How Investors May Respond To Moelis (MC) Earnings Miss Despite In-Line Revenue And Rising Cost Pressure

Moelis & Co. Class A MC | 0.00 |

- Earlier this year, Moelis & Company reported first-quarter revenue that matched analyst expectations but delivered earnings per share that fell well short of forecasts, highlighting higher-than-anticipated costs or margin pressure.

- This earnings miss came during a mixed quarter for independent advisers, where some peers exceeded both revenue and profit expectations, sharpening comparisons around Moelis’ efficiency and profitability.

- We’ll now explore how Moelis’ earnings shortfall, despite meeting revenue expectations, could influence the existing investment narrative around margin expansion.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Moelis Investment Narrative Recap

To own Moelis, you generally need to believe its advisory franchise can convert deal pipelines into healthy, sustainable margins without overextending on compensation and expansion. The recent Q1 earnings miss, despite in line revenue, puts the short term spotlight squarely on margin resilience and cost discipline, but the stock’s modest 1.9% pullback suggests the immediate impact on the core investment case and near term catalysts is noticeable rather than thesis breaking.

Against that backdrop, the fresh US$300 million buyback authorization, alongside active repurchases in early 2026, is particularly relevant. It underlines management’s willingness to return capital even as profitability comes under pressure, which can support per share metrics but also raises questions about how much flexibility Moelis retains if earnings volatility persists or deal activity softens more than expected.

Yet while capital returns may look reassuring, the real test for investors will be how Moelis copes with rising costs and...

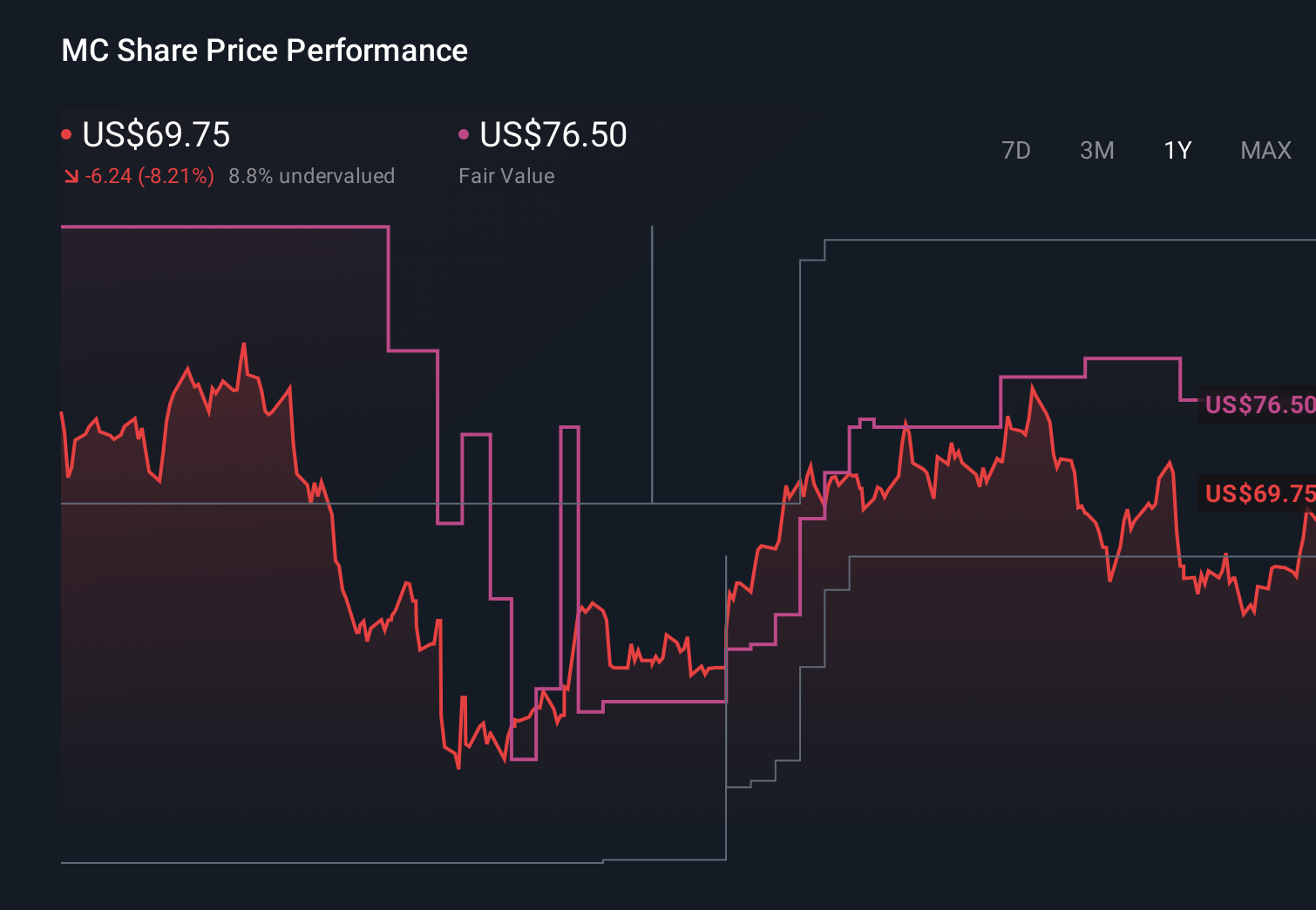

Moelis' narrative projects $2.1 billion revenue and $381.7 million earnings by 2028. This requires 15.3% yearly revenue growth and about a $183.6 million earnings increase from $198.1 million today.

Uncover how Moelis' forecasts yield a $76.50 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most pessimistic analysts were already assuming about US$2.3 billion of revenue and US$462.9 million of earnings by 2029, yet after this earnings miss you can see how views on heavy transaction dependence and margin pressure might widen further, so it is worth comparing those harsher expectations with more optimistic takes before deciding which story you believe.

Explore 3 other fair value estimates on Moelis - why the stock might be worth as much as 37% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Moelis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 12 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.