How Investors May Respond To Zscaler (ZS) Expanding Its Zero Trust Ecosystem With New Partnerships

Zscaler, Inc. ZS | 118.05 | -3.42% |

- In late March 2026, P0 Security announced a technology partnership with Zscaler and Versa unveiled an integration between Versa Secure SD-WAN and Zscaler Internet Access, both aimed at extending Zero Trust security and automating secure connectivity for modern production and branch environments.

- Together with Zscaler’s recent fiscal Q2 results and raised full-year guidance, these collaborations highlight growing demand for identity-first, AI-aware Zero Trust security spanning connectivity, authentication and authorization.

- We’ll now explore how this expanded Zero Trust ecosystem, especially the Versa SD-WAN integration, may influence Zscaler’s existing investment narrative.

Find 58 companies with promising cash flow potential yet trading below their fair value.

Zscaler Investment Narrative Recap

To own Zscaler, you have to believe in sustained adoption of cloud delivered, identity first Zero Trust security, even as competition and cloud providers crowd the field. The new P0 Security and Versa SD WAN integrations reinforce the Zero Trust platform story but do not fundamentally change the near term tension between strong top line guidance and ongoing losses, or the key risk that hyperscalers and large security vendors keep compressing pricing and margins.

Among recent updates, Versa’s integration of its Secure SD WAN with Zscaler Internet Access looks most relevant here, because it directly supports the shift away from legacy appliances toward unified, cloud based security. That aligns with one of the main catalysts around the multi year replacement cycle for firewalls and branch networking, but also puts a spotlight on whether Zscaler can turn higher automation and larger deployments into better operating leverage without letting sales and marketing spend run too far ahead of revenue.

Yet even as these partnerships broaden Zscaler’s reach, investors should be aware that intensifying pressure from bundled cloud security offerings could…

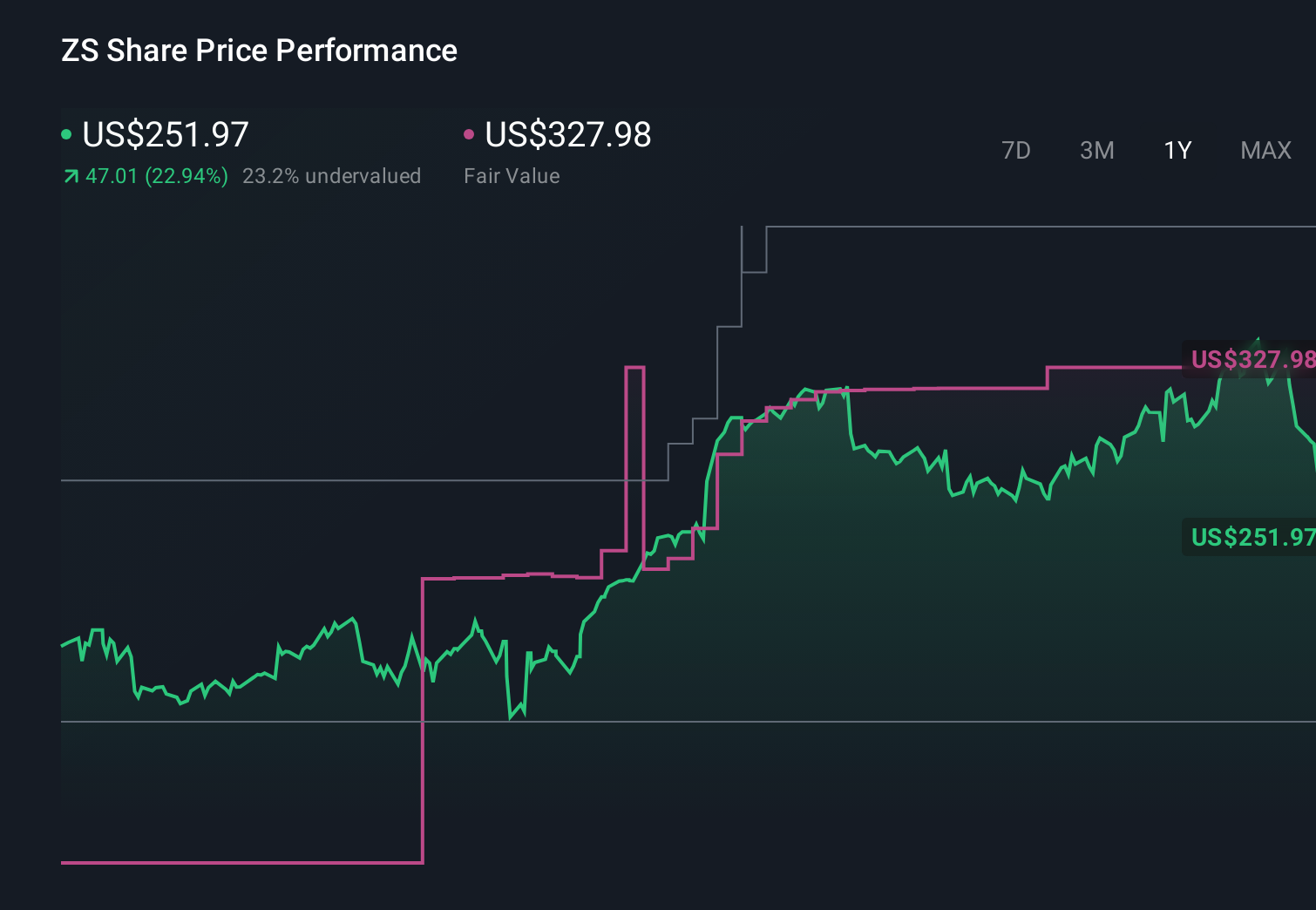

Zscaler's narrative projects $4.7 billion revenue and $139.8 million earnings by 2028. This requires 20.5% yearly revenue growth and about an $181 million earnings increase from -$41.5 million today.

Uncover how Zscaler's forecasts yield a $304.23 fair value, a 120% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$5.5 billion by 2029, so partnerships like Versa and P0 might either reinforce that upside or force a rethink of how quickly Zscaler can balance rapid platform expansion with the rising costs and competition they were already worried about.

Explore 6 other fair value estimates on Zscaler - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Zscaler research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Zscaler research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zscaler's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.