How Investors May Respond To Seadrill (SDRL) After Citigroup’s Shift From Neutral To Sell

Seadrill Limited SDRL | 45.63 | +2.40% |

- In the past few days, Citigroup downgraded offshore driller Seadrill from Neutral to Sell, signaling a more cautious stance on the company’s outlook and underlying risks.

- This shift adds to an already mixed analyst backdrop, highlighting how differing views on offshore demand, balance sheet strength, and legal exposures are shaping sentiment around Seadrill.

- We’ll now examine how Citigroup’s downgrade reshapes Seadrill’s investment narrative, particularly around future earnings resilience and risk perception.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Seadrill Investment Narrative Recap

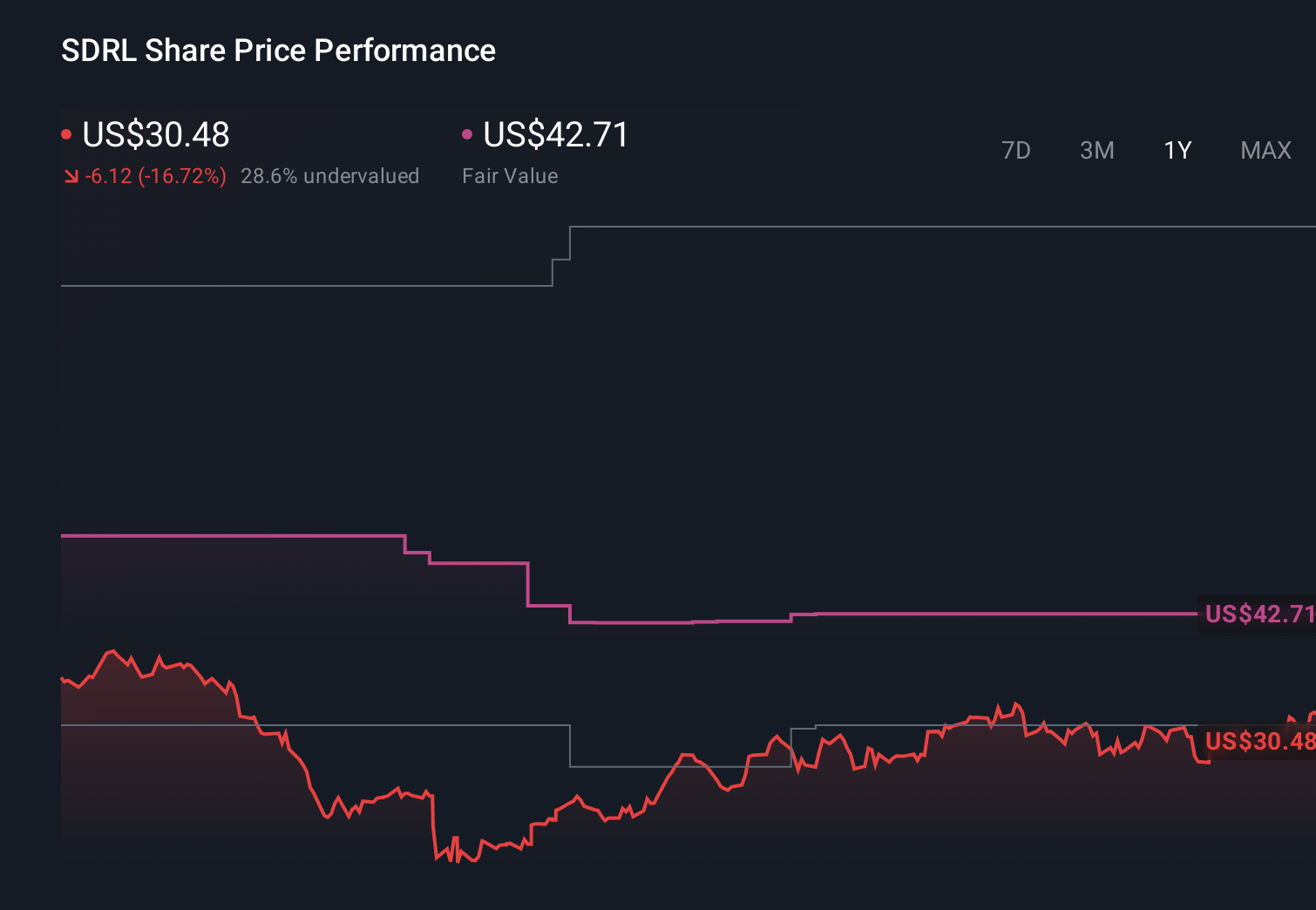

To own Seadrill, you need to believe that offshore drilling demand and tight high spec rig supply will eventually support stronger utilization and pricing, despite recent earnings volatility and legal overhangs. Citigroup’s downgrade to Sell and slightly lower US$32.00 price target primarily affects short term sentiment around earnings resilience, but does not materially change the key near term catalyst of contract wins and utilization, or the biggest current risk, which remains legal and regulatory exposures.

The most relevant recent announcement here is Seadrill’s Q3 2025 results and updated 2025 revenue guidance, which narrowed to US$1,360 million to US$1,390 million while the company still reported a year to date net loss and thinner margins. Against Citigroup’s more cautious stance, this combination of modest revenue guidance improvement and weaker profitability keeps the spotlight firmly on whether Seadrill can translate its backlog into more consistent earnings and cash flow without further legal or cost surprises.

Yet behind the headline downgrade, investors should be aware that unresolved legal exposures in Brazil and Angola could still...

Seadrill's narrative projects $1.6 billion revenue and $231.6 million earnings by 2028. This requires 7.2% yearly revenue growth and a $154.6 million earnings increase from $77.0 million.

Uncover how Seadrill's forecasts yield a $43.50 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community span roughly US$43 to US$376 per share, showing how far apart individual views can be. Set against this wide range, the risk that softer utilization and heavier competition could pressure day rates and margins into 2026 is a key factor readers should weigh as they compare these different perspectives.

Explore 5 other fair value estimates on Seadrill - why the stock might be worth over 10x more than the current price!

Build Your Own Seadrill Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 38 companies in the world exploring or producing it. Find the list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.