How Margin Pressure and Perceived Undervaluation Will Impact MercadoLibre (MELI) Investors

MercadoLibre, Inc. MELI | 0.00 |

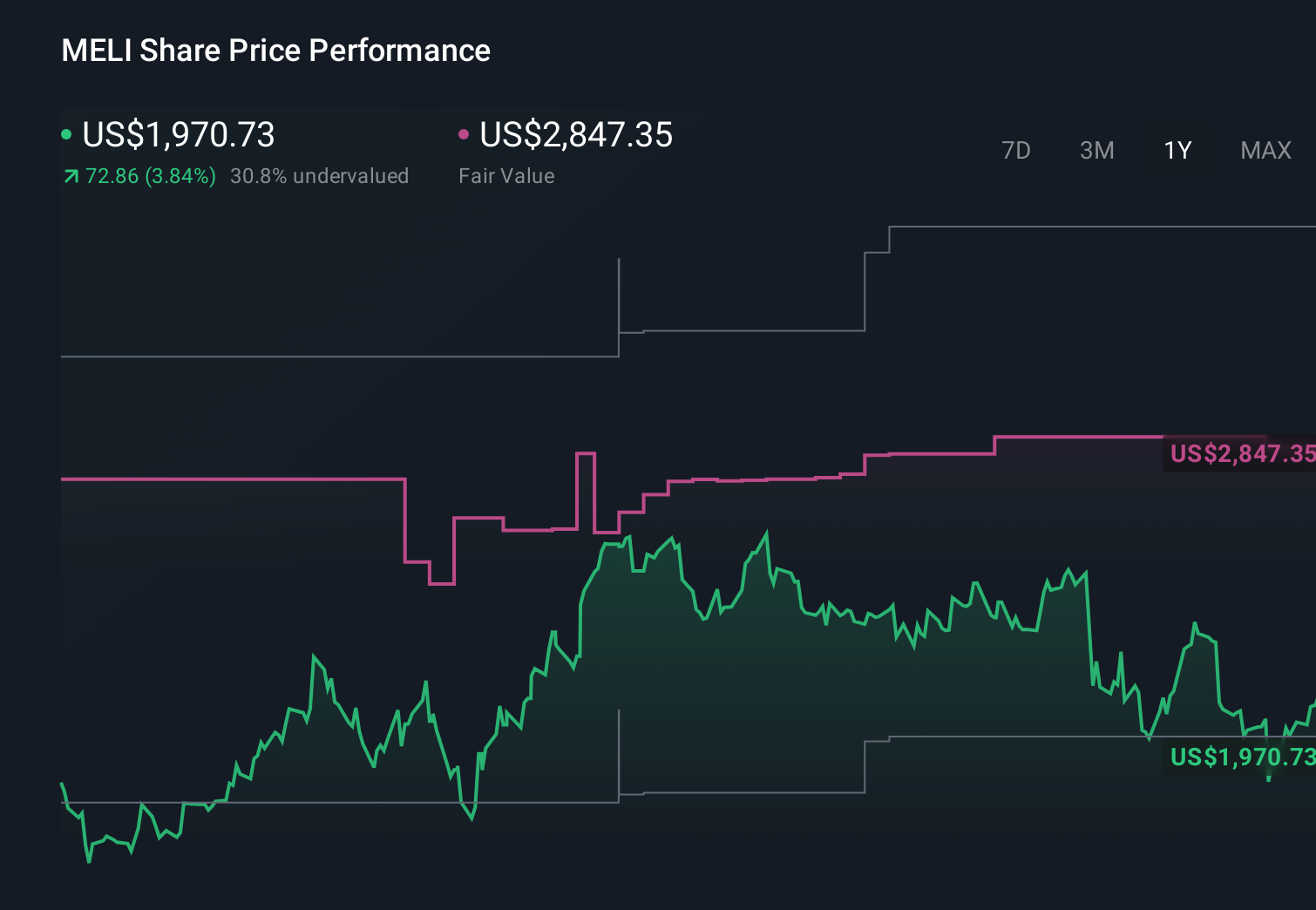

- In recent days, coverage of MercadoLibre has highlighted strong revenue growth, expanding fintech operations, and heavy ongoing investment that is compressing margins and earnings expectations.

- At the same time, several analysts and institutional investors argue that the shares may be undervalued based on discounted cash flow analysis and MercadoLibre’s entrenched role in Latin American e-commerce and digital payments.

- Against this backdrop of perceived undervaluation and margin pressure, we’ll explore how these developments may reshape MercadoLibre’s existing investment narrative.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you need to believe its integrated e commerce and fintech platform in Latin America can keep growing engagement while eventually translating heavy investment into durable profitability. The key near term catalyst remains execution in fintech, particularly credit cards and lending, while the biggest risk is that rapid credit expansion and ongoing spending keep margins under pressure. Recent estimate cuts and a Zacks Strong Sell rating highlight this risk, but they do not yet fundamentally alter that core thesis.

Among the recent developments, Bank of America’s focus on MercadoLibre’s fast growing credit card operation feels most relevant. The portfolio more than doubled year over year in Q1 2026 and now represents 45% of total lending, with monthly active credit card users up 68%. This directly ties into both the upside case for fintech driven revenue growth and the downside risk that credit quality or capital needs could weigh further on earnings.

Yet beneath the growth story, investors should be aware that rapid credit expansion in volatile markets could...

MercadoLibre's narrative projects $57.9 billion revenue and $4.8 billion earnings by 2029. This requires 26.1% yearly revenue growth and a $2.8 billion earnings increase from $2.0 billion today.

Uncover how MercadoLibre's forecasts yield a $2440 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts were already assuming only steady 6 percent margins and around US$3.6 billion of earnings by 2029, so if rising competition or credit costs hit harder than expected, their more pessimistic view of slower, harder won growth might start to look less extreme.

Explore 24 other fair value estimates on MercadoLibre - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MercadoLibre research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.