How Needham’s KARNO Commercialization Call Could Reshape the Hyliion Holdings (HYLN) Investment Narrative

Hyliion Holdings HYLN | 0.00 |

- In June 2026, Needham initiated coverage on Hyliion Holdings with a Buy rating, citing the company’s planned transition from development to commercialization of its KARNO power module and highlighting multiple potential catalysts through year-end 2026.

- The report underscored KARNO’s fuel flexibility and emissions profile, alongside Hyliion’s debt-free balance sheet, as key factors supporting its early commercialization plans in clean energy and power applications.

- We’ll now examine how Needham’s bullish initiation and focus on KARNO commercialization timing could influence Hyliion’s existing investment narrative.

Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

Hyliion Holdings Investment Narrative Recap

To own Hyliion today, you have to believe the KARNO power module can move from R&D projects to meaningful commercial sales, particularly in data centers and defense, without exhausting the company’s cash. Needham’s new coverage reinforces that commercialization timeline as the key near term catalyst, while the biggest current risk remains any delay in UL certification or customer field deployments. The stock’s jump on the rating does not change that underlying execution risk.

The recent selection of the USX 1 Defiant as a test vessel for four 200 kW KARNO Cores ties directly into the catalysts Needham highlighted. It connects Hyliion’s multi fuel, 800 V DC architecture with a concrete defense use case, potentially supporting the shift from pure R&D revenue to early product sales. How quickly those sea trials progress, and how reliably the system performs, will be critical in shaping the commercialization story.

Yet against this optimism, investors should be aware that delays to reaching full 200 kilowatt output and facility level UL certification could...

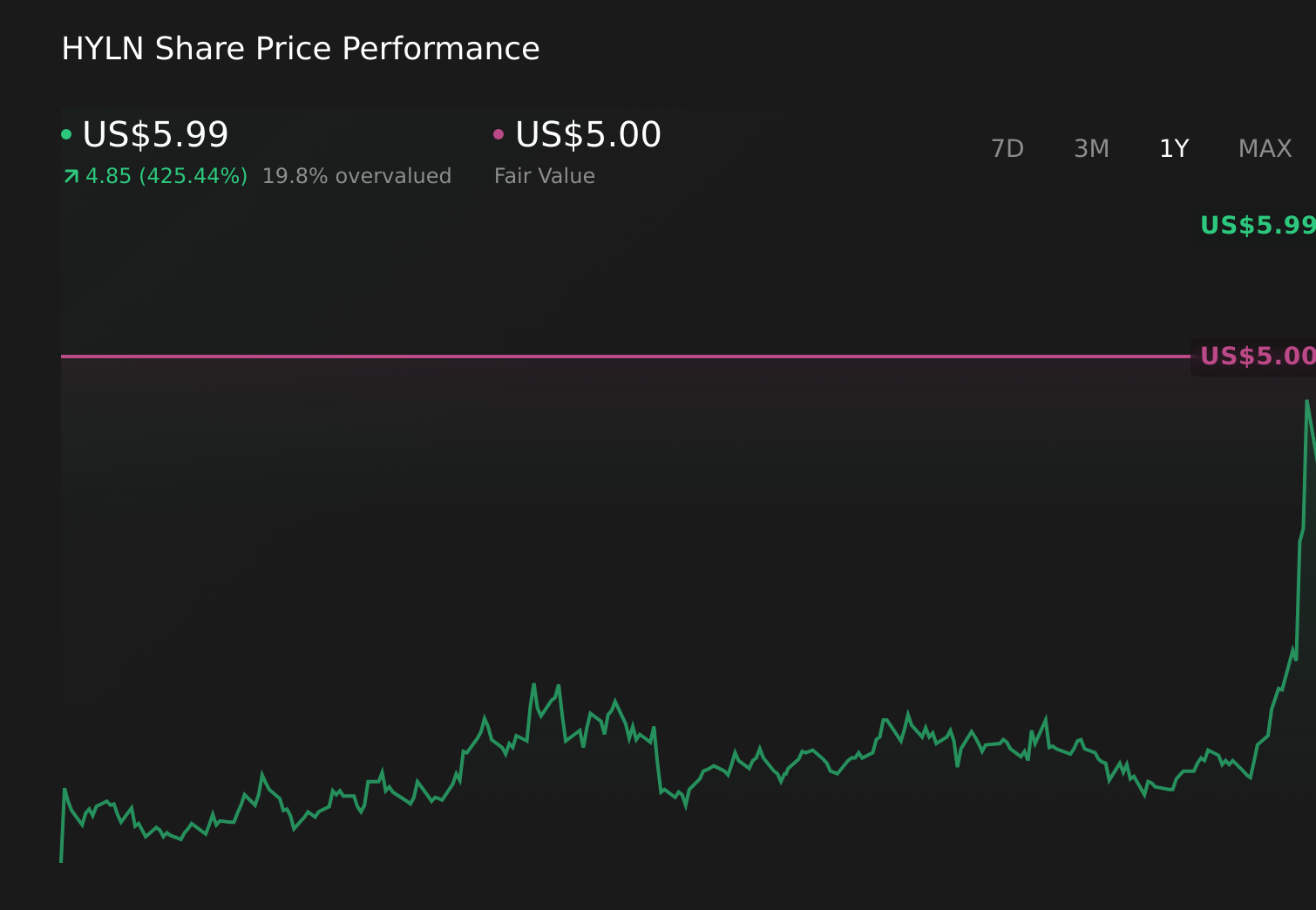

Hyliion Holdings' narrative projects $154.7 million revenue and $18.3 million earnings by 2028. This requires 230.8% yearly revenue growth and a $76.7 million earnings increase from -$58.4 million today.

Uncover how Hyliion Holdings' forecasts yield a $5.00 fair value, a 33% downside to its current price.

Exploring Other Perspectives

Needham’s upbeat view lands alongside much more cautious analysts who, before this news, were assuming roughly 162 percent annual revenue growth but still no profits within three years. If you are weighing the risk that early data center deployments slip or UL certification drags, these low end forecasts offer a useful counterpoint and show just how differently people can interpret the same business story.

Explore 4 other fair value estimates on Hyliion Holdings - why the stock might be worth as much as $7.00!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hyliion Holdings research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Hyliion Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hyliion Holdings' overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.