How Investors May Respond To Fortinet (FTNT) Ransomware Surge And AI-Driven Threats Spotlighted In New Report

Fortinet, Inc. FTNT | 0.00 |

- In late April and early May 2026, Fortinet released its 2026 Global Threat Landscape Report revealing a very large year-over-year jump in ransomware victims and rising AI-enabled cybercrime, while also preparing to report quarterly earnings on 6 May with analysts expecting higher earnings per share and revenue.

- The combination of Fortinet’s heightened role in global cybercrime disruption, including law-enforcement collaborations and a new Cybercrime Bounty program, and improving analyst expectations has sharpened focus on how effectively its technology and threat intelligence translate into recurring revenue strength.

- We’ll now examine how the surge in AI-enabled cyber threats highlighted in Fortinet’s report influences the company’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 37 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Fortinet Investment Narrative Recap

To own Fortinet, you need to believe that rising cyber risk translates into durable demand for its integrated security platform and expanding software and services mix. The latest Threat Landscape Report, with its surge in AI-enabled attacks and ransomware, reinforces that demand backdrop and keeps attention on near term earnings delivery and billings growth as key catalysts. The biggest current risk is that hardware driven strength fades faster than higher margin subscriptions can compensate.

The recent launch of FortiOS 8.0 and expanded FortiAI capabilities is particularly relevant here, as it ties Fortinet’s core platform directly to the AI driven threats highlighted in the new report. How effectively these AI and SASE features convert heightened threat awareness into recurring revenue will influence whether analysts’ expectations for improving EPS and revenue, and the ongoing firewall refresh cycle, remain a support or become a pressure point for the stock.

Yet beneath the headline growth story, investors should also be aware that...

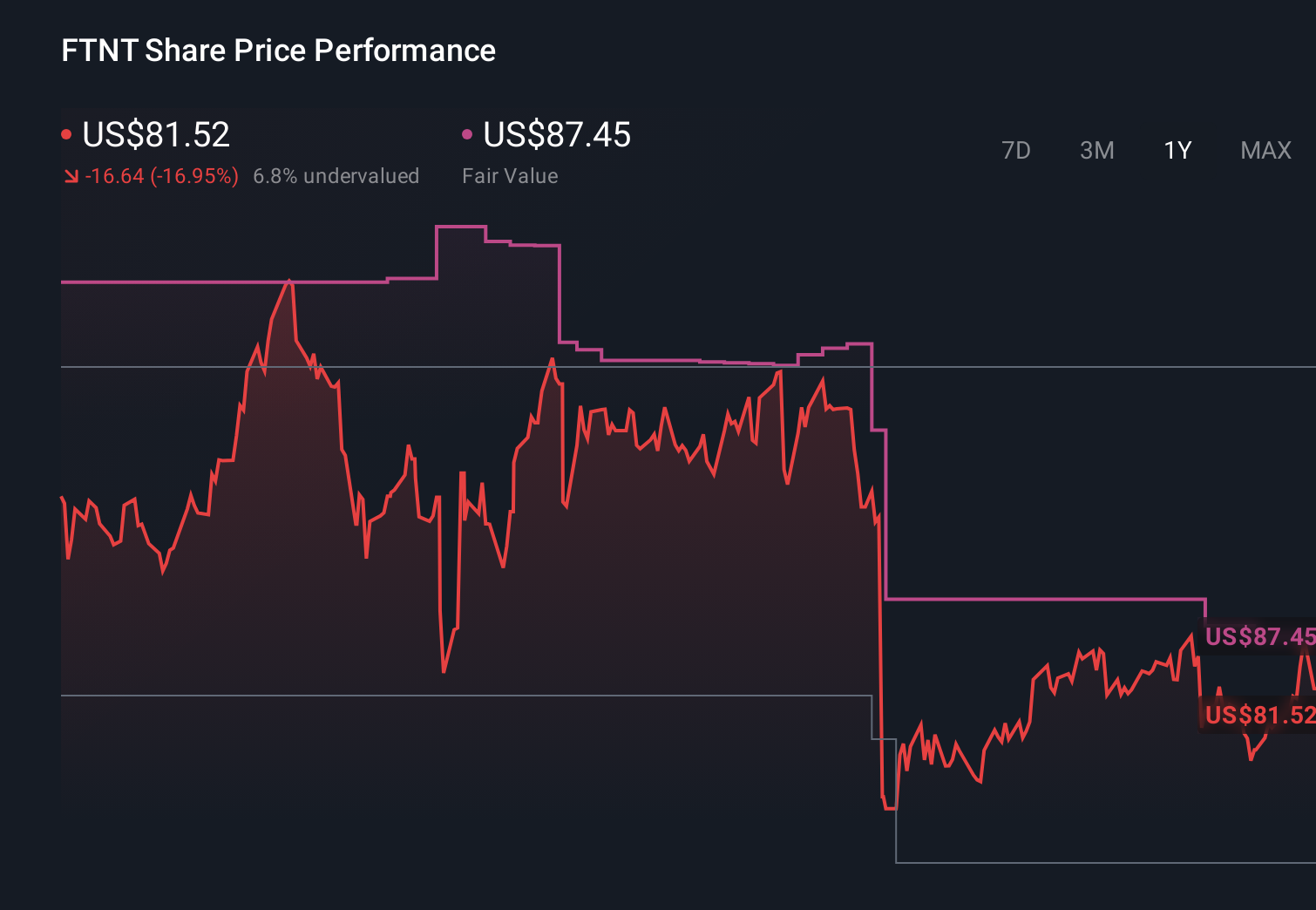

Fortinet's narrative projects $9.2 billion revenue and $2.5 billion earnings by 2029. This requires 10.6% yearly revenue growth and about a $0.6 billion earnings increase from $1.9 billion today.

Uncover how Fortinet's forecasts yield a $89.00 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much harsher picture, assuming revenue of about US$9.0 billion and only US$2.3 billion earnings by 2029, and warning that Fortinet’s hardware heavy model could be a real problem if customers accelerate their shift to cloud native security after AI driven attacks like those in the new report push them to consolidate on fewer platforms.

Explore 20 other fair value estimates on Fortinet - why the stock might be worth as much as 25% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Fortinet research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Fortinet research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fortinet's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.