How Investors May Respond To Otter Tail (OTTR) Settling Key PVC Pipe Antitrust Claims

Otter Tail Corporation OTTR | 0.00 |

- On May 28, 2026, Otter Tail Corporation said its Northern Pipe Products and Vinyltech subsidiaries agreed to pay US$39.5 million and US$34.0 million, respectively, to settle two of three plaintiff classes in an industry-wide PVC pipe antitrust case, while continuing to contest remaining end‑user claims.

- The company plans to use existing cash for these settlements, which it does not expect to materially affect its financial position or liquidity, while emphasizing that the agreements involve no admission of wrongdoing.

- We’ll now examine how resolving most of this antitrust litigation, while end‑user claims persist, could influence Otter Tail’s investment narrative.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Otter Tail Investment Narrative Recap

To own Otter Tail, you need to believe in the resilience of its regulated utility and complementary manufacturing and plastics businesses, even as earnings are forecast to decline. The PVC antitrust settlements appear manageable relative to cash and are not expected to materially alter liquidity, but the unresolved end user claims keep legal and reputational risk on the table in the near term, which could matter more than usual given softer profit expectations.

The most relevant recent announcement alongside the settlements is Otter Tail’s reaffirmed 2026 EPS guidance of US$5.22 to US$5.62, issued with its first quarter 2026 results. Holding guidance steady while committing US$73.5 million to litigation settlements underlines management’s message that the core business can absorb these outflows, but it also sharpens the focus on how any adverse development in the remaining end user class could interact with already pressured earnings forecasts.

Yet investors should be aware that the unresolved end user PVC claims could still...

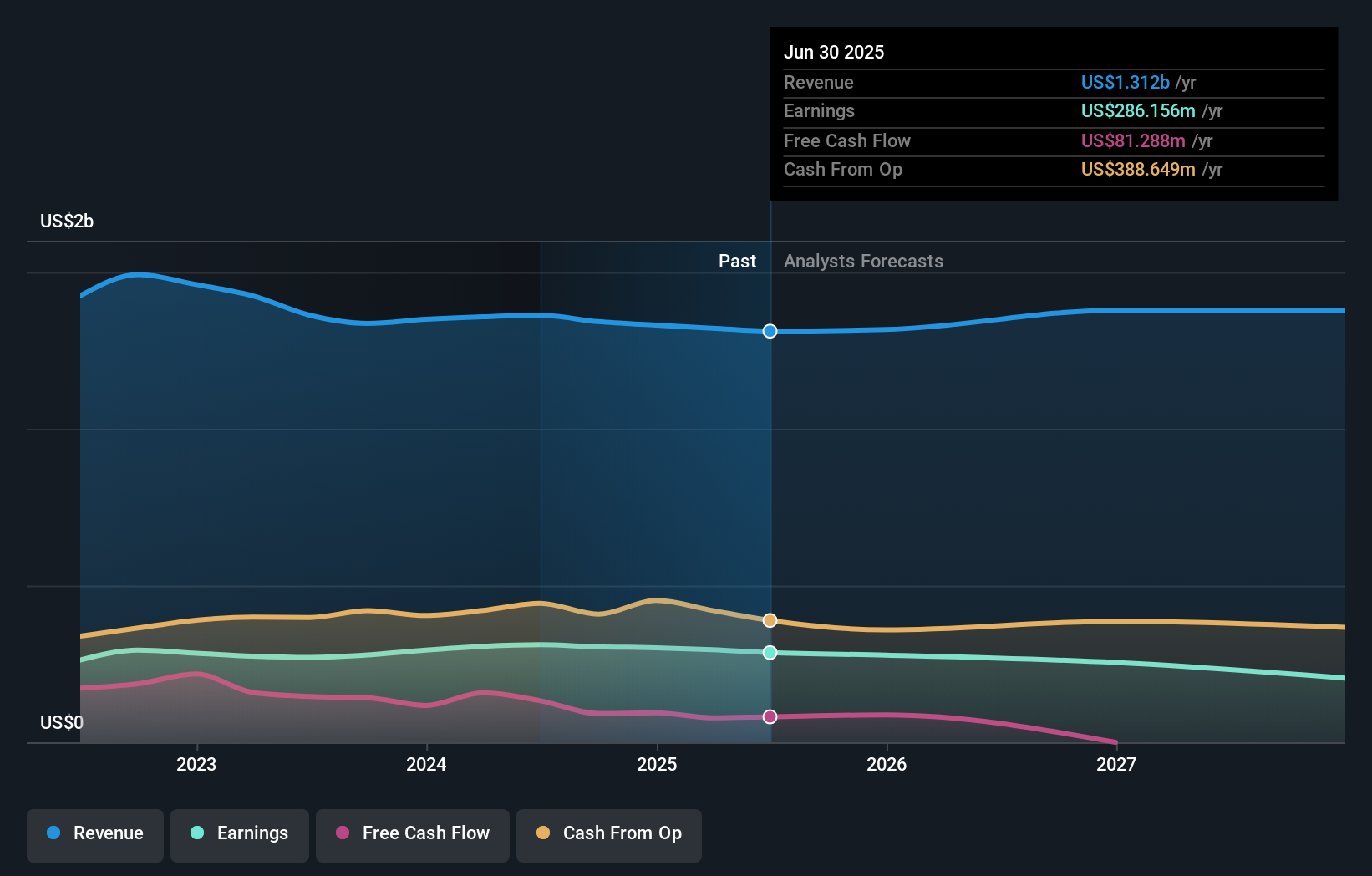

Otter Tail’s narrative projects $1.4 billion revenue and $205.5 million earnings by 2029. This implies 2.9% yearly revenue growth and an earnings decrease of about $74.9 million from $280.4 million today.

Uncover how Otter Tail's forecasts yield a $90.50 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Otter Tail span roughly US$65 to US$90. As you weigh those views, remember that unresolved PVC end user claims keep legal risk tied to the plastics segment and could influence how the earnings outlook evolves.

Explore 3 other fair value estimates on Otter Tail - why the stock might be worth 25% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Otter Tail research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Otter Tail research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Otter Tail's overall financial health at a glance.

No Opportunity In Otter Tail?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.