How Investors May Respond To Tutor Perini (TPC) Surging Revenue And Earnings Beat Expectations

Tutor Perini Corporation TPC | 0.00 |

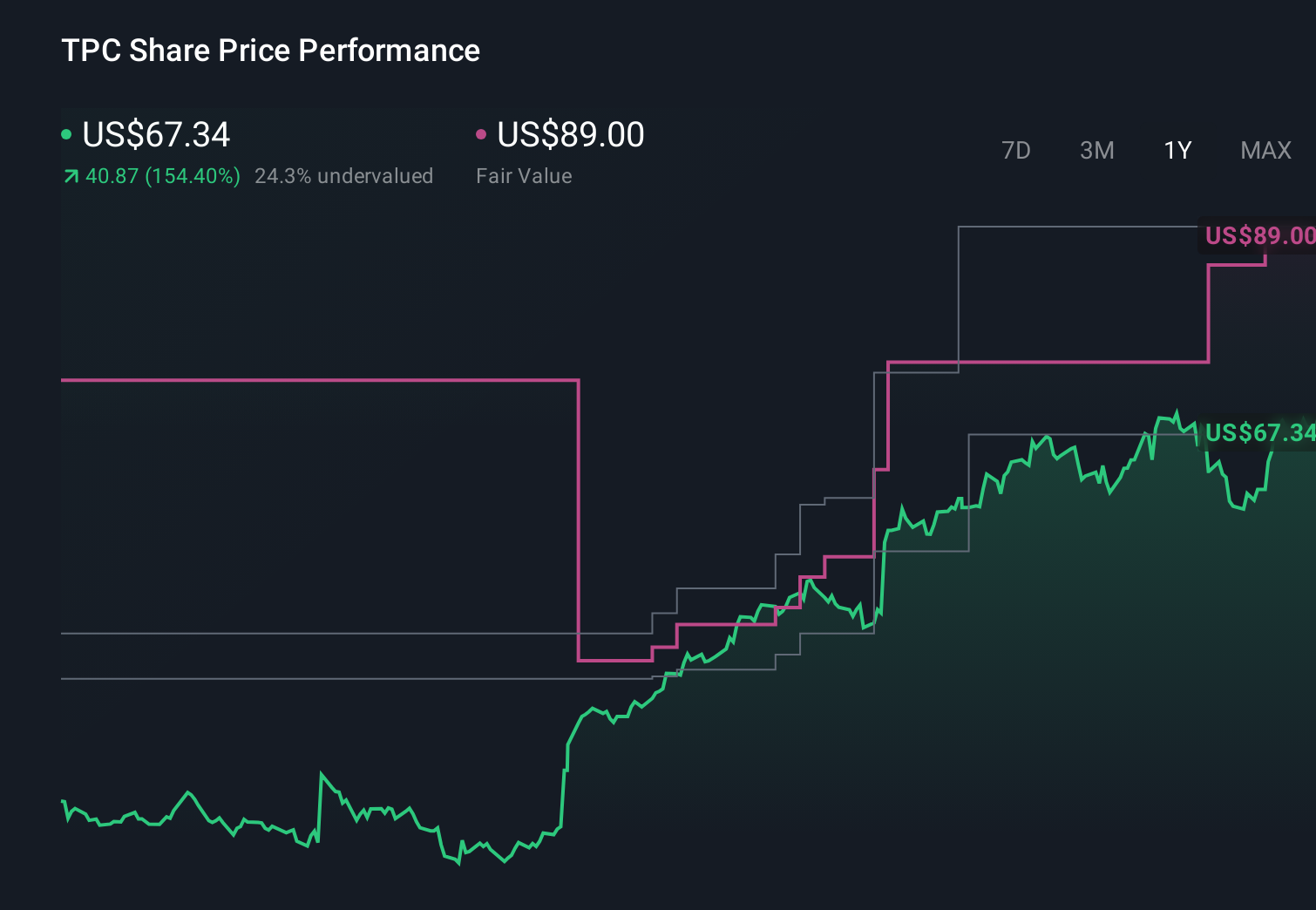

- Tutor Perini recently reported quarterly revenue of US$1.51 billion, up 41.2% year on year, with both revenue and earnings surpassing analyst estimates.

- This performance points to stronger-than-expected execution on its large project portfolio, potentially reinforcing confidence in its long-term backlog-driven outlook.

- We’ll now examine how this stronger-than-expected revenue growth influences Tutor Perini’s investment narrative built around backlog, margins, and risk.

Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Tutor Perini Investment Narrative Recap

To own Tutor Perini, you need to believe its record backlog can translate into steadier margins while execution and contract risks stay contained. The latest US$1.51 billion quarter, up 41.2% year on year and ahead of expectations, supports the near term catalyst of converting big civil and building projects into profitable revenue, but it does not remove the ongoing risk that any new cost overrun or dispute on a mega project could quickly unsettle that progress.

Among recent announcements, the Honolulu City Center Guideway and Stations contract, at about US$1.66 billion plus a later US$53 million change order, ties directly into this strong revenue print. It highlights how a few very large public infrastructure projects can both power growth and concentrate risk, especially when they run for many years and depend on smooth execution, stable funding, and careful cost control to protect margins.

Yet beneath the strong quarter, there is still the question of how Tutor Perini might handle a serious setback on one of these huge public projects that investors should be aware of...

Tutor Perini's narrative projects $7.8 billion revenue and $428.4 million earnings by 2029.

Uncover how Tutor Perini's forecasts yield a $109.50 fair value, a 30% upside to its current price.

Exploring Other Perspectives

By contrast, the most cautious analysts were assuming only about US$7.9 billion of revenue and US$294.2 million of earnings by 2029, reminding you that opinions on execution risks and future profitability can differ widely and that this latest revenue beat might ultimately shift both the optimistic and pessimistic cases over time.

Explore 5 other fair value estimates on Tutor Perini - why the stock might be worth as much as 96% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Tutor Perini research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Tutor Perini research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tutor Perini's overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.