How Investors May Respond To W. R. Berkley (WRB) Boosting Dividends And Restoring Buyback Firepower

W. R. Berkley Corporation WRB | 0.00 |

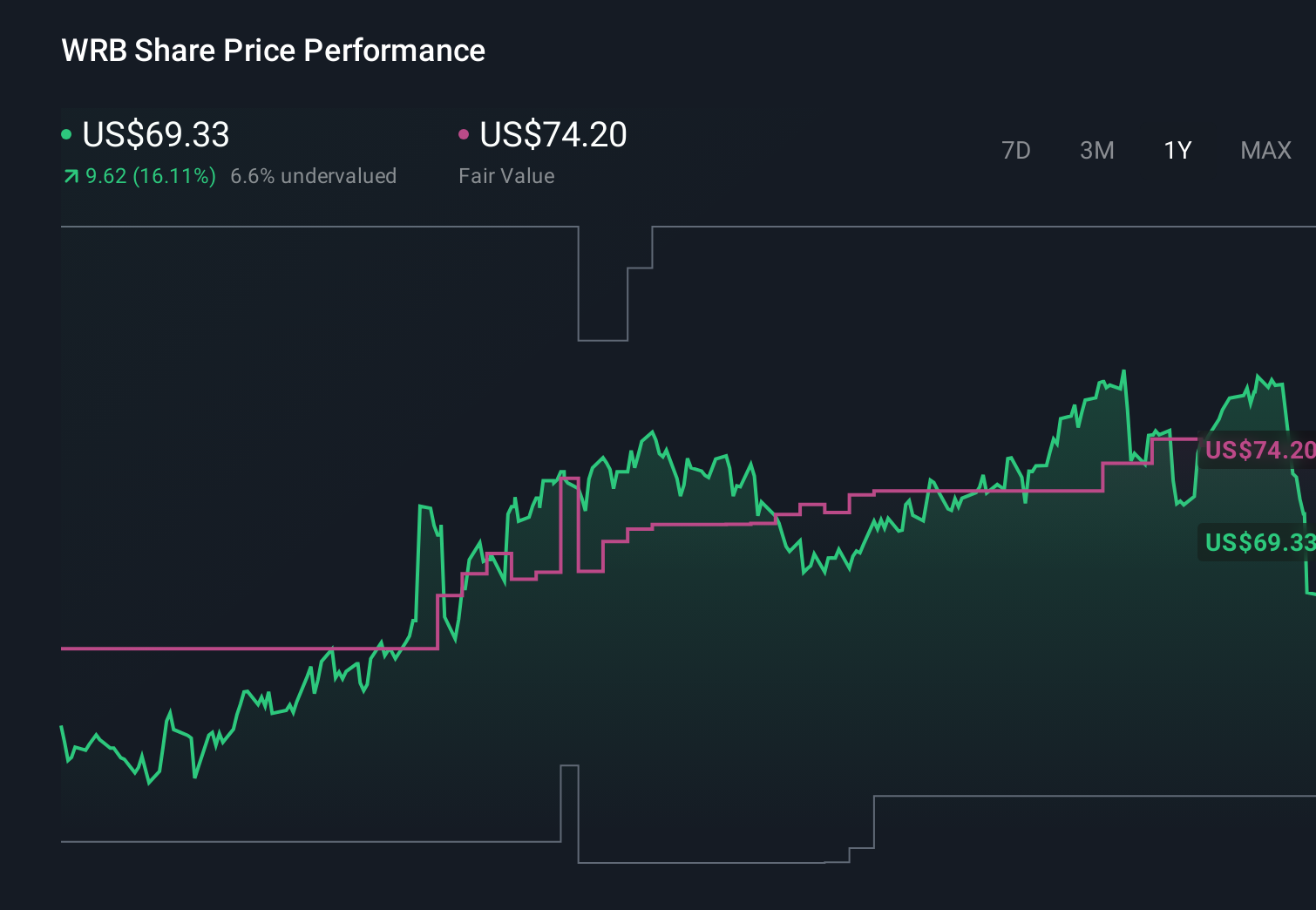

- W. R. Berkley recently announced that its board declared a special cash dividend of US$0.50 per share, raised the regular quarterly dividend by 11.1% to US$0.10 per share, and restored its share repurchase authorization to 25,000,000 shares, with the dividends scheduled to be paid on July 2, 2026.

- This combination of higher dividends and renewed buyback capacity highlights how the insurer is returning capital to shareholders while signaling confidence in its balance sheet strength.

- Next, we will examine how the higher regular dividend shapes W. R. Berkley’s existing investment narrative around capital management.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

W. R. Berkley Investment Narrative Recap

To own W. R. Berkley, you need to believe its specialty focus, underwriting discipline, and capital allocation can keep creating value despite competition and inflation pressures. The new special dividend, higher regular dividend, and refreshed buyback authorization all support the near term capital return story, but do not materially change the core short term catalyst, which is sustaining attractive underwriting results while managing rising loss costs. The biggest risk remains that pricing or claims trends move against the company faster than expected.

The most relevant prior announcement here is the Q1 2026 update, where W. R. Berkley reported US$3,690.33 million in revenue and US$515.22 million in net income. That solid earnings base provides context for the board’s decision to increase cash returns, suggesting capital levels can support both business investment and shareholder distributions. For investors watching catalysts, this link between earnings power and capital management is central to assessing how durable the current capital return profile really is.

Yet behind the bigger capital return headlines, investors should still be aware of how prolonged social and economic inflation could...

W. R. Berkley’s narrative projects $14.3 billion revenue and $2.0 billion earnings by 2028. This requires 0.0% yearly revenue growth and a $0.2 billion earnings increase from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $68.33 fair value, a 5% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady progress, the most cautious analysts assume revenue could shrink to about US$13.8 billion with flat earnings near US$1.9 billion a year and warn that rising catastrophe risks might still pressure the story despite today’s dividend and buyback news, so it is worth comparing these more pessimistic views with your own expectations.

Explore 3 other fair value estimates on W. R. Berkley - why the stock might be worth as much as 88% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.