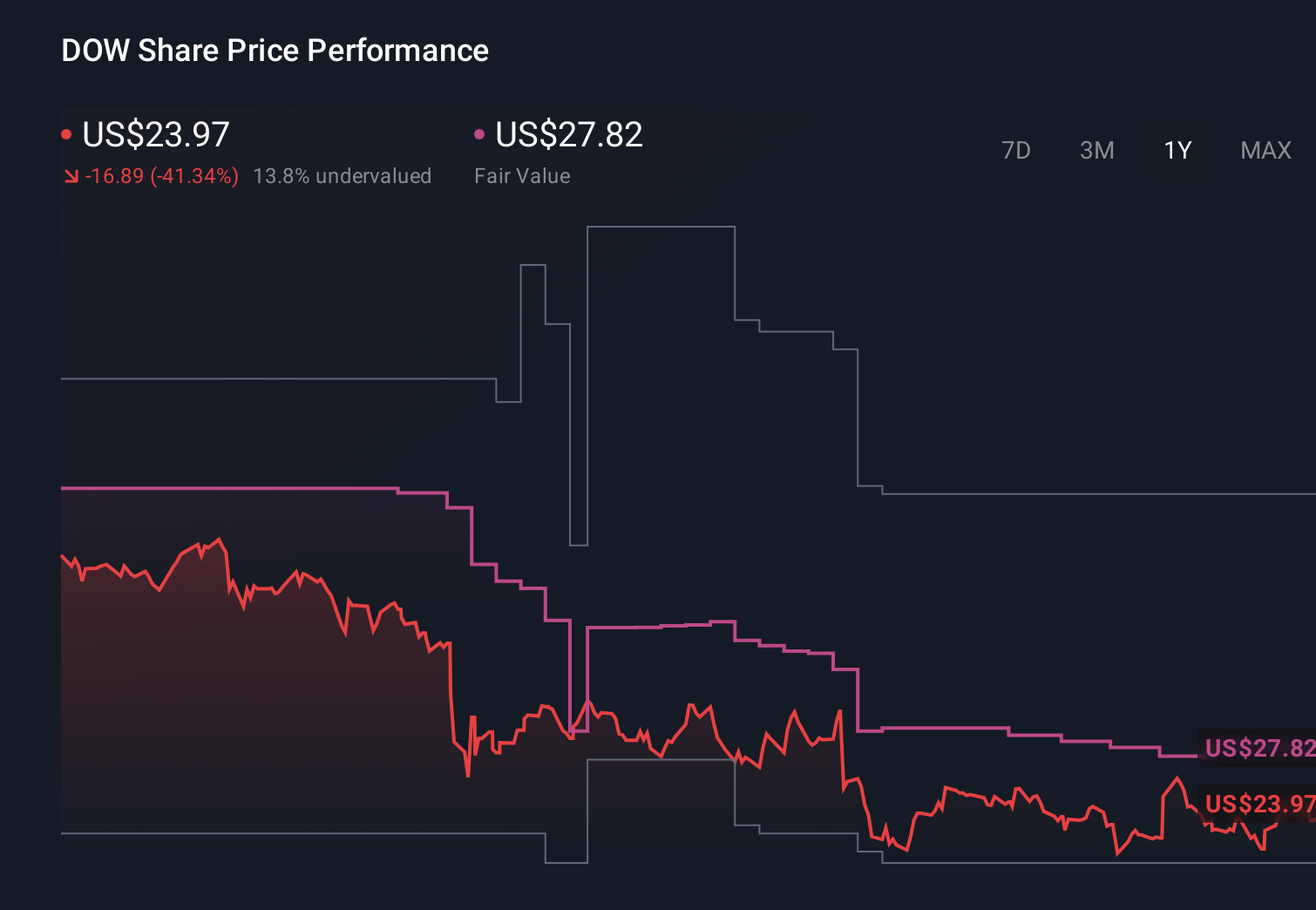

Dow, Inc. DOW | 0.00 |

- In late April 2026, Dow Inc. reported first‑quarter 2026 results showing sales of US$9,794 million versus US$10,431 million a year earlier and a net loss of US$533 million versus US$307 million, and subsequently filed a US$2.31 billions shelf registration for up to 60,000,000 common shares linked to an ESOP-related offering.

- This combination of wider quarterly losses driven by weaker pricing and volumes, alongside preparations to issue ESOP-related equity, highlights how Dow is balancing employee ownership with profit pressures.

- With Dow’s deeper quarterly loss underscoring margin pressure, we’ll now examine what this means for the company’s existing investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

Dow Investment Narrative Recap

To own Dow today, you need to be comfortable with a materials business working through weak pricing, softer volumes, and ongoing losses while relying on cost cuts, asset rationalization, and selective capital spending to restore profitability. The wider Q1 2026 loss and the US$2.31 billion ESOP‑related shelf do not appear to change the core near term catalyst, which remains execution on cash generation and margin repair, but they do reinforce the immediate risk around sustained earnings pressure.

Among recent developments, the CEO transition announced in mid April stands out in light of these results. Jim Fitterling will move to Executive Chair and Karen S. Carter, with deep operational experience at Dow, will become CEO in July 2026. For investors focused on catalysts, this handover puts extra attention on how management follows through on cost reduction targets, asset reviews, and capital allocation choices as the company works through weaker margins.

Yet against this focus on leadership and cost control, one important risk investors should be aware of is how persistent margin pressure could combine with...

Dow's narrative projects $45.1 billion revenue and $1.6 billion earnings by 2029. This requires 4.6% yearly revenue growth and about a $4.5 billion earnings increase from -$2.9 billion today.

Uncover how Dow's forecasts yield a $42.94 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a far harsher picture, assuming roughly flat revenue near US$39.7 billion and only about US$650 million of earnings by 2029, so if you worry that ongoing margin pressure and industry overcapacity could bite harder than consensus expects, it may be worth comparing your own expectations with these more pessimistic scenarios and considering how the latest quarterly loss and potential share issuance might shift those views.

Explore 6 other fair value estimates on Dow - why the stock might be worth 33% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Dow research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Dow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dow's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

- Find 50 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.