How Investors May Respond To Life Time (LTH) Buyback After Strong 2025 Results And 2026 Outlook

Life Time Group Holdings, Inc. LTH | 26.99 | +3.37% |

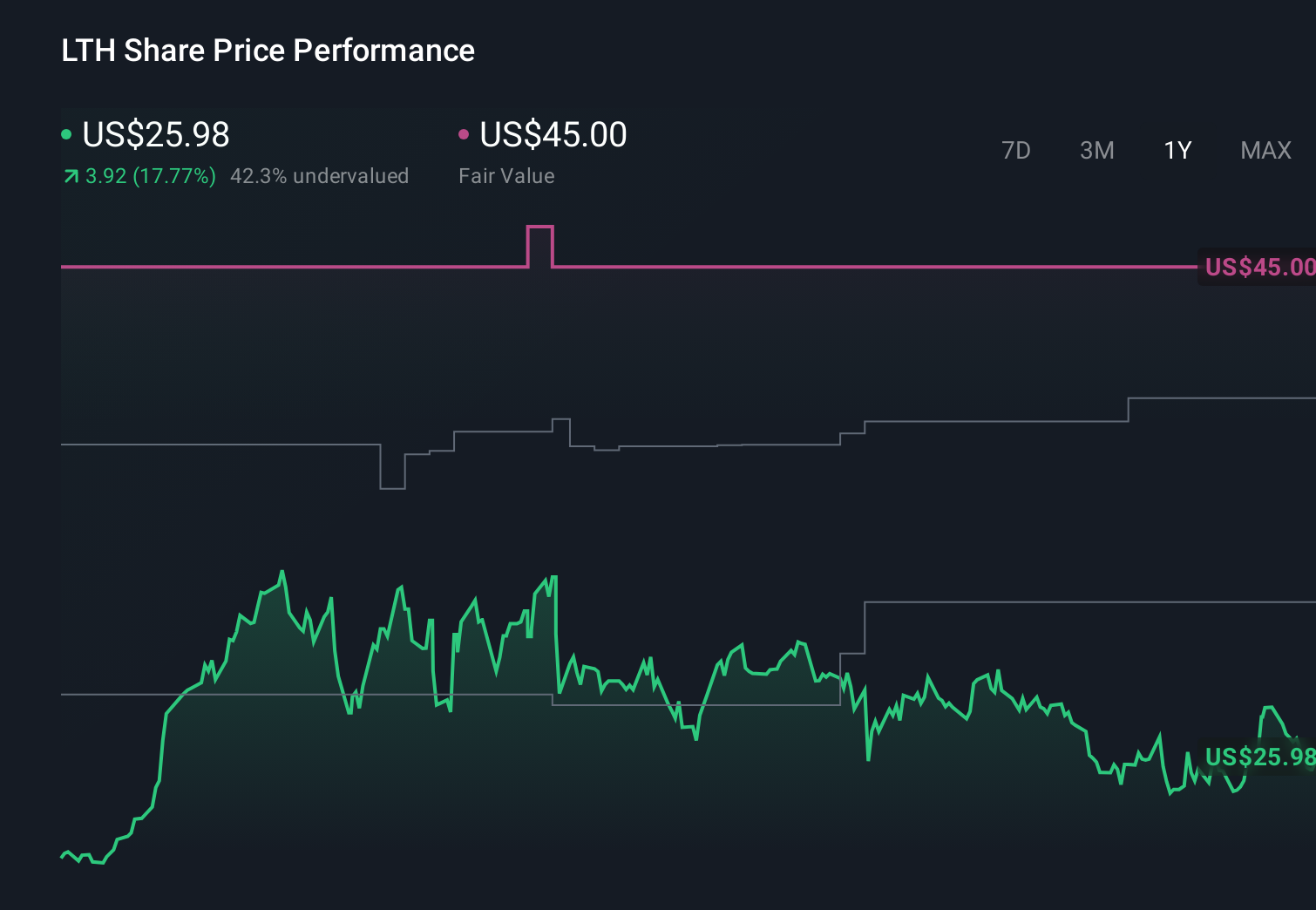

- In February 2026, Life Time Group Holdings, Inc. reported higher fourth-quarter and full-year 2025 revenue and net income versus 2024, reiterated its 2026 revenue and earnings guidance, and authorized a US$500 million share repurchase program with no expiration date.

- The combination of stronger profitability and a sizable, open-ended buyback plan highlights management’s confidence in the company’s cash generation and capital allocation priorities.

- Next, we’ll examine how this substantial share repurchase authorization might reshape Life Time’s investment narrative built around premium club expansion.

Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

Life Time Group Holdings Investment Narrative Recap

To own Life Time Group Holdings, you need to believe its premium, experience-focused clubs can keep attracting and retaining members while funding expansion without overstretching the balance sheet. The recent jump in 2025 revenue and net income, plus the new US$500 million share repurchase, does not remove the key near term catalyst or risk: execution on capital intensive club growth still hinges on healthy cash flow and access to sale leaseback financing.

The open ended buyback is the most relevant piece of news here, because it sits directly alongside heavy club growth spending and heightened debt levels. While 2026 guidance for US$3,300 million to US$3,330 million in revenue and US$330 million to US$336 million in net income frames expectations, the scale and timing of repurchases may influence how much financial flexibility Life Time retains if sale leaseback markets or borrowing costs change.

Yet beneath the strong 2025 earnings and large repurchase plan, investors should be aware of how reliant Life Time’s expansion remains on sale leaseback funding and...

Life Time Group Holdings' narrative projects $3.8 billion revenue and $457.9 million earnings by 2028. This requires 10.7% yearly revenue growth and a $231.1 million earnings increase from $226.8 million today.

Uncover how Life Time Group Holdings' forecasts yield a $40.18 fair value, a 48% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming roughly US$3.6 billion of revenue and US$361 million of earnings by 2028, so this buyback and club expansion push may either ease those sale leaseback and capex worries or reinforce them, and you should know that reasonable people can look at the same numbers and reach very different conclusions.

Explore 3 other fair value estimates on Life Time Group Holdings - why the stock might be worth as much as 66% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Life Time Group Holdings research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Life Time Group Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Life Time Group Holdings' overall financial health at a glance.

No Opportunity In Life Time Group Holdings?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.