How Investors May Respond To W.W. Grainger (GWW) Upgraded 2026 Outlook And Higher Dividend

W.W. Grainger, Inc. GWW | 0.00 |

- In its latest update, W.W. Grainger reported a strong first quarter, raising its 2026 net sales and earnings guidance and lifting its quarterly dividend by 10%, underscoring progress in its business transformation and digital expansion across High-Touch Solutions and Endless Assortment segments.

- The company’s emphasis on enhanced e-commerce capabilities, supply chain investments, and improving performance in Canada highlights how its operational upgrades are reshaping the quality and resilience of its cash generation profile.

- We’ll now examine how Grainger’s upgraded 2026 guidance and dividend increase may influence its existing investment narrative and risk outlook.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

W.W. Grainger Investment Narrative Recap

To own Grainger, you need to believe its High Touch and Endless Assortment businesses can keep converting operational improvements and digital growth into resilient cash generation. The latest guidance raise and 10% dividend increase support that view in the near term, while also sharpening focus on valuation risk and the possibility that higher capital spending or a softer MRO backdrop could pressure margins if conditions turn less supportive.

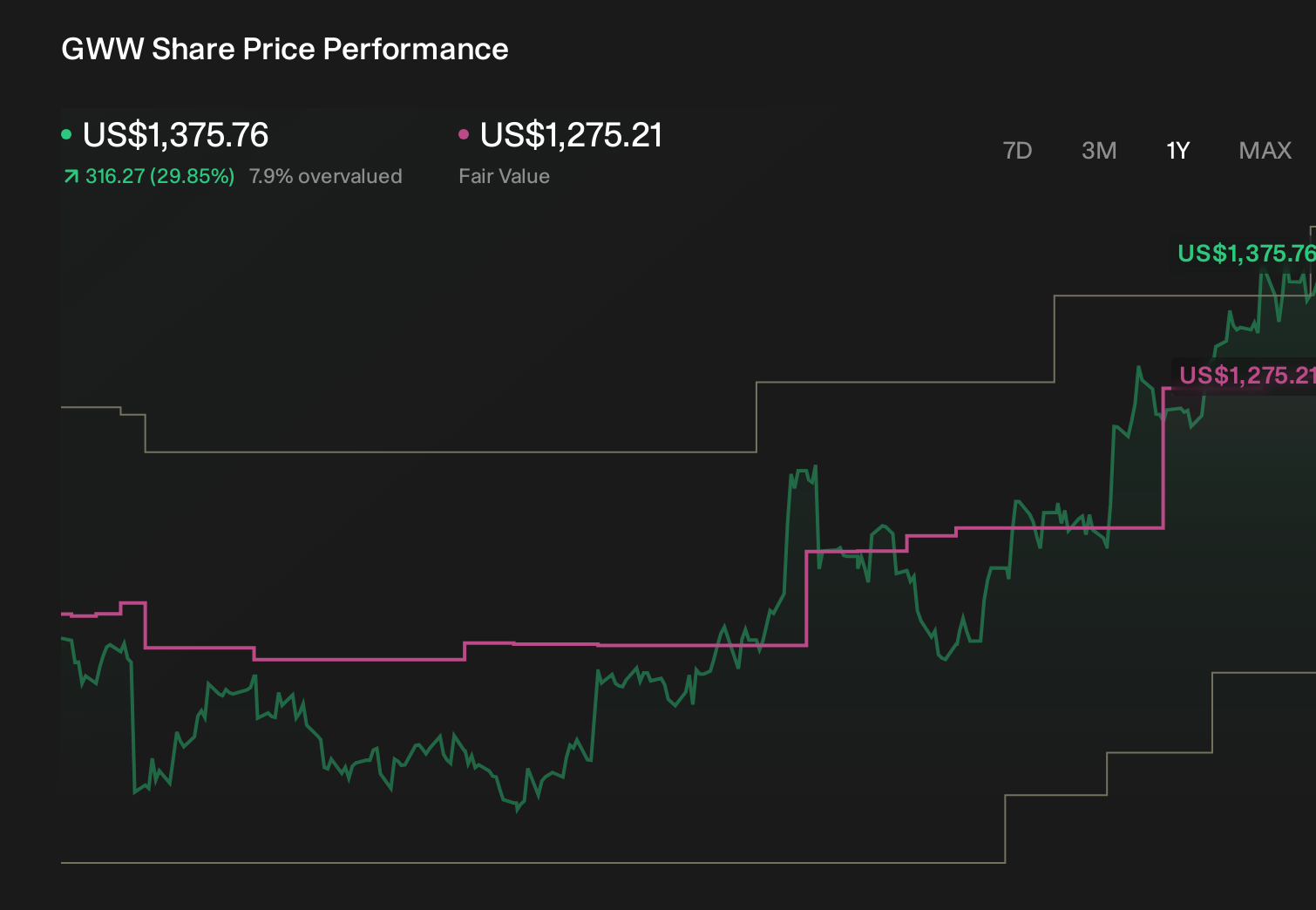

The most relevant recent announcement is Grainger’s upgraded 2026 outlook to US$19.2 billion to US$19.6 billion in net sales and US$44.25 to US$46.25 in diluted EPS, coming alongside a 10% quarterly dividend increase to US$2.49 per share. Against a share price already above the consensus target and a premium P/E multiple, that stronger guide reinforces the current momentum catalyst but also makes any future disappointment on growth or margins more sensitive for shareholders.

Yet behind the raised guidance and higher dividend, investors should also be aware of how rising capital intensity could affect free cash flow and...

W.W. Grainger's narrative projects $22.5 billion revenue and $2.5 billion earnings by 2029. This requires 7.0% yearly revenue growth and about a $0.7 billion earnings increase from $1.8 billion today.

Uncover how W.W. Grainger's forecasts yield a $1275 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Grainger could reach about US$22.5 billion of revenue and US$2.6 billion of earnings by 2029, which is a much more upbeat view than consensus and leans heavily on continued digital and supply chain gains, so this strong quarter may either reinforce that optimism or prompt you to question whether those higher expectations still look realistic.

Explore 3 other fair value estimates on W.W. Grainger - why the stock might be worth 19% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your W.W. Grainger research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free W.W. Grainger research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W.W. Grainger's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.