How Investors May Respond To Harrow (HROW) Taking Over BYOOVIZ US Commercialization And Ophthalmic Biosimilars

Harrow, Inc. HROW | 0.00 |

- In July 2026, Samsung Bioepis announced it had relaunched BYOOVIZ (ranibizumab-nuna) in the US, with Harrow (Nasdaq: HROW) now responsible for commercializing this Lucentis-referencing ophthalmology biosimilar and OPUVIZ (aflibercept-yszy), which references Eylea, following the transition of rights from Biogen.

- An important aspect of this development is BYOOVIZ’s FDA interchangeability designation, which, alongside its biosimilar pricing potential, may help reduce cost barriers for patients needing anti-VEGF therapies for conditions like wet age-related macular degeneration.

- We’ll now examine how Harrow’s expanded role in US ophthalmic biosimilars with BYOOVIZ could influence its existing investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Harrow Investment Narrative Recap

To own Harrow, you need to believe its expanding ophthalmic portfolio can offset heavy dependence on VEVYE, IHEEZO, and TRIESENCE while the company moves toward profitability. The BYOOVIZ relaunch and biosimilar role could support near term revenue and margin ambitions, but they also heighten execution and integration risk, which remains one of the biggest near term threats if uptake, pricing, or payer coverage disappoint.

Among recent updates, Harrow’s reaffirmed 2026 revenue guidance of US$350 million to US$365 million stands out against the BYOOVIZ news, because it frames how much incremental biosimilar contribution the market might be implicitly expecting. If biosimilar adoption proves slower or costlier than anticipated, that guidance could become harder to reach, especially given Harrow’s rising debt load and continued net losses.

Yet, while biosimilars may broaden Harrow’s opportunity set, investors should also weigh the risk that intensified pricing pressure and payer scrutiny could ultimately...

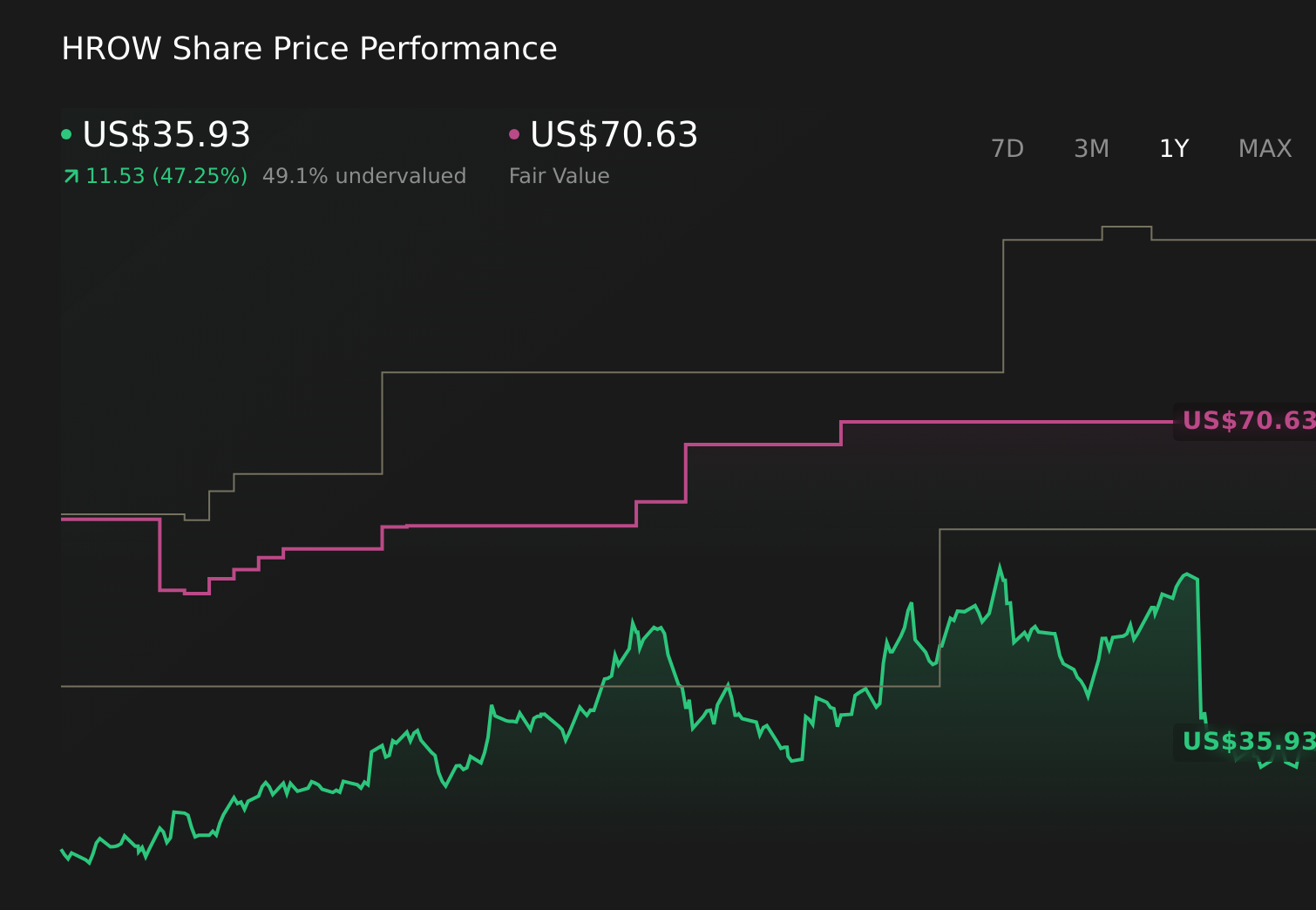

Harrow's narrative projects $784.8 million revenue and $246.0 million earnings by 2029.

Uncover how Harrow's forecasts yield a $68.38 fair value, a 59% upside to its current price.

Exploring Other Perspectives

This BYOOVIZ relaunch comes as the most optimistic analysts were already modeling Harrow revenue of about US$866 million and earnings near US$264 million by 2029, so if you thought biosimilars might simply add incremental upside, it is worth remembering those forecasts also assume concentration risk in key drugs stays manageable and pricing pressure does not undermine that growth path.

Explore 3 other fair value estimates on Harrow - why the stock might be worth just $59.00!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Harrow research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Harrow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harrow's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.