How Investors May Respond To ResMed (RMD) Leadership Shift And Capital Return Milestones

ResMed Inc. RMD | 0.00 |

- In late April 2026, ResMed reported higher third‑quarter and nine‑month sales and earnings, confirmed a US$0.60 quarterly dividend, completed its long-running share repurchase program, and announced that long-serving CFO Brett Sandercock would retire in May 2026 while remaining an advisor through 2027.

- The appointment of former Exact Sciences finance chief Aaron Bloomer as ResMed’s new CFO brings extensive global healthcare finance and capital allocation experience that could influence how the company funds growth, manages margins, and evaluates future M&A.

- Now we’ll examine how the appointment of experienced healthcare CFO Aaron Bloomer could influence ResMed’s investment narrative and execution priorities.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

ResMed Investment Narrative Recap

To own ResMed, you need to believe in ongoing demand for sleep and respiratory care, supported by an integrated hardware and digital ecosystem. The key near term catalyst remains execution on growth and margin initiatives, while a major risk is any hit to device demand from alternative therapies or reimbursement changes. The latest results and CFO transition do not appear to materially change those high level drivers, but they sharpen focus on capital allocation and cost control.

Among the recent announcements, the completion of the long running US$1,363.36 million share repurchase program stands out. It closes a multi year capital return effort just as ResMed reports higher sales and earnings, and confirms a US$0.60 quarterly dividend. Together, these updates frame how the new CFO may think about balancing reinvestment, potential M&A and ongoing shareholder returns relative to the company’s key growth catalysts.

Yet while the headline story looks constructive, investors should also be aware of the risk that GLP 1 therapies could...

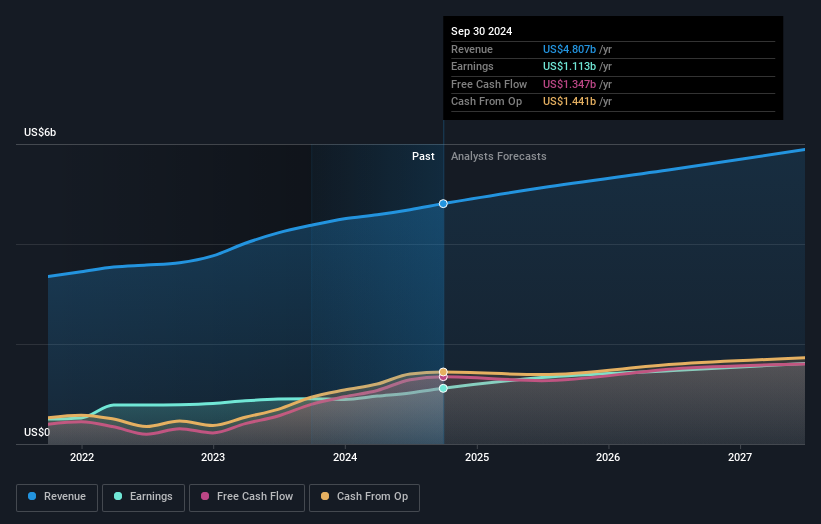

ResMed's narrative projects $6.7 billion revenue and $1.9 billion earnings by 2029. This requires 7.6% yearly revenue growth and an earnings increase of about $0.4 billion from $1.5 billion.

Uncover how ResMed's forecasts yield a $288.21 fair value, a 39% upside to its current price.

Exploring Other Perspectives

Before this news, the most cautious analysts were assuming revenue of about US$6.6 billion and earnings of roughly US$1.8 billion by 2029, which is a more restrained path than the consensus and reflects worry that GLP 1 usage or slower adoption of ResMed’s digital ecosystem could limit upside; you should treat this CFO change and the latest results as fresh information that might shift both that bearish view and the more optimistic scenarios.

Explore 8 other fair value estimates on ResMed - why the stock might be worth 13% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your ResMed research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free ResMed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ResMed's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.