How Investors May Respond To GE Vernova (GEV) Earnings, Debt Issuance, Buybacks and Data Center Demand

GE Vernova Inc. GEV | 898.57 | +0.42% |

- In early February 2026, GE Vernova reported past 2025 results showing revenue of US$10,956 million in Q4 and US$38,068 million for the year, alongside net income of US$3,664 million for Q4 and US$4,884 million for the full year, while also issuing multiple new senior unsecured bond offerings and completing share repurchases of 8,179,000 shares for US$3,343.5 million.

- Recent agreements with Maxim Power and Xcel Energy, combined with GE Vernova’s near 100 gigawatts gas power backlog and growing data center–linked turbine demand, underscore how its traditional utility-focused business is increasingly intertwined with hyperscaler-driven electricity needs.

- We’ll now examine how GE Vernova’s stronger earnings, deepening Xcel alliance, and data center-driven turbine demand affect its longer-term investment narrative.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

GE Vernova Investment Narrative Recap

To own GE Vernova, you need to believe that rising electricity demand from data centers and grid upgrades can support its mix of gas, wind, and electrification businesses while management manages project risk and capital intensity. The recent Q4 beat, larger dividend, and Maxim/Xcel agreements reinforce the near term catalyst of strong gas turbine and grid equipment demand, but they do not remove key risks around project delays, tariffs, and wind profitability.

The Xcel Energy Strategic Alliance looks especially important here, because it ties together gas turbines, wind projects, and grid equipment under a long term framework that could support more stable orders. For an investment case built on backlog quality and execution, that kind of multi decade relationship offers some visibility on future equipment and service work, even as the company continues to face lumpy infrastructure projects and ongoing restructuring efforts.

Yet even with this momentum, investors should be aware that concentrated exposure to large, lumpy grid and wind projects could still...

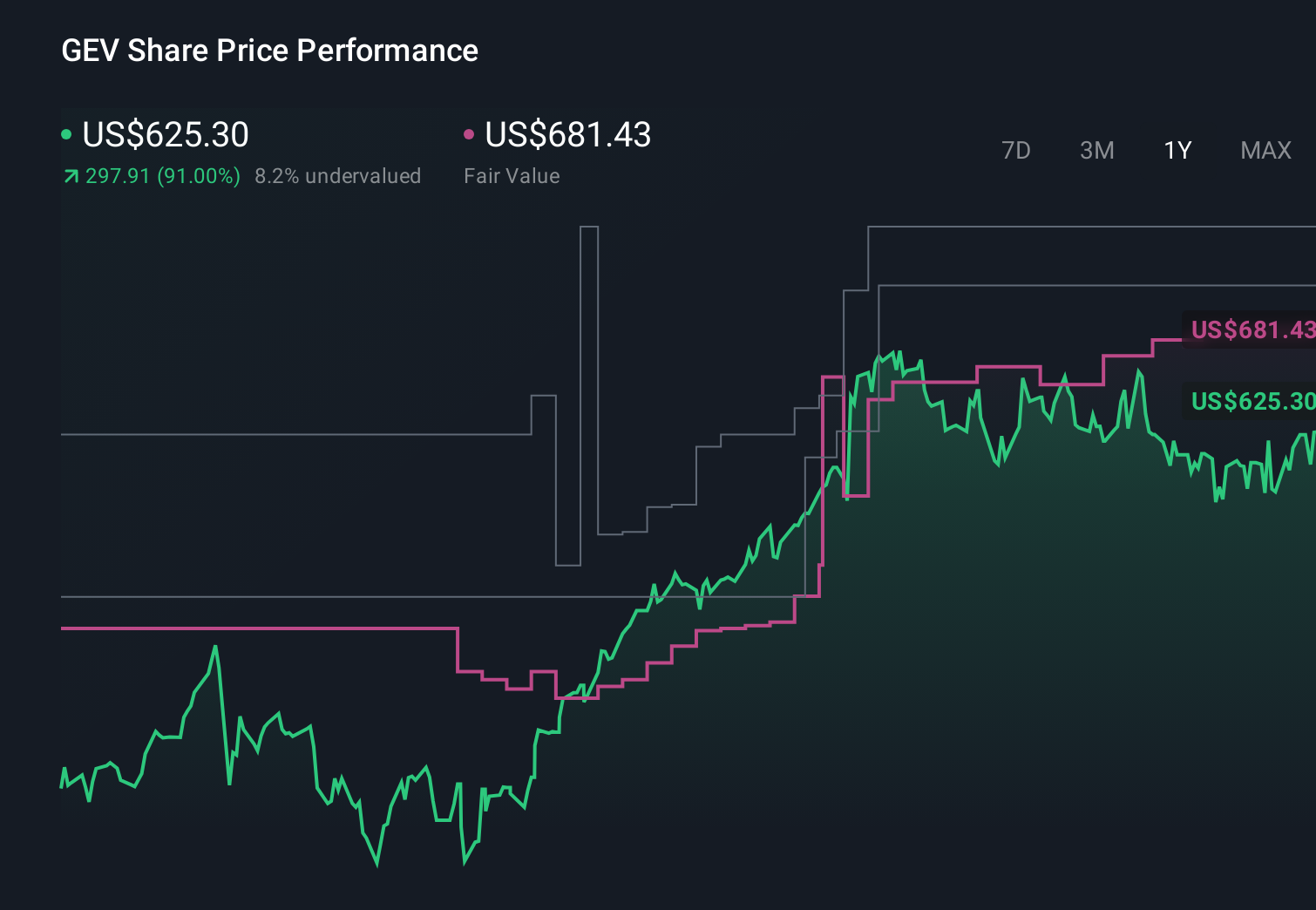

GE Vernova's narrative projects $48.0 billion revenue and $5.8 billion earnings by 2028. This requires 9.5% yearly revenue growth and about a $4.6 billion earnings increase from $1.2 billion today.

Uncover how GE Vernova's forecasts yield a $819.92 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue of about US$53.7 billion and earnings near US$7.7 billion by 2028, so if you worry about rising input costs and execution risk in wind and electrification, it is worth asking whether this new backlog news narrows that gap or makes those forecasts look even more stretched.

Explore 16 other fair value estimates on GE Vernova - why the stock might be worth 32% less than the current price!

Build Your Own GE Vernova Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your GE Vernova research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free GE Vernova research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate GE Vernova's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.